Rust, Rigs, and the Recurring Revenue Hidden in Plain Sight: A Deep Dive into Beng Kuang Marine (SGX: BEZ)

Analysis date: 17 March - 23 April 2026

The Old Steel and the Sea: Why You Should Care About a Ship Maintenance Company

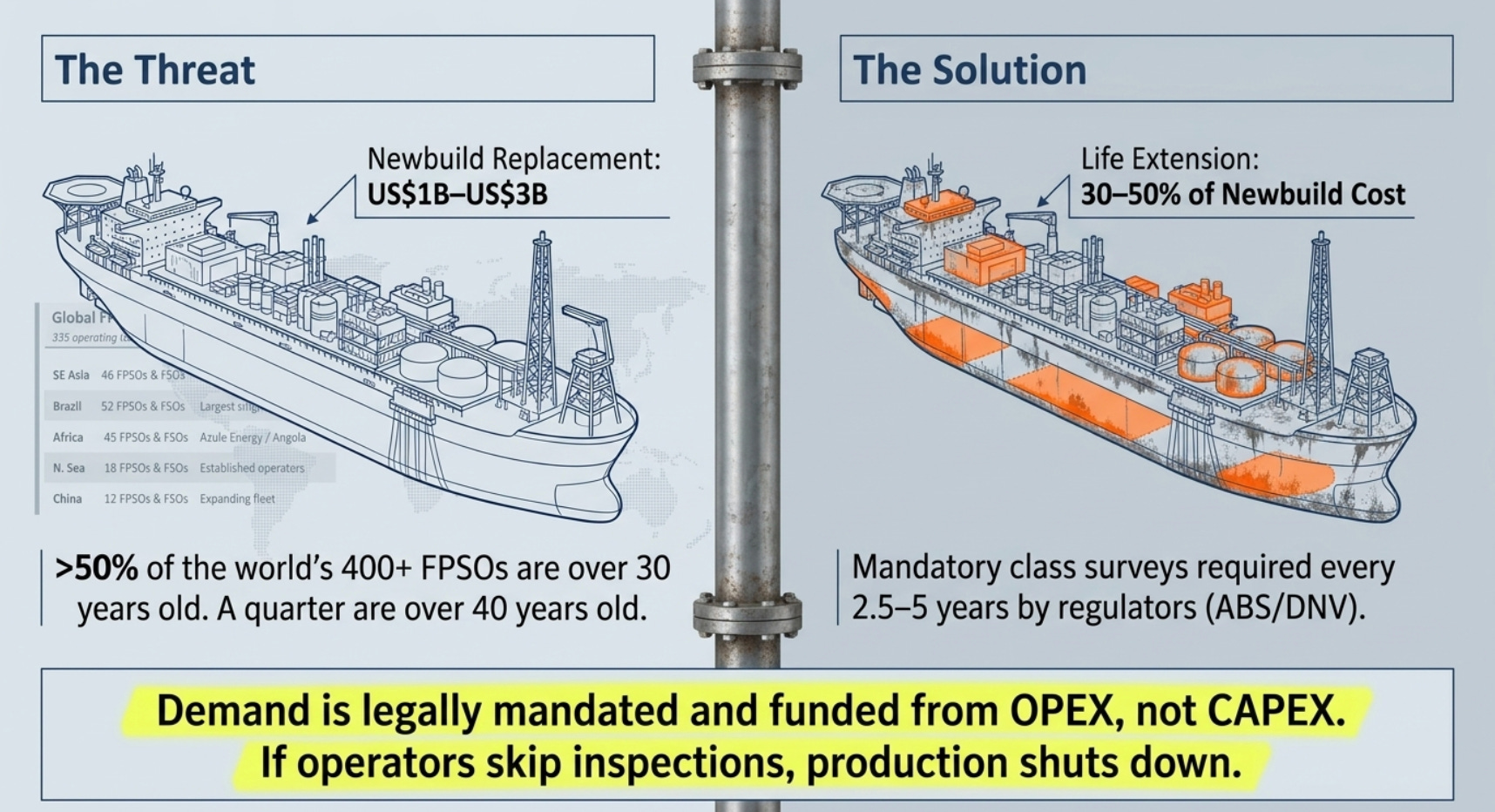

There is an image I want you to hold in your mind. Somewhere off the coast of Angola, in the South Atlantic, a floating city of steel sits anchored in water so deep that if you dropped a mountain into it, the peak would never break the surface. This floating city — a Floating Production, Storage and Offloading vessel, or FPSO — produces tens of thousands of barrels of oil every single day. It has been doing so for over thirty years. The steel on its hull is weathered. Rust has begun its silent negotiation with the structure. The operators of this vessel face a choice: spend a billion to three billion dollars building a new one, or spend a fraction of that — perhaps 30 to 50 percent — to send a small, specialized team out to repair and certify the old one while it continues producing.

