Why I Passed on Graftech (EAF): Riding The Battery Hype, Or Perhaps Not...

A deep-dive into graphite electrodes, needle coke, vertical integration, and the art of knowing when the birds in the bush will never make it into your hand.

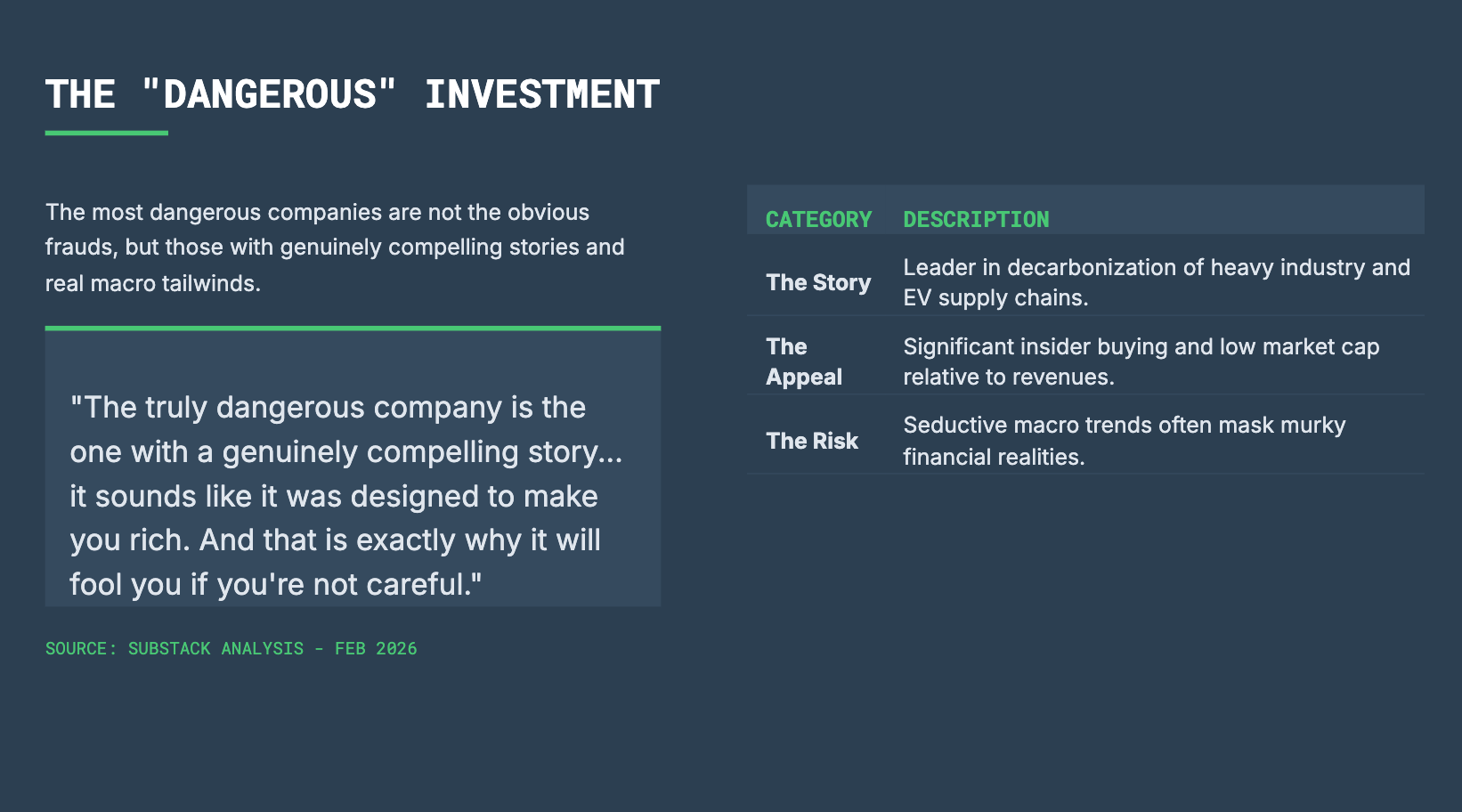

There is a kind of company that is the most dangerous thing in investing. It is not the fraudulent company. It is not the obviously bad company with terrible products and incompetent management. Those are easy — you just avoid them. The truly dangerous company is the one with a genuinely compelling story, one that touches real macro tailwinds, operates in an industry you’ve never heard of, and sits at the intersection of the green energy revolution, the decarbonization of heavy industry, and the geopolitical race for critical materials. It sounds like it was designed to make you rich. And that is exactly why it will fool you if you’re not careful.

Graftech International (NYSE: EAF) is that company.

I want to be very clear at the outset: this is not a short thesis. It is not a story about a terrible business or dishonest management. Graftech makes something genuinely essential. It operates in a space that is structurally shifting in its favor over the long term. Insiders are buying. And at a market cap of just over $200 million at the time of my analysis — a company with $500 million in annual revenues — the headline numbers look like the setup to a very exciting trade. I understand why people are excited about it. The company came on to my radar initially because Marathon asset management took a massive stake in it (and scaled down eventually).

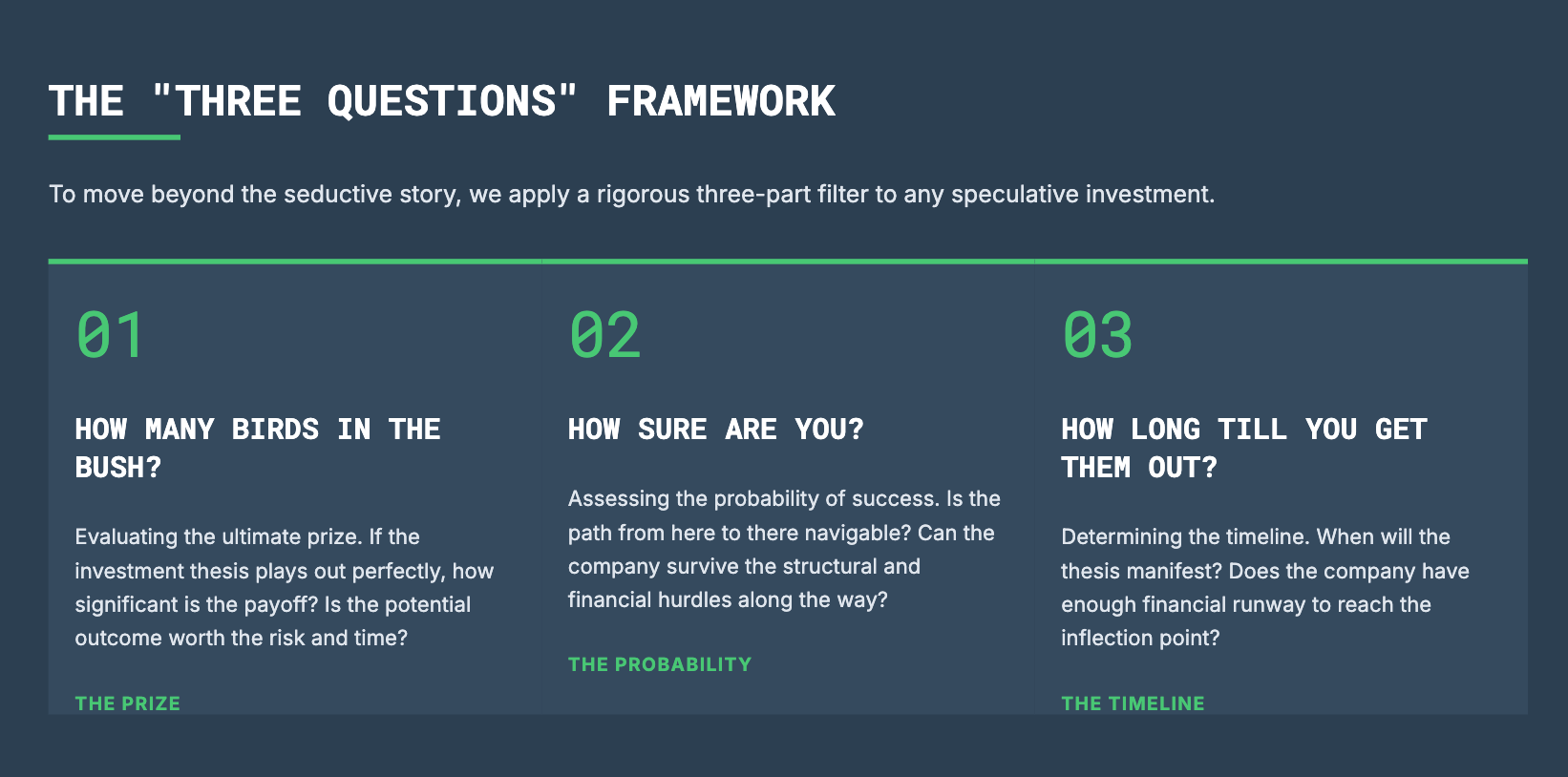

But I’m passing. And I want to walk you through exactly why, because the reasoning is more useful than the conclusion. The framework I use has three questions, and if any one of them fails, the investment is rejected. Those questions are: How many birds are in the bush? How sure are you? How long till you get them out? By the time you’re done reading this, I think you’ll see not just why I passed on Graftech, but how to apply this kind of thinking to any speculative situation where the story is seductive and the numbers are murky.

Let’s start at the beginning, because you need to understand what Graftech actually does before any of this makes sense.

Carbon, Steel, and the Little Electrode That Runs the World

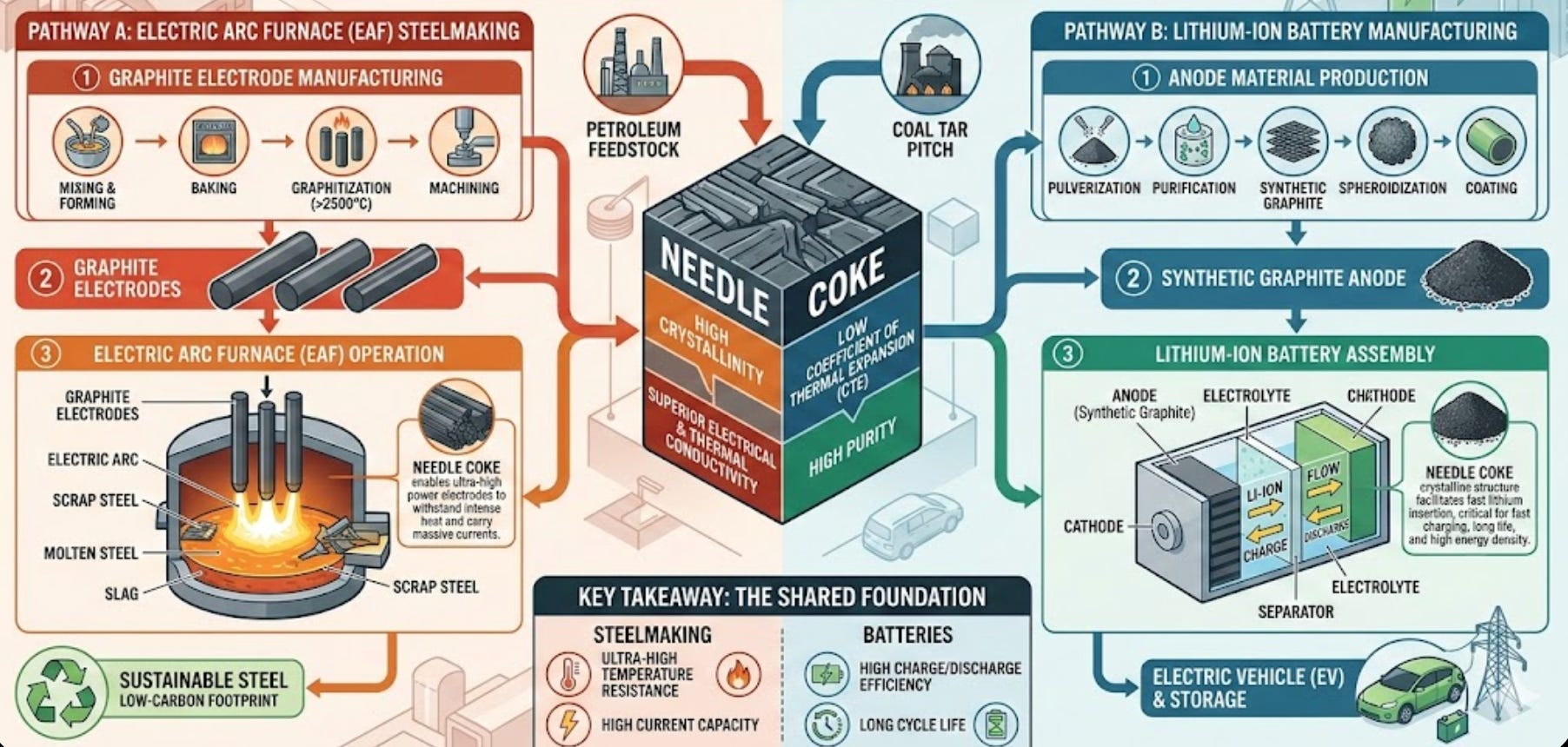

Picture a giant furnace — not the kind you have in your basement, but an industrial monster the size of a house, capable of reaching temperatures exceeding 3,500 degrees Celsius. Inside this furnace, mountains of scrap steel are fed in: old cars, demolished bridges, outdated refrigerators, the metal detritus of human civilization. And at the top of this furnace, plunging down into the heat like enormous lightning rods, are three cylindrical rods of graphite — each one roughly as tall as a person and as wide as a barrel. These are graphite electrodes, and they are the mechanism by which massive electrical current is converted into the arc of heat that melts steel. Without them, there is no Electric Arc Furnace (EAF) steelmaking. Without EAF steelmaking, the world’s transition away from coal-belching blast furnaces basically stalls.