This is not a romantic metaphor. According to data from the American Bureau of Shipping (ABS), more than half of the world’s FPSOs are over 30 years old, and a quarter are over 40 years old — and ABS classes nearly 60% of this niche fleet. The challenge of maintaining and extending the life of these aging giants is not optional. It is legally mandated. If you skip the inspection, regulators shut down production. If you ignore the corrosion, the consequences can be catastrophic. The maintenance is not discretionary. It is as inevitable as a dentist’s appointment, except the patient is a multi-billion dollar oil-producing machine, and missing the appointment means losing hundreds of millions of dollars in daily production revenue.

The company I want to tell you about makes its living precisely there — in that narrow, technically demanding, legally non-negotiable space between a rusting FPSO and the regulator’s deadline. It is called Beng Kuang Marine Limited, ticker BEZ on the Singapore Exchange. It is a $107 million market cap company that almost nobody is talking about. And even after everything I am about to tell you — the elegant business model, the sticky customers, the reasonable valuation, the structural tailwinds — I still said no to buying it. At least for now.

Here is the full story of why I find it fascinating, why I added it to my watchlist, and the exact thinking I used to hold myself back from pulling the trigger.

The Market That Nobody Sees Coming

Before we talk about the company, we need to understand the pond it swims in, because the size and nature of that pond is perhaps the most important thing an investor needs to verify before anything else.

There is a concept in investing I keep coming back to: the best businesses are not necessarily the ones doing the most exciting things — they are the ones solving problems that are inevitable, recurring, and difficult to replace. Think about elevator maintenance. Nobody gets excited about elevator maintenance. But if you own the elevator in a building, you have no choice but to maintain it. The law requires it. The insurance requires it. And because very few people are trained to maintain it, the elevator maintenance company has pricing power and customer stickiness that a restaurant or retailer can only dream of. This is the conceptual framework I want you to carry as we walk through Beng Kuang’s story.

Now apply that framework to FPSOs. The FPSO Life Extension Services market reached USD 1.46 billion globally in 2024, and is projected to grow at a CAGR of 6.8% through to 2033, reaching USD 2.84 billion — driven primarily by aging fleets and the cost advantage of life extension over replacement. The global FPSO market itself was valued at USD 30.63 billion in 2026, expected to reach USD 51.45 billion by 2035, growing at a CAGR of 7%. These are not trivial numbers. And within that growing market, the maintenance and life-extension segment is the most structurally protected part, because unlike new builds — which get cancelled when oil prices fall — maintenance is funded from operating budgets, not capital budgets. Oil companies can defer building new FPSOs. They cannot legally defer inspecting the ones already producing.

Since regulatory bodies like ABS and DNV mandate inspections and repairs every 2.5 to 5 years to prevent production suspensions, ASOM enjoys “sticky,” recurring demand regardless of the broader economic climate. This is the economic architecture underneath Beng Kuang. The business does not need to win new customers to survive. It needs its existing customers to keep using their existing assets. And those assets are aging. Every single year, the world’s FPSO fleet gets older. Every single year, the mandatory inspection cycle ticks closer. Every year that a customer defers, the cost and urgency of the work increases. Beng Kuang does not market to create demand. Demand arrives on its own, driven by physics, chemistry, and the law.