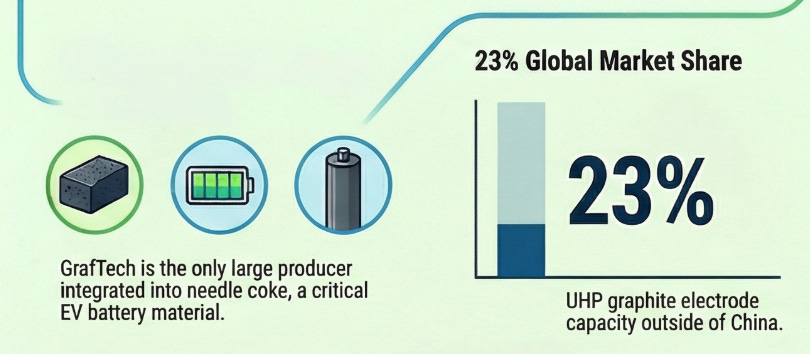

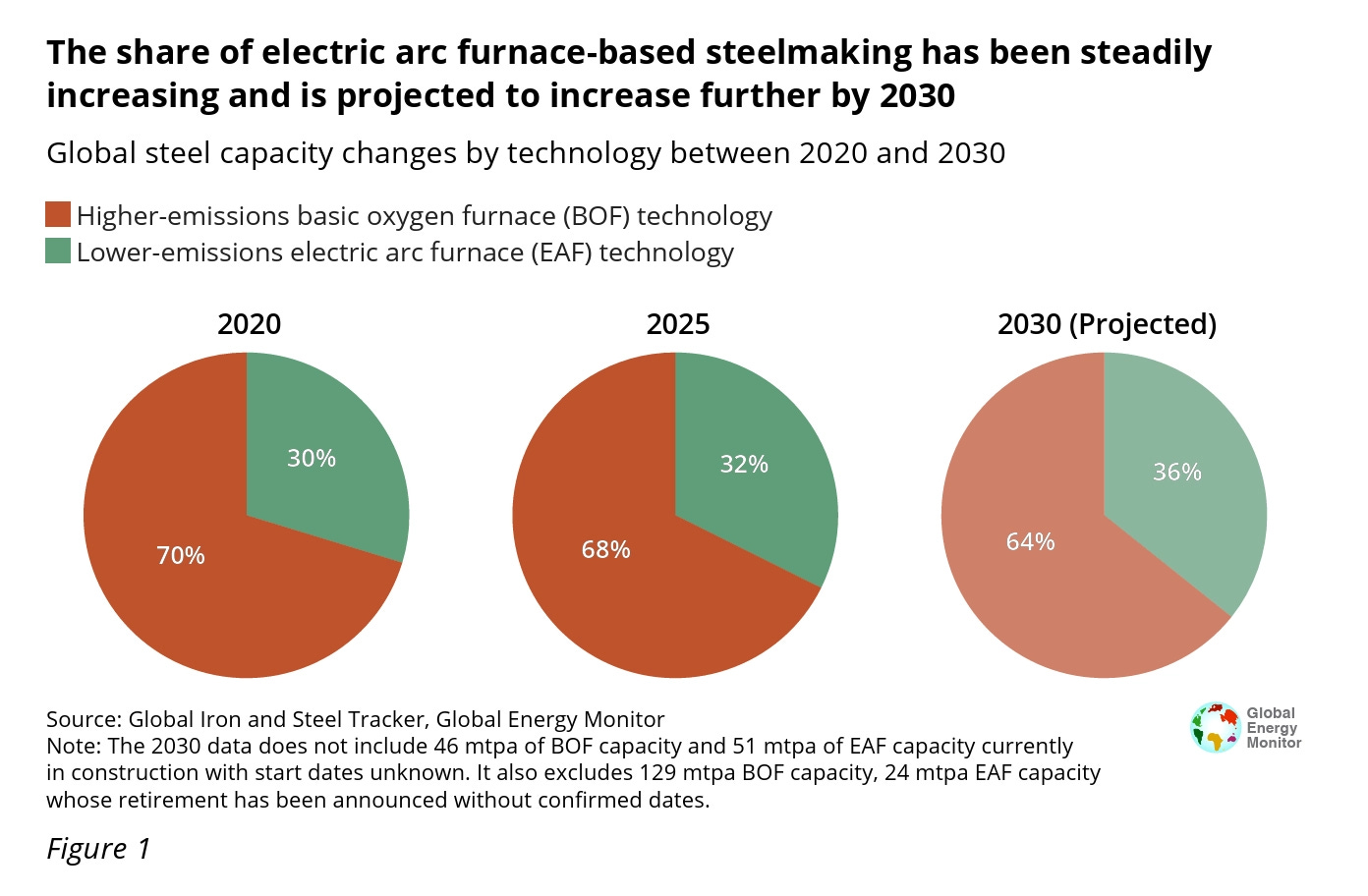

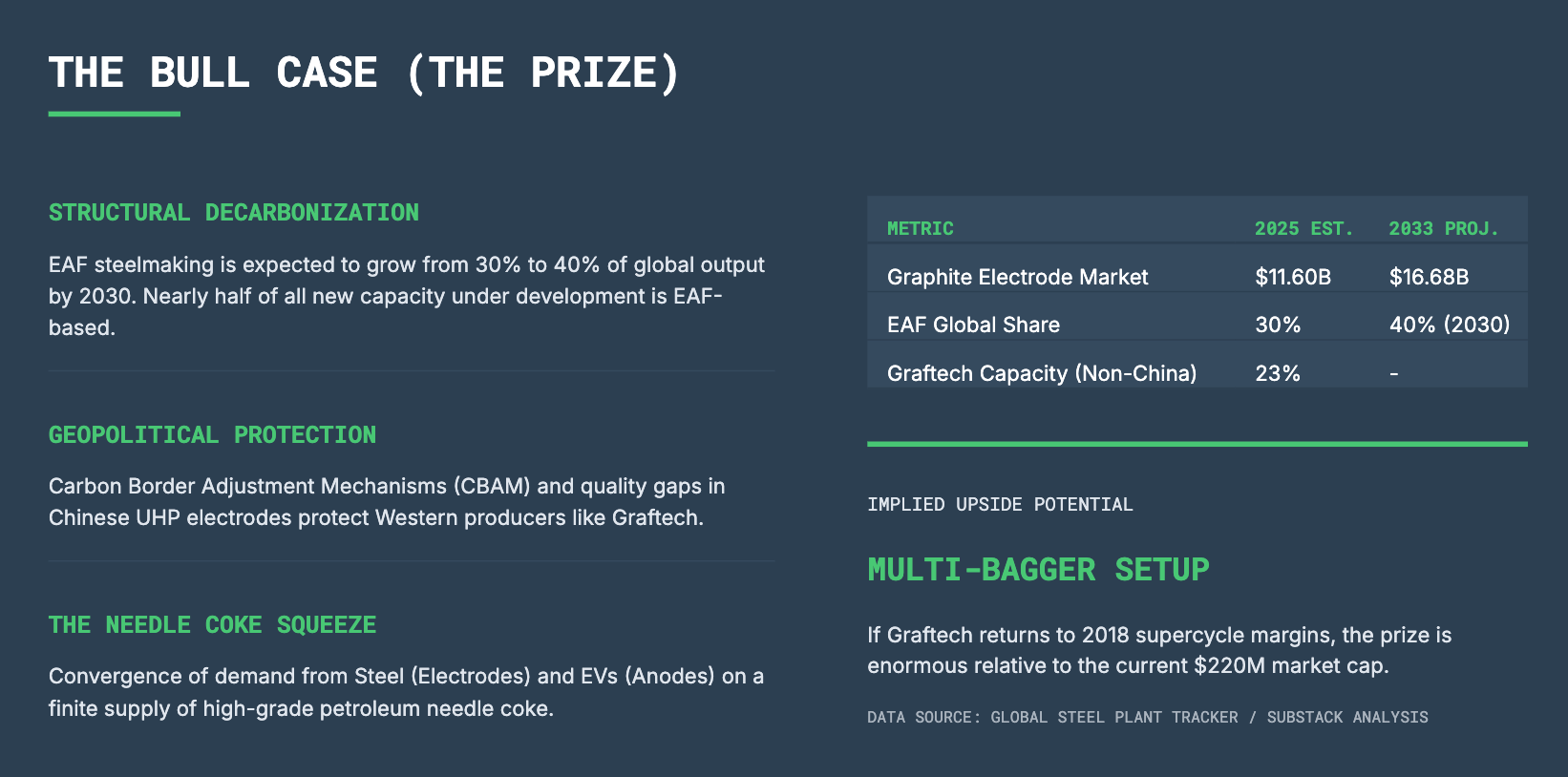

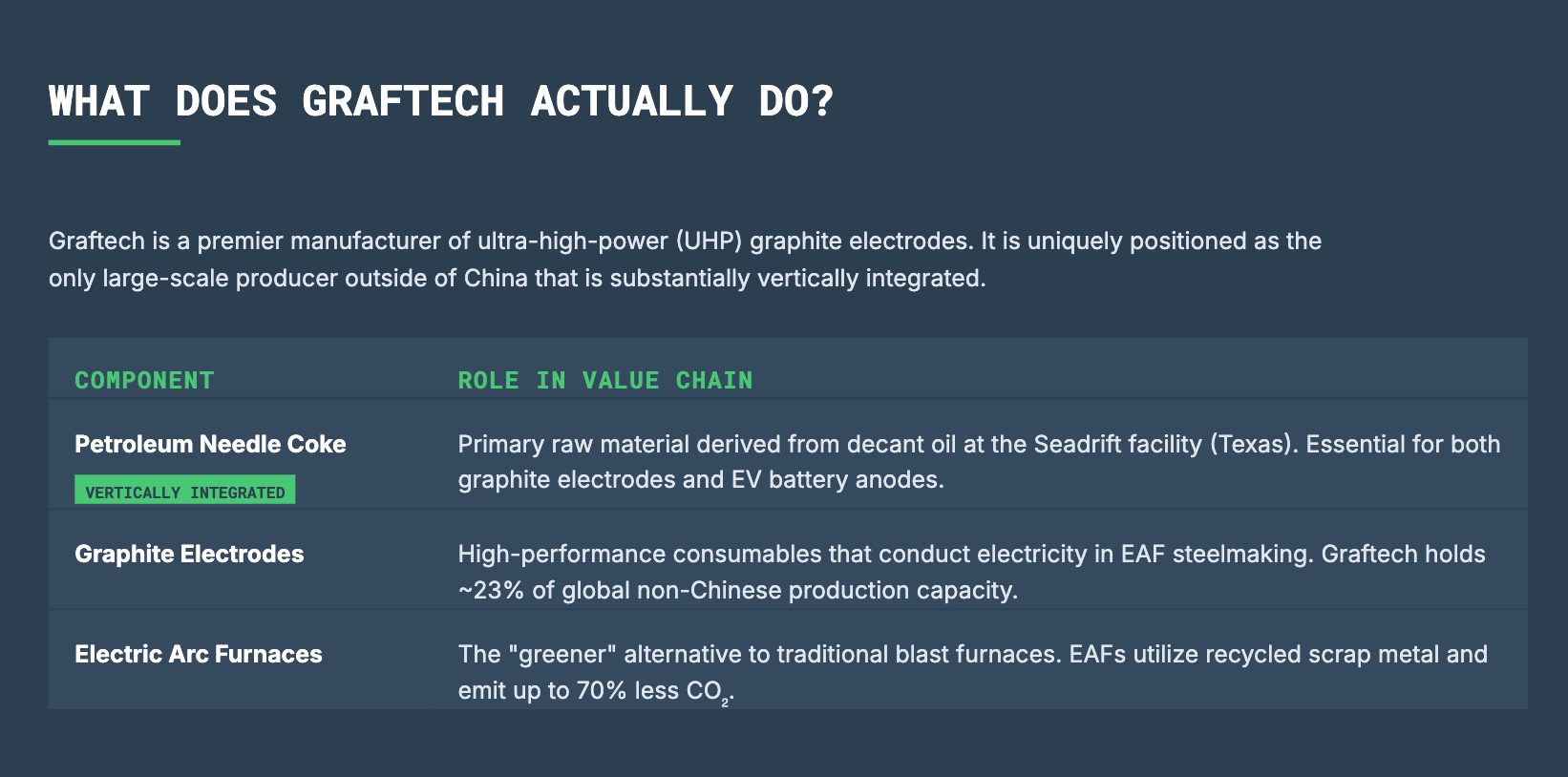

Graftech makes these electrodes. In fact, it is one of the most important manufacturers of high-performance, ultra-high-power (UHP) graphite electrodes in the world outside of China, with roughly 23% of global (non-Chinese) production capacity. That is a meaningful position in a niche market. EAF steelmaking currently represents about 30% of global steel output, and by 2030 it is expected to reach 40% as policy mandates tighten on blast furnace emissions — a route that emits up to 70% less CO₂ than the traditional blast-oxygen pathway. So Graftech sits at the center of one of the most powerful secular trends of our industrial era: the decarbonization of steel.

But here is where the story gets interesting — and complicated. Because Graftech doesn’t just make the electrodes. It also makes the primary raw material that goes into the electrodes: petroleum needle coke. This stuff is produced at their Seadrift facility in Port Lavaca, Texas, from a highly aromatic feedstock called decant oil. The needle coke is then shipped to their electrode manufacturing plants in Calais (France), Pamplona (Spain), and Monterrey (Mexico), where it is baked, impregnated, re-roasted, graphitized, and machined into the finished product. This process — this vertical integration — is the core of the Graftech bull thesis. And, as you will see, it is also the core of why I cannot buy the stock right now.

To understand the double-edged nature of that integration, you need to understand needle coke as a material. It is not just used in graphite electrodes. Needle coke also plays a critical role in the expanding electric vehicle battery market, because synthetic graphite — the preferred anode material for lithium-ion EV batteries due to its superior charging rate and energy density — is made using needle coke as a feedstock. This means needle coke has two hungry customers competing for supply: the steelmaking industry and the battery industry.

In theory, that creates the conditions for a structural supply squeeze that would benefit a vertically integrated needle coke producer enormously.

In theory.

Section I: How Many Birds Are in the Bush?

The first question an investor must ask is simply: if this thing works, how good is it? How much money is actually sitting in the bush waiting to be captured? This is not the same as asking whether the stock is cheap — it is asking whether the potential outcome, if achieved, is worth the risk and time you’re about to take on.

Let’s build the bull case for Graftech as honestly as we can, because it deserves a fair hearing.

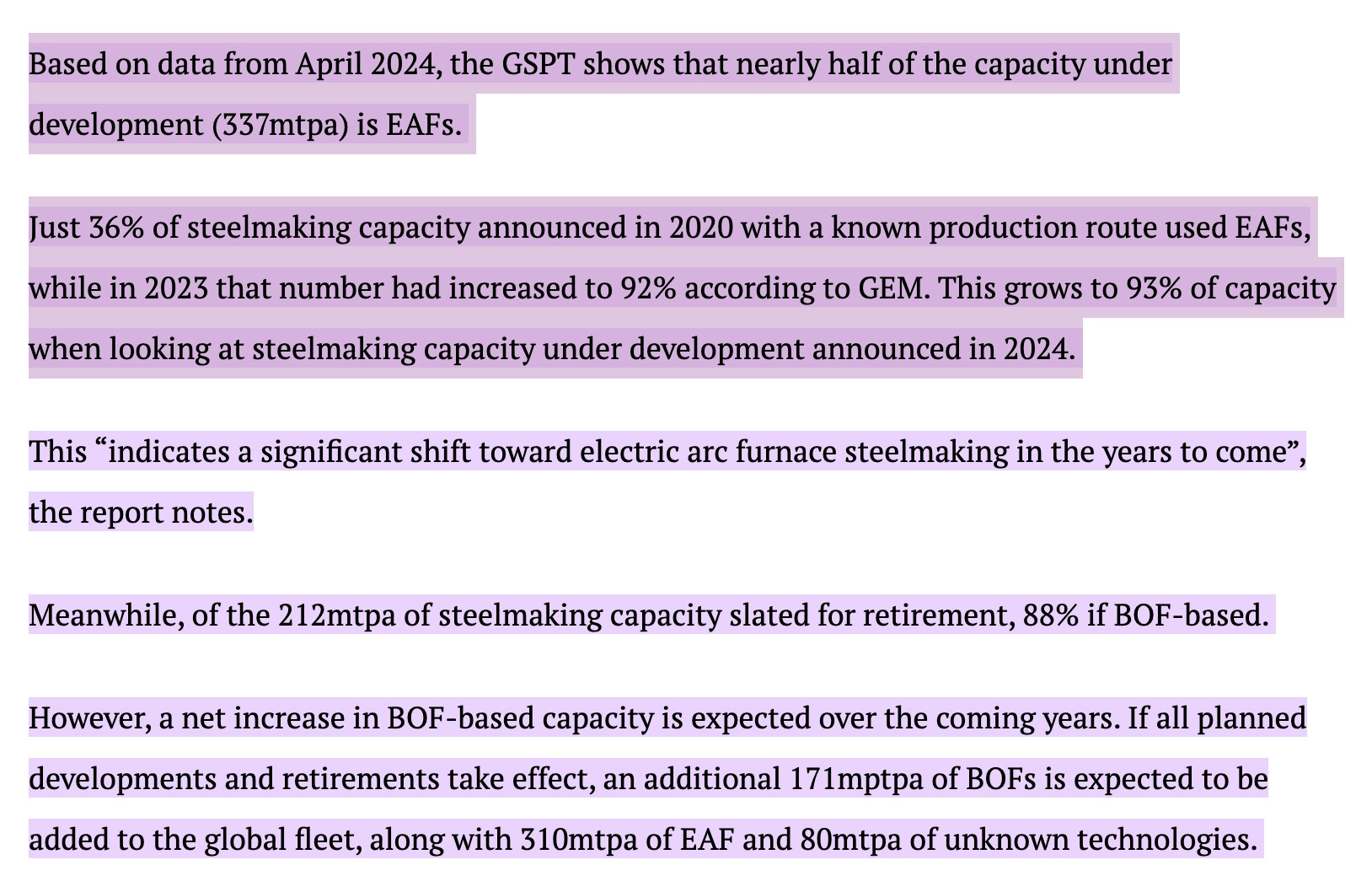

The Macro Tailwind Is Real. The shift from blast furnace (BOF) to electric arc furnace steelmaking is not a speculative forecast — it is happening, and the data is unambiguous. Based on Global Steel Plant Tracker data, EAF steelmaking accounted for roughly 30% of global output in 2025 and is expected to reach 40% by 2030 as policy mandates tighten. More specifically, nearly half of all new steelmaking capacity currently under development globally is EAF-based, which signals that the structural transition is accelerating even if the installed base moves slowly. EAFs are economically attractive not just because they are greener — they are cheaper to build than blast furnaces, more operationally flexible, and capable of profitable production at lower volumes, which suits the economics of smaller, regional “mini-mill” operators perfectly.