A Company That Nearly Destroyed Itself, Then Found Its Mind

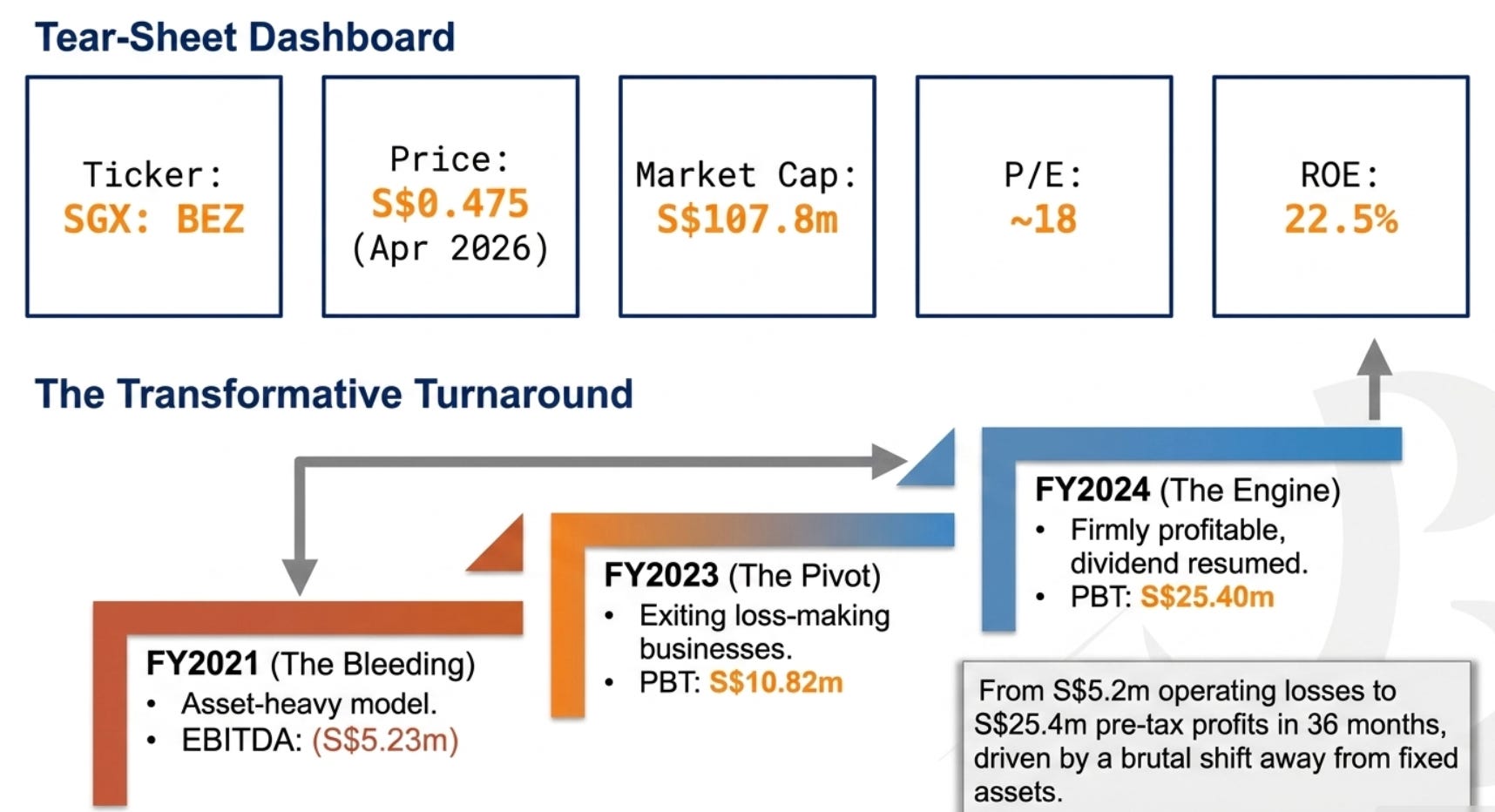

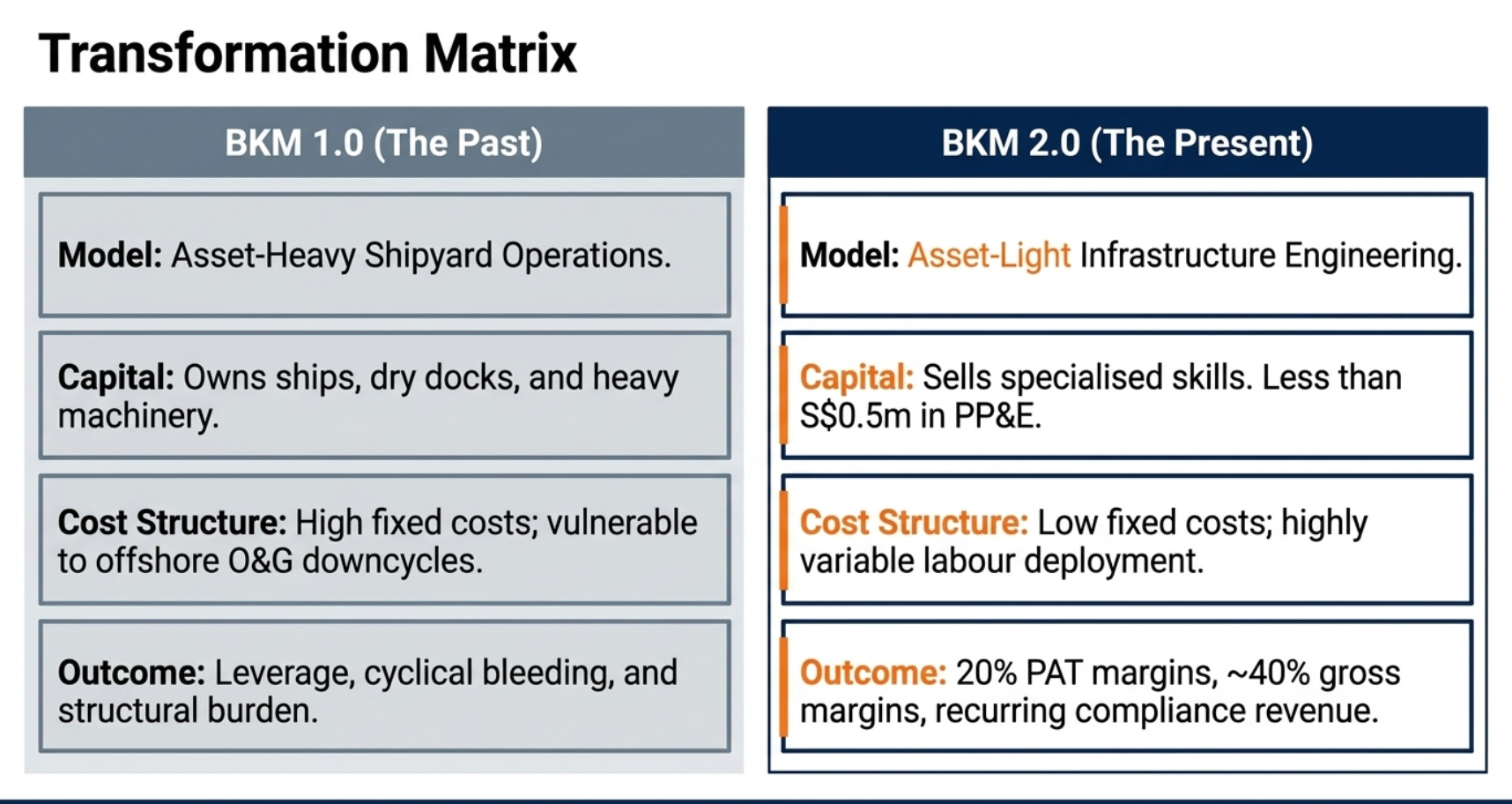

Understanding where Beng Kuang is today requires understanding where it nearly ended up. The company was founded in 1994 and has been listed on the SGX since 2004. For much of its early history, it was what you might call a capital-intensive shipyard business — the kind that requires large amounts of equipment, property, and labor to generate revenue, and which suffers enormously when the offshore oil and gas cycle turns against it. And turn against it, it did. By the early 2020s, the company was loss-making, leveraged, and carrying the heavy structural burden of an asset-heavy model that no longer made economic sense in a cyclical industry.

Then, in 2021, something happened that changed the company’s trajectory completely. Ever since CEO Yong Jiunn Run took the helm at Beng Kuang Marine in 2021, he has turned a loss-making, leveraged shipyard operator into a profitable, asset-light O&M provider. Under the BKM 2.0 strategy, BKM has shifted away from capital-heavy shipyard operations toward higher-margin, recurring services.

I want you to think about what this transformation actually means in business terms, because it is not just an operational change — it is a fundamental rethinking of what the company is. The old Beng Kuang owned things: ships, equipment, dry docks. Owning things is expensive. It requires constant capital reinvestment, generates debt, and creates operating leverage that punishes you during downturns. The new Beng Kuang sells skills and expertise — things you cannot buy on Amazon and cannot easily replicate. You deploy a team of specialized engineers and technicians to an FPSO in Angola, you do the work, you charge for the work, and you come home. The capital expenditure is minimal. The return on invested capital is high. When projects slow down, you redeploy your crew. You do not carry the crushing fixed costs of idle machinery.

This transformation is visible in the numbers. In FY2021, the company reported revenue of S$51.31 million with a gross profit of S$11.90 million and an EBITDA of negative S$5.23 million — it was losing money at the operating level. By FY2024, revenue had grown to S$111.88 million, gross profit to S$38.73 million, and profit before tax to S$25.40 million. That is a company that went from bleeding to generating strong, recurring profitability in just three years — and it did it without buying a single new ship.

What I found refreshing, and what I consider a genuine green flag in a world full of management teams that bury bad news in footnotes, is that Beng Kuang’s management explicitly identifies and separates one-off gains in their reporting. They do not try to pass non-recurring income off as operating performance. They call it out. This is the behavior of a management team that respects its shareholders and believes its recurring business is strong enough to stand on its own.

The Business Model: Thinking About Customer Acquisition Cost and Lifetime Gross Profit

Most retail investors look at P/E ratios. Experienced investors look at unit economics. Let me show you how to think about Beng Kuang’s business through that lens, because it reveals something structurally interesting.

The key question for any service business is: how much does it cost to acquire a customer, and once you have them, how much gross profit do they generate over the lifetime of the relationship? This is the Customer Acquisition Cost (CAC) versus Lifetime Gross Profit framework. And in Beng Kuang’s case, the economics are quietly extraordinary.