The China Wall Protects Western Producers. China produces more graphite electrodes than the rest of the world combined, and its manufacturers have been dumping product globally at prices that are causing real pain to Western producers. But there are structural limits to how far this can go. The carbon border adjustment mechanism (CBAM) implemented at the beginning of 2026, as well as new tariff protection measures expected to take effect later in the year, are expected to support higher levels of EAF steel production in key commercial regions for Graftech. Additionally, a significant portion of China’s UHP electrodes simply don’t meet the quality standards demanded by the most sophisticated steel mills, and the tariff and logistics cost of importing Chinese electrodes into the US and Europe further levels the playing field. Graftech’s facilities in France, Spain, and Mexico position it as the natural Western-hemisphere supplier of choice.

The Needle Coke Thesis Is Genuinely Intriguing. Here is the elegant part of the bull case. Right now, the global graphite market in 2025 is facing an oversupply situation, with China accounting for nearly all recent supply growth and also dominating refining. Needle coke prices are depressed. Everyone is suffering — which is precisely the condition that creates extraordinary future opportunity. Think about what happens when EAF adoption continues to accelerate, and EV battery demand continues to grow: both industries compete more intensely for the same raw material — needle coke. The two demand curves converge on the same supply source. If EAF adoption is as rapid as the structural data suggests, and if battery demand grows at even a fraction of the projected rate, then needle coke — currently oversupplied and cheap — faces a structural shortage that could push prices dramatically higher.

And who benefits most from a needle coke price spike? Theoretically, a company that owns its own needle coke production and can insulate its electrode manufacturing from input cost inflation. That company is Graftech.

The Competitive Moat Has Real Substance. Only a very small number of companies in the world can produce high-grade petroleum needle coke consistently. The precise control of what’s called “mesophase management” — the behavior of liquid crystals during the coking process — is an art form that requires specific operating conditions, highly experienced operators, and proprietary process knowledge that cannot simply be reverse-engineered. Feedstock scarcity further compounds this barrier: high-quality needle coke requires highly aromatic, low-sulfur, low-metal feedstocks like FCC decant oil, which are geographically concentrated and not universally available. Building greenfield needle coke production outside of China has remained essentially flat for many years precisely because of these capital, technical, and permitting barriers. Graftech’s Seadrift facility in Texas is one of very few operations in the Western world capable of this.

Graftech is the only large-scale graphite electrode producer that is substantially vertically integrated into petroleum needle coke, giving it the structural position of the lowest-cost producer. That is a meaningful, genuine moat — the kind Charlie Munger would describe as “hard to replicate.”

So What Is the Implied Prize? Let’s think about customer economics for a moment. A graphite electrode is what finance people call a “consumable” — it gets eaten up during the steel-melting process, lasting only 5 to 8 hours of furnace operation. This is an extraordinary economic feature. Electrode replacement cycles occur every 8 to 10 hours of melting, necessitating high working capital for electrode inventories. Your customers cannot avoid buying from you. There is no “skip this quarter” option when you’re melting steel. The lifetime gross profit from a single large steel mill customer — locked in by switching costs from ArchiTech (Graftech’s advanced furnace monitoring platform) and by the mission-critical nature of the product — is enormous relative to the cost of winning that customer.

Projections suggest the graphite electrode market could grow from $11.60 billion in 2025 to $16.68 billion by 2033, with UHP electrodes — Graftech’s specialty — leading the charge. Against a current market cap of roughly $220 million (at the time of my analysis), the implied upside from a market recovery is genuinely startling. If the cycle turns and Graftech can return to even a fraction of the margins it earned during the 2018 supercycle — when revenues were $1.8 billion and the stock was a multi-bagger — the return from current levels would be extraordinary. The birds in the bush are plentiful, enormous, and real.

And yet…

Section II: How Sure Are You?

The second question is the hardest. It is not enough to identify a beautiful potential outcome — you must assess the probability that the path from here to there is navigable, and whether the company can survive long enough to walk it. This is where the Graftech thesis begins to fracture, not because the long-term story is wrong, but because the near-term reality is far uglier than most people appreciate.

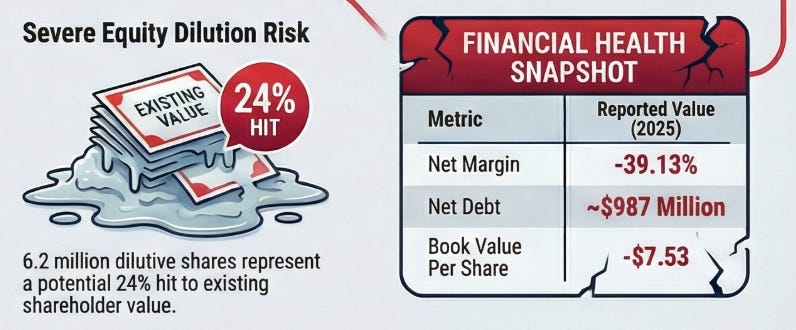

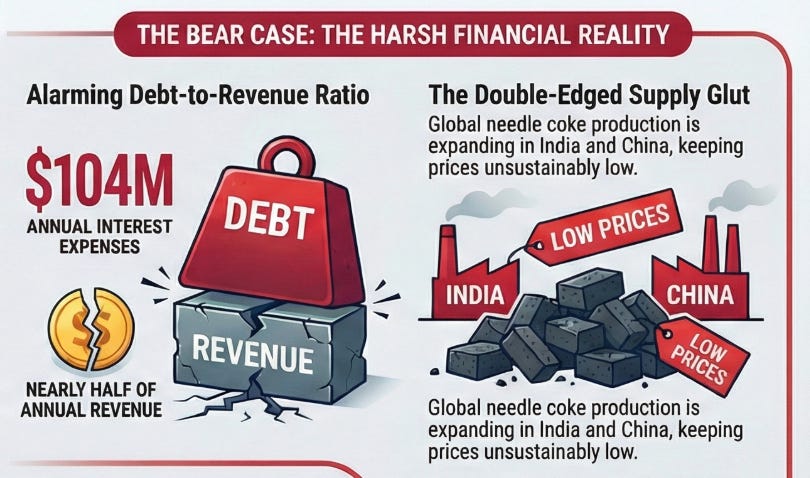

The Financials Are Genuinely Alarming. Let’s start with the numbers, because no amount of narrative substitutes for arithmetic. Revenues have collapsed from $1.8 billion in 2018 to $504 million in 2025, with net debt ballooning to $987 million and negative EBITDA. The company posted a full-year net loss of over $219 million in 2025 — more than its entire market capitalization at the time of my analysis. Gross debt stands at $1,125 million, with net debt around $987 million. Interest expense alone reached $104 million in 2025. Let that sink in: the company’s interest bill is approximately half of its annual revenue. And it’s still burning cash.

The operating margin stands at -12.03%, the net margin at -39.13%, and the Beneish M-Score of 4.65 suggests potential issues warranting additional scrutiny. The company had to undergo a 1-for-10 reverse stock split in 2025 to avoid delisting from the NYSE — a signal that, whatever management says in earnings calls, the market has serious structural doubts about the equity. A reverse split does not create value; it is a cosmetic procedure performed on a patient whose vital signs are deteriorating.