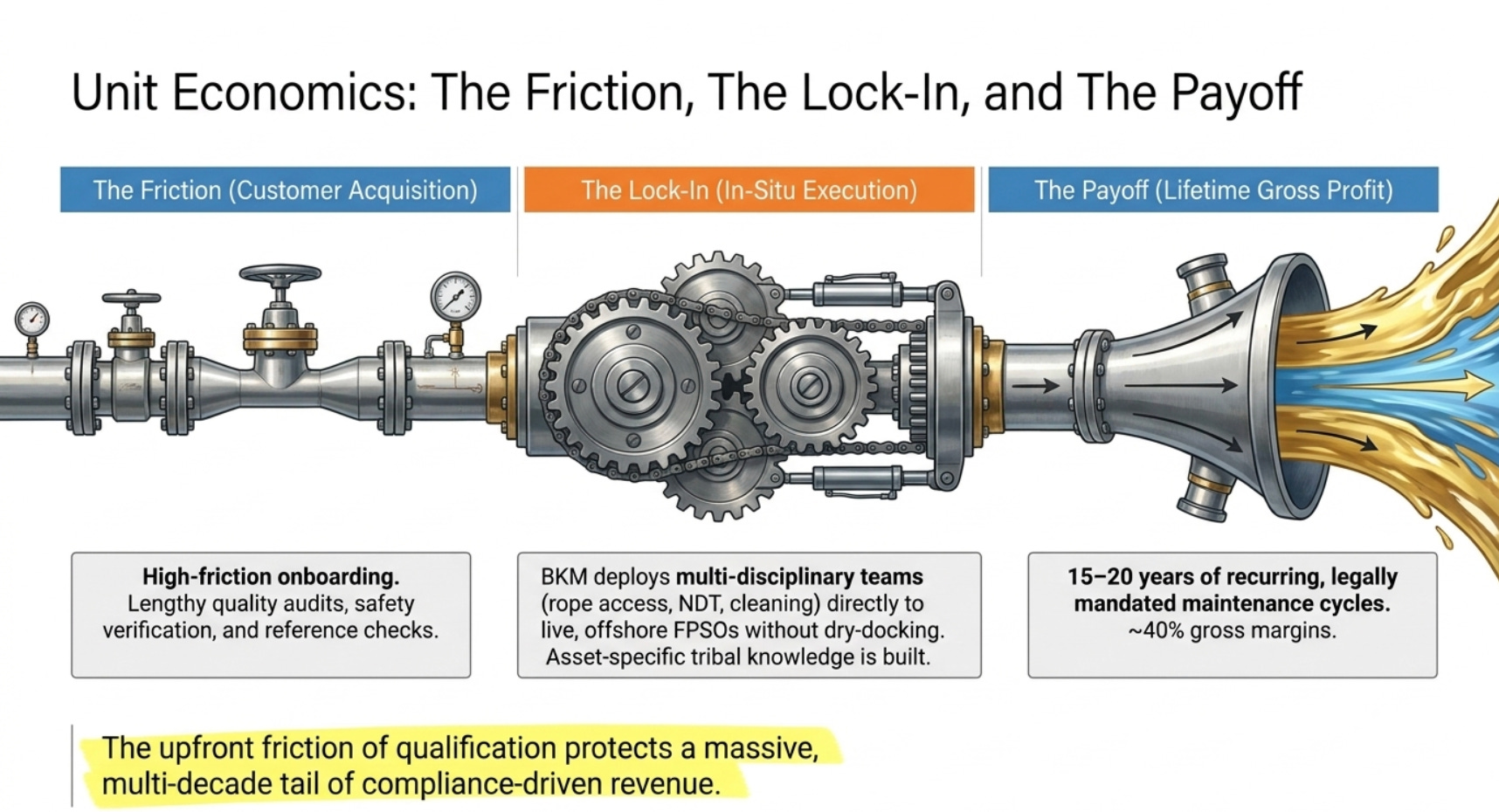

Think about what acquiring a customer actually looks like for this business. An FPSO operator — say MODEC, or BW Offshore, or SBM Offshore — brings Beng Kuang on to service one of their vessels. There is a lengthy and expensive qualification process involved in becoming a certified vendor for a safety-critical offshore asset. Engineers are assessed. Quality management systems are audited. Safety records are verified. Reference projects are reviewed. This onboarding process takes time, costs both parties money, and builds an information relationship — the service provider learns the specific peculiarities of that vessel, the access points, the corrosion patterns, the history of previous repairs. That knowledge lives in the heads of the engineers who did the work, and it is not easily transferable.

Here is where the economics flip in Beng Kuang’s favor: once you are in, switching costs are enormous. And I do not mean “enormous” in the vague qualitative sense that consultants use. I mean structurally enormous — the kind embedded in regulation, safety culture, and asset-specific tribal knowledge that takes years to accumulate. Being an asset-light player, PAT margins stand in the 20% range and gross margins in the low 40% range, with less than $0.5 million in PPE. That is remarkable capital efficiency. You are generating 40% gross margins from a business with virtually no fixed assets.

Now, an FPSO has a design life of 20 to 30 years, with operators routinely extending them further through life-extension programs. ASOM supports more than 20 offshore floating assets globally, within a structurally aging FPSO fleet. If each asset requires mandatory inspections every 2.5 to 5 years, and Beng Kuang is the embedded resident contractor, then a single asset relationship could generate contract revenue repeatedly over the remaining life of that vessel. Assuming an average contract engagement value of several million dollars per inspection or maintenance cycle, and multiplying that across recurring mandatory cycles over a 15 to 20 year remaining asset life, the lifetime gross profit from a single FPSO relationship is potentially tens of millions of dollars from a customer they will almost certainly retain — because the switching costs make replacement expensive, risky, and disruptive. The CAC, relative to this lifetime value, is minimal.

This is what a good business looks like. Not viral growth or explosive revenue multiples. Just a deeply embedded, hard-to-displace service with a legally mandated demand cycle and gross margins that would make many SaaS companies envious.

ASOM: The Crown Jewel Hidden in Plain Sight

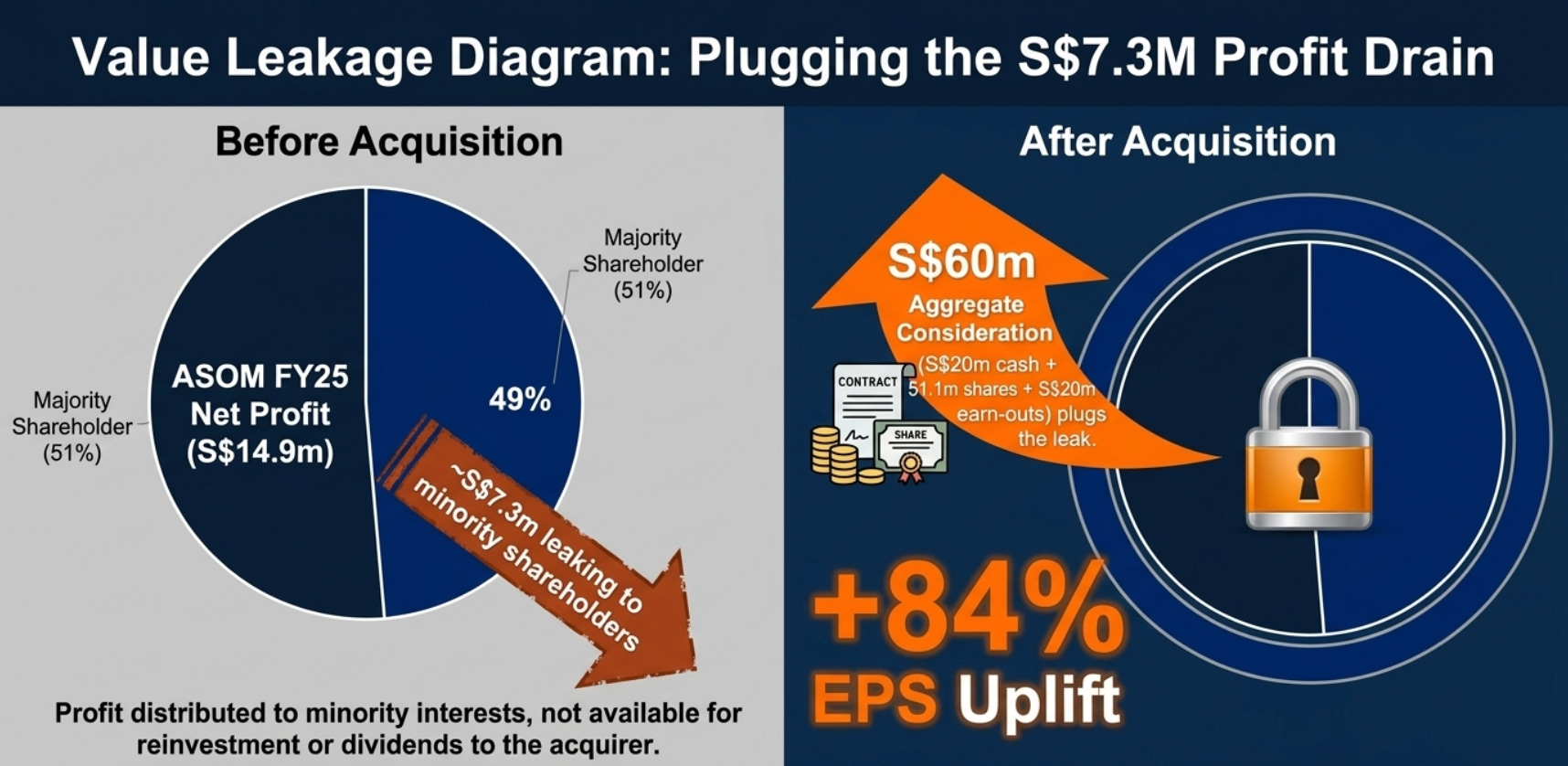

If Beng Kuang’s Infrastructure Engineering division is the engine of the business, then ASOM — Asian Sealand Offshore and Marine — is the engine inside the engine. And for most of Beng Kuang’s recent listed history, 49% of ASOM’s earnings were leaking out to minority shareholders who were not Beng Kuang.

ASOM is a specialized team that goes to FPSOs while they are still offshore — while the vessel is producing oil, in international waters, potentially in technically and logistically challenging locations like West Africa or South America — and repairs them. No dry docking. No bringing the vessel home. They do the inspection, the structural repair, the corrosion mitigation, the NOBA tank cleaning, the nitrogen leak testing — all of it, in situ. This is technically demanding work that requires multi-disciplinary teams with specific certifications, specific equipment, and specific experience on specific asset types. BKM can quickly demobilise and redeploy crews with minimal fixed-cost burden, allowing it to preserve margins and remain flexible during temporary slowdowns. This operational agility — the ability to move people without moving assets — is the structural advantage of the asset-light model made concrete.