The Pricing Environment Is Getting Worse, Not Better. Management acknowledged in the Q4 2025 earnings call that pricing heading into 2026 is no better than the 2025 level — which was already at unsustainably low levels. The CEO noted that the problem is not demand — it’s supply. The supply imbalance is being driven by gross overcapacity built in both China and India, with Indian manufacturers expressing plans to bring additional capacity online. Even in the US market — where Graftech has 65% of its anticipated 2026 order book already committed and where pricing is strongest due to tariff protection — the company conceded pricing direction is negative.

This matters enormously because Graftech is trying to raise prices on uncommitted volumes by approximately 15%, while simultaneously its net loss is running at approximately 25% of revenues. You cannot price your way out of this arithmetic without a simultaneous and dramatic improvement in the demand/supply balance for electrodes. That improvement is not on the horizon in the near term.

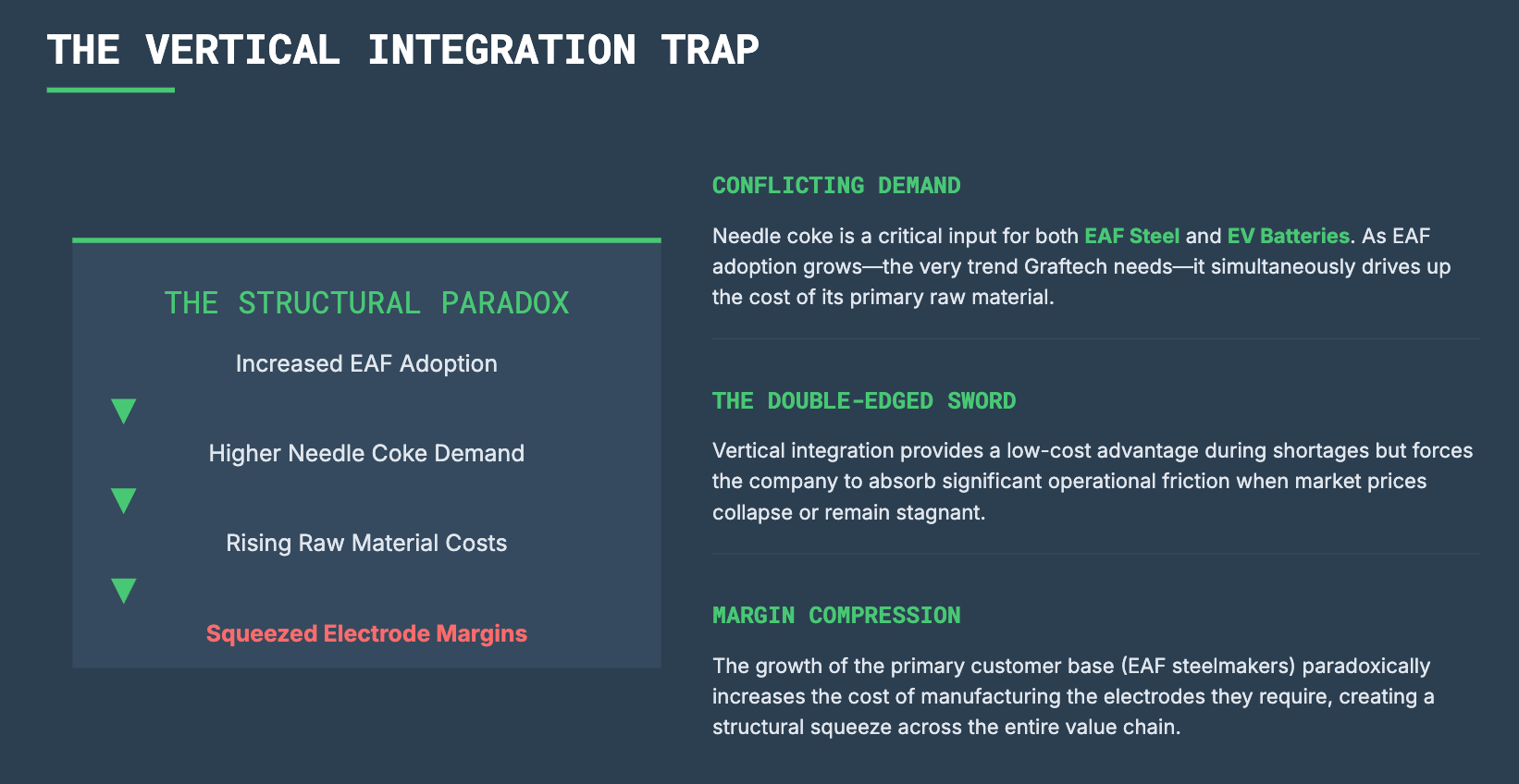

The Vertical Integration Is a Double-Edged Sword That Is Currently Cutting the Wrong Way. This is perhaps the subtlest and most important insight in this analysis, so bear with me.

When needle coke prices are high due to a supply shortage, a vertically integrated producer like Graftech benefits: it controls its own input cost, can produce electrodes cheaper than competitors who must buy needle coke on the open market, and earns margin on both ends of the supply chain. This is the dream scenario.

But when needle coke prices are low due to oversupply — which is the exact situation right now — the calculus reverses. Here is why: Graftech’s Seadrift facility has a fixed cost structure. It must keep operating to maintain the technical know-how and the condition of the plant. Those costs don’t go away when needle coke spot prices collapse. Meanwhile, Graftech’s customers for graphite electrodes could theoretically go to the open market and buy cheap needle coke from Chinese or Indian producers, then have it processed by a competitor without the burden of an in-house production facility. Graftech, paradoxically, is stuck with its own supply chain. Its vertical integration — designed as a cost advantage — becomes a cost anchor in a world of needle coke oversupply.

Think of it like an oil company that also owns gas stations. When oil prices are high and gas demand is strong, that integration is a machine for printing money. But when oil is oversupplied and gas margins are compressed at the pump, the upstream division is losing money and the downstream division is also losing money, and the integration compounds both problems rather than buffering them. While Graftech’s vertical integration into needle coke offers a significant competitive advantage by ensuring supply and potentially diversifying into the EV battery market, the company’s profitability is severely hampered by oversupply and intense pricing pressure. The same sword cuts both ways.

The Supply Glut Is Not Clearing — It Is Growing. The bull thesis requires that competitors exit the needle coke market, supply contracts, and prices recover. There is one data point that supports this view: Mitsubishi Chemical decided to exit the needle and pitch coke business entirely by 2027, pushed out by Chinese competition. That is one exit from a market with many participants. But look at what is simultaneously happening on the other side of the ledger:

Indian Oil Corporation (IOCL) is adding 56,000 tonnes per annum of calcined needle coke capacity at its Paradip refinery. TAQAT/Chevron Lummus is developing a 75,000 TPA needle coke and synthetic graphite complex in Saudi Arabia. A Chinese firm, Zhongyi Future, is investing $1.49 billion in a massive new needle coke carbon material project. EAM/Phillips 66 is developing a 60,000 TPA graphite anode plant in the US and expanding in Finland and India. Gazprom Neft is commissioning a new 31,000 TPA coker at its Omsk refinery. For every exit from the market, there appear to be two or three new entrants. This is what a supply glut that is getting worse looks like — not one that is clearing.

China is projected to control roughly 80% of battery-grade graphite production through 2035, and its capacity expansion in needle coke is driven by its insatiable appetite for EV battery anodes. The Western hope that Chinese supply will be restricted by tariffs or geopolitics is real but unreliable — trade policy is notoriously volatile, and any US-China trade détente can rapidly upend a thesis that depended on tariff walls.

The Dilution Risk Is Significant and Underappreciated. One of the less-discussed but mathematically important aspects of the Graftech situation is its equity dilution pipeline. The company has approximately 6.2 million dilutive shares sitting in unvested RSUs, PSUs, DSUs, and stock options — against a total current share count of 25.7 million. That represents roughly 24% potential dilution from compensation alone, before any consideration of future equity raises. Given that the company cannot raise more debt (it is already carrying $1.1 billion in debt against negative book value — book value per share is -$7.53), any future capital need must come from equity. The existing shareholders will be diluted.