The numbers behind ASOM are striking. Looking at the three-year financial history disclosed in the acquisition documents, ASOM reported revenues of S$50.55 million in FY2023, growing to S$86.27 million in FY2024, before declining to S$75.21 million in FY2025 due to operational timing delays — not structural customer loss. Gross profit over the same period was S$18.18 million, S$31.67 million, and S$30.15 million respectively. Profit after tax was S$10.04 million, S$19.33 million, and S$14.94 million. These are meaningful profitability numbers for a business that runs on people and expertise rather than capital equipment.

Beng Kuang’s decision to acquire the remaining 49% stake in ASOM for up to S$60 million, structured cleverly so that a significant portion of the acquisition cost is funded by ASOM’s own future earnings, changes the group’s earnings profile dramatically. In FY2025, 49% of ASOM’s S$14.9M net profit (c. S$7.3M) leaked to minorities. On a pro forma basis, the acquisition would have increased BKM’s EPS by 84% year-on-year from 2.61 cents to 4.80 cents. An 84% uplift in earnings per share from a single structural change — eliminating minority leakage — is not a trivial thing. It is a material rerating catalyst hiding inside an accounting footnote.

The acquisition price — valuing ASOM at approximately 8x FY2025 profit after tax for the entire business — is not cheap in isolation, but it is reasonable for a business with recurring, compliance-driven revenue, 40% gross margins, blue-chip clients, and the kind of embedded positioning that makes it structurally defensible. The deal is both earnings and valuation accretive. We see no teething issues given BKM’s initial stake, while the structure of the transaction is sound and current ASOM management remains incentivised to continue delivering for BKM.