Moreover, given the current situation where additional financing is imminent, the equity value might be diluting further.

The Accounting Deserves a Second Look. Graftech defers maintenance costs for equipment over periods of up to 20 years — a practice that flatters current earnings but is questionable in an industry moving as rapidly as the graphite and battery materials space. Equipment that was state-of-the-art a decade ago may be technically obsolete before the 20-year depreciation window closes, given the pace of technological development in electrode manufacturing driven by EV battery demand. Additionally, the company includes direct labor costs in its inventory valuation — a practice that, while technically permissible under GAAP, inflates the apparent value of inventory and disguises the true intrinsic value of the business. These are not fraudulent practices, but they warrant skepticism when you’re trying to understand the real cash economics of the operation.

Deferred maintenance cost for equipments (in my opinion) is deferred for too long of a period — 20 years. Equipments will likely become obsolete by then due to the fact that the graphite industry is moving extremely fast because of battery demand and hence competition.

The Beneish M-Score. A Beneish M-Score of 4.65 suggests potential financial manipulation. For context, an M-Score above -1.78 is typically flagged as a potential earnings manipulation signal. A score of 4.65 is well into the red zone. This does not mean fraud is occurring — the score can be triggered by legitimate accounting practices under stress — but it means an investor needs to look more carefully at the quality of reported earnings, which in this case are already deeply negative. The signal reinforces rather than creates concern.

Section III: How Long Till You Get Them Out?

The third question is about time. Even a correct thesis can destroy your portfolio if the timeline is wrong, because capital has a cost — not just the opportunity cost of what else you could own, but the real psychological and financial cost of watching a position bleed while you wait for the world to catch up to your analysis. The question of when the thesis resolves is often as important as whether it resolves at all.

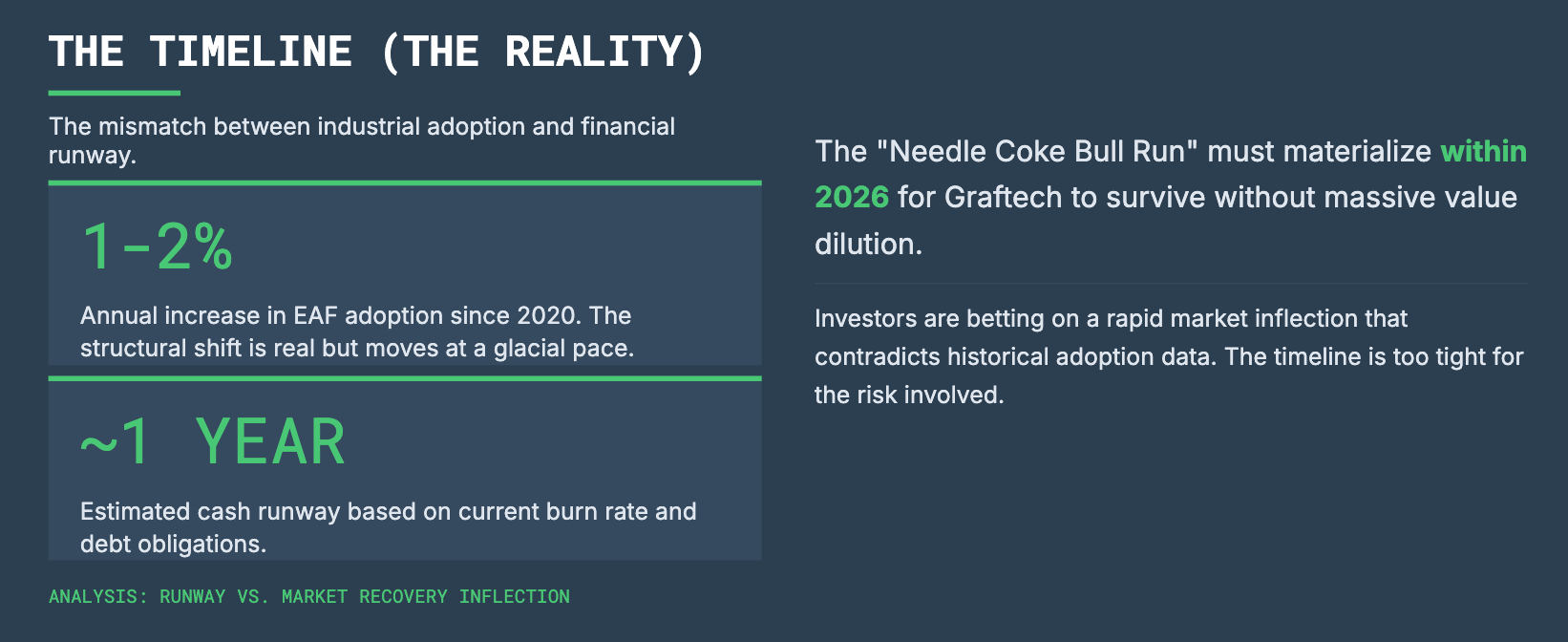

The Runway Is Alarmingly Short. With $340 million in total liquidity including $138 million in cash and gross debt of $1,125 million — with no major debt maturities until December 2029 — the company has bought itself some time. Management’s narrative is that the 2029 debt wall gives them room to navigate. But let’s do the cash flow math. Operating cash flow was approximately -$40 million in 2024 and has not meaningfully improved. Free cash flow was approximately -$74 million. Interest expense is $104 million annually. If current conditions persist — pricing flat or declining, volumes modestly growing — the company’s $340 million liquidity position could be consumed within one to two years without external financing.

The needle coke “bull run” that would rescue the economics of this business needs to arrive before the cash runs out. It needs to arrive not just eventually — but specifically within the next 12 to 24 months. And based on all available supply-side data, that is not looking likely. The market is adding capacity, not contracting it.

EAF Adoption Is Moving in the Right Direction, But Too Slowly. The long-term data on EAF adoption is unambiguously positive. EAF steelmaking emits up to 70% less CO₂ than traditional blast furnace methods, and China has banned new coal-based steel projects. But the pace of adoption tells a more sobering story for the near term. EAF’s share of global steel output moved from roughly 30% in 2020 to about 32% in 2025 — a gain of only two percentage points over five years. The structural transition is real. The speed of that transition, at the installed plant level, is constrained by the enormous sunk cost of existing blast furnace infrastructure, the political economy of shutting down blast furnaces (which are deeply tied to regional employment and national identity in countries like China, Japan, and India), and the capital intensity of building new EAF capacity.

The demand uplift that would consume enough needle coke to create a shortage — the core mechanism of the Graftech recovery thesis — is probably 5 to 10 years away at the current pace of adoption. That is not a timeline that is compatible with a company that may have 12 to 24 months of runway under current conditions.

The Competition Problem Has No Near-Term Resolution. In the Q4 2025 earnings call, CEO Timothy Flanagan noted that the company is operating in “one of the most challenging environments the graphite electrode industry has seen in almost a decade” — marked by global overcapacity, aggressive competitor behavior, geopolitical uncertainty, and subdued steel production in many regions. This is not a cyclical trough that will naturally clear in a quarter or two. Overcapacity in commodity industries is notoriously sticky — producers keep running plants even at losses because the fixed cost of shutting down is high and the hope of recovery keeps management teams optimistic. The graphite electrode market has the additional complication of Chinese and Indian state-supported producers who can operate at losses indefinitely because their governments view steel industry infrastructure as a strategic asset.

In Q2 2025, UHP graphite electrode prices in China were around $2,140 per metric ton — compared to $4,230 per metric ton in the United States. The gap between Chinese and Western pricing is nearly 2x, and Chinese producers are aggressively trying to capture Western market share despite the tariff friction. Even with tariff protections, the pricing pressure on Graftech’s non-US business is severe.

The Customer Lifetime Value Calculation Is Impaired. We mentioned earlier that graphite electrodes are consumables with an attractive recurring revenue profile — your customers must keep buying from you as long as they’re running their furnaces. In a functioning business, this translates into a powerful customer lifetime value (LTV) dynamic: a steel mill that installs ArchiTech (Graftech’s proprietary furnace management system) creates a high-switching-cost relationship that effectively locks in multi-year electrode procurement. The customer acquisition cost (CAC) to win a large steel mill is significant — technical demonstrations, integration of monitoring systems, pricing negotiations — but the lifetime gross profit from a locked-in customer running multiple furnaces around the clock is extraordinary.

The problem is the denominator of that LTV/CAC equation: the gross profit per tonne of electrodes sold. Right now, Graftech’s gross margin is -3.68%. The lifetime gross profit from each customer is negative. You are burning cash to retain customers and burning cash to produce the product. When your unit economics are inverted, volume growth makes things worse, not better. Selling more electrodes at a loss simply accelerates the cash burn. This is why the 6% increase in 2025 sales volume — which management celebrated — failed to move the needle on profitability.

The Reverse Stock Split Is a Bad Omen. It is worth pausing on the 1-for-10 reverse split Graftech executed in August 2025. The proximate cause was the threat of NYSE delisting due to the stock trading below $1.00. Management framed it as a technical compliance measure. But the history of reverse stock splits in distressed companies is not encouraging. Academic research on reverse splits consistently shows that they are associated with continued underperformance in the subsequent 12 to 36 months, because the underlying problems that caused the stock to fall to penny territory don’t disappear by multiplying the share price by 10. They just become less visually offensive.

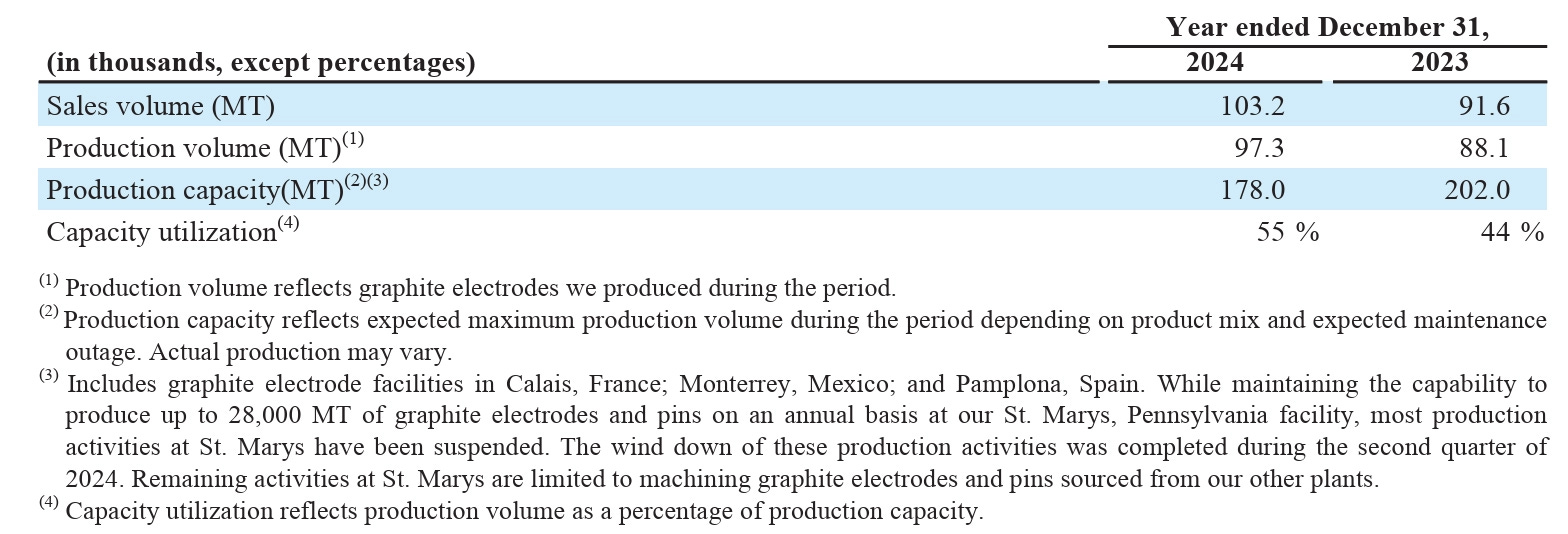

Simultaneously, the company had to cut back on production capacity due to losses. As of 2025, production capacity was approximately 178 thousand metric tons, with primary manufacturing facilities in Calais, Pamplona and Monterrey. The production capacity was reduced from 202 thousand metric tons as the increased cost resulted in the company having to (indefinitely) suspend the production activities of their pennsylvania (St Marys) facility. In shorts, despite the weak outlook, it is important to take note that the company currently is not performing at full capacity (currently only performing at about 55% of its max capacity).

What Would Change My Mind? I want to be fair. The scenario in which this investment works is not impossible — it is just highly dependent on a specific chain of events that I cannot estimate with sufficient confidence:

First, graphite electrode prices would need to rise substantially — not 15% as currently planned, but something like 40% to 60% — driven by a combination of tariff escalation against Chinese and Indian imports and a faster-than-expected increase in Western EAF utilization. Second, the needle coke market would need to tighten — specifically, the Chinese capacity expansion directed at the EV battery market would need to consume so much needle coke that the supply available to the graphite electrode segment contracts significantly. Third, Graftech would need to sustain operations through this transition without diluting shareholders through a distressed equity raise or defaulting on its debt obligations.

Each of those conditions is plausible individually. All three occurring simultaneously, within the next 12 to 24 months, is not a bet I can make with confidence.

Conclusion: The Bird in the Hand

There’s an old saying that a bird in the hand is worth two in the bush. What the saying doesn’t tell you is how to count the birds in the bush, how sure you are they’re really there, and how long it will take to catch them. Those are the three questions that this analysis is built around, and they are the three questions that Graftech fails.

The birds in the bush are real and genuinely numerous — the long-term tailwinds for EAF steelmaking, the needle coke supply thesis, the Western geopolitical realignment away from Chinese materials, and the unique position of a vertically integrated, technically sophisticated producer in a market with high barriers to entry. I believe in that story. It is not a fiction.

But my confidence in the path from here to there is insufficient. The company’s financial position is fragile — $987 million in net debt against negative book value, $104 million in annual interest expense, negative gross margins, and a runway that gets shorter with each passing quarter. The supply side of the needle coke market is expanding, not contracting. EAF adoption is real but happening at a glacial pace relative to the speed at which Graftech’s cash is being consumed. The vertical integration that represents the company’s crown jewel is, in the current environment, functioning more like a millstone than a moat.

With revenues having collapsed from $1.8 billion in 2018 to $504 million in 2025, and negative EBITDA, this is not a company that can wait indefinitely for its moment. The clock is ticking.

The investment might work if you are willing to accept that this is, at its core, a call option on a very specific commodity supercycle materializing within a very specific and compressed time window. Some investors are excellent at that kind of trade. I am not one of them — my circle of competence does not extend to forecasting commodity cycles with the precision that this play requires. And as Charlie Munger once said, knowing the edge of your competence is at least as important as having competence itself.

So I pass. Not because Graftech is a bad company. Not because management is dishonest. Not because the macro thesis is wrong. I pass because the three questions — how many birds, how sure, how long — do not all return satisfactory answers simultaneously. And in investing, a chain is only as strong as its weakest link.

The most important decision in a thesis like this is knowing when not to pull the trigger — even when the story is beautiful, the setup looks compelling, and insiders are buying. The vertical integration was designed to be Graftech’s greatest strength. In the current environment, it is designed to make the company fail. That dissonance is not a reason to be pessimistic about the long-term story. It is a reason to wait.

I’ll watch. I’ll revisit. If the needle coke supply picture tightens meaningfully — if EAF adoption accelerates faster than current data suggests — I will look again. But right now, I’d rather own a bird I can hold than chase two in a bush I can’t see into clearly.

All data points sourced from Graftech’s public filings, Q4 2025 earnings call transcript, GuruFocus, Seeking Alpha, Mordor Intelligence, IMARC Group, and Investing News Network. This article represents the author’s personal analysis and is not investment advice. Do your own due diligence.