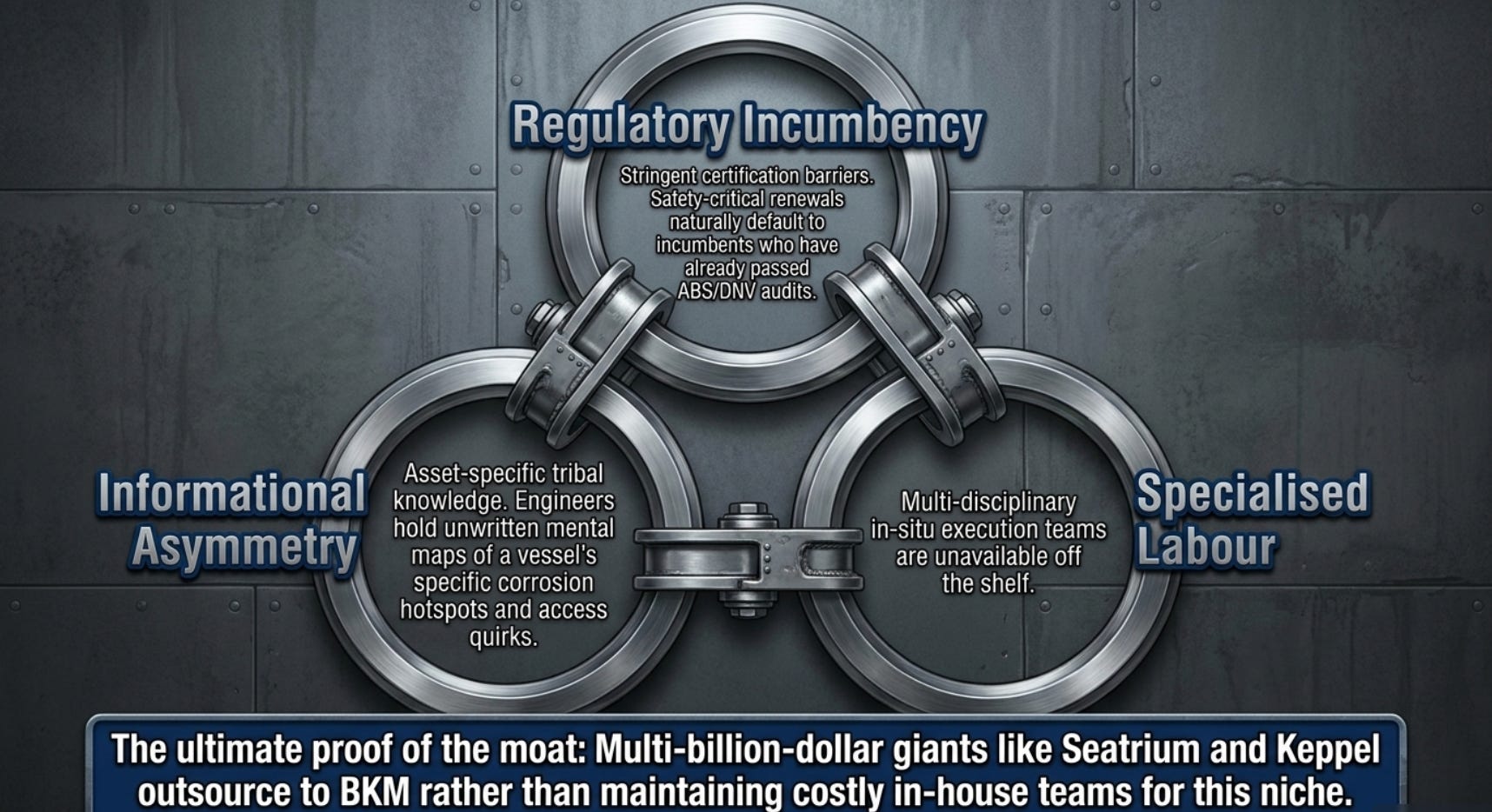

The Moat: When Trust Becomes a Balance Sheet Item

There is a famous Charlie Munger concept about the competitive advantage of businesses that are embedded in safety-critical supply chains. The idea is simple: when the consequences of failure are catastrophic — a plane falling from the sky, a ship flooding, an offshore rig exploding — the buyer of a service is not primarily optimizing for cost. They are optimizing for certainty. And certainty, built over years of successful execution in exactly the environments where failure is not forgiven, is not something a new entrant can acquire overnight.

The moat of Beng Kuang is precisely this. It has three interlocking components that reinforce each other.

The first is the switching cost created by asset-specific knowledge. When Beng Kuang’s engineers service a particular FPSO for the first time, they are building a mental map of that vessel — the access constraints, the corrosion hotspots, the history of previous interventions, the idiosyncratic challenges of that specific hull and topside configuration. This knowledge is not written in any manual. It lives in the experience of the people who did the work. A new contractor starting from zero would face a substantial learning curve on a safety-critical asset where learning curves are expensive and dangerous. The incumbent has an informational advantage that compounds every time the contract is renewed.

The second component is the regulatory and certification moat. International safety bodies like ABS and DNV do not certify just any team to perform inspection and life-extension work on operating FPSOs. Compliance resets structurally every 2.5 to 5 years, and contracts are typically renewed due to compliance requirements and incumbency. A competitor wanting to displace Beng Kuang would need to achieve the same certifications, the same references, the same track record on comparable assets. The cost and time required to build those credentials is itself a barrier. By the time a competitor earns the right to bid, Beng Kuang has already renewed the contract.

The third component is the labor moat — what I call the multi-disciplinary team that is not available off the shelf. You cannot hire specialized offshore FPSO maintenance engineers from a temp agency. This expertise is accumulated over years of field experience in specific environments. Beng Kuang’s ability to deploy multi-disciplinary teams — engineers who can do structural assessment, corrosion prevention, mechanical maintenance, NDT inspection, rope access work, and in-situ tank cleaning, all at once, on a live offshore asset — is a capability that takes years to build and is nearly impossible for a customer to replicate internally. This is why even organizations as large as Keppel and Seatrium, with their massive in-house engineering capabilities, outsource this work rather than building their own teams: the volume of work does not justify the cost of maintaining a permanent specialized force, and the margin for error does not permit using generalist engineers.

Beng Kuang has maintained relationships with clients for over 30 years. That is not a marketing statistic. That is proof that the switching costs are real.

The Capital Return Engine: How I Think About CRR

I use a metric I call Cash Reinvestment Rate, or CRR, as one of my primary tests of business quality. It is not a standard accounting ratio. The idea is simple: strip out non-recurring gains from net profit, divide the remaining normalized earnings by the net capital actually deployed in the business — working capital plus fixed assets — and you get a sense of how efficiently the business converts its invested capital into cash returns. A high CRR tells you the business has pricing power, low capital intensity, and strong unit economics. A low CRR tells you the business is consuming capital as fast as it generates it.

For Beng Kuang, the CRR calculation for FY2024 yields approximately 38%: taking net profit of S$21.1 million and subtracting S$8.2 million in one-off gains gives normalized earnings of S$12.9 million, divided by net invested capital of approximately S$33.5 million. For FY2023, the calculation yields 23%. Both figures are attractive — businesses generating 20-40% cash returns on invested capital are the kinds of businesses that compound value over long periods without requiring constant capital infusions. The CRR is improving as the BKM 2.0 strategy matures, which is the direction you want.

For comparison, think about a business like Microsoft’s Azure or Amazon’s AWS — the recurring, subscription-like nature of their revenue generates compound returns because each dollar of investment creates a perpetually renewing cash stream. Beng Kuang is not in that league of scale or growth velocity, but the structural logic is analogous: you invest in qualifying for and embedding within a client relationship, and that relationship generates recurring contract renewals driven by mandatory compliance cycles, not sales efforts. The CAC is front-loaded and one-time. The lifetime gross profit is recurring and multi-year.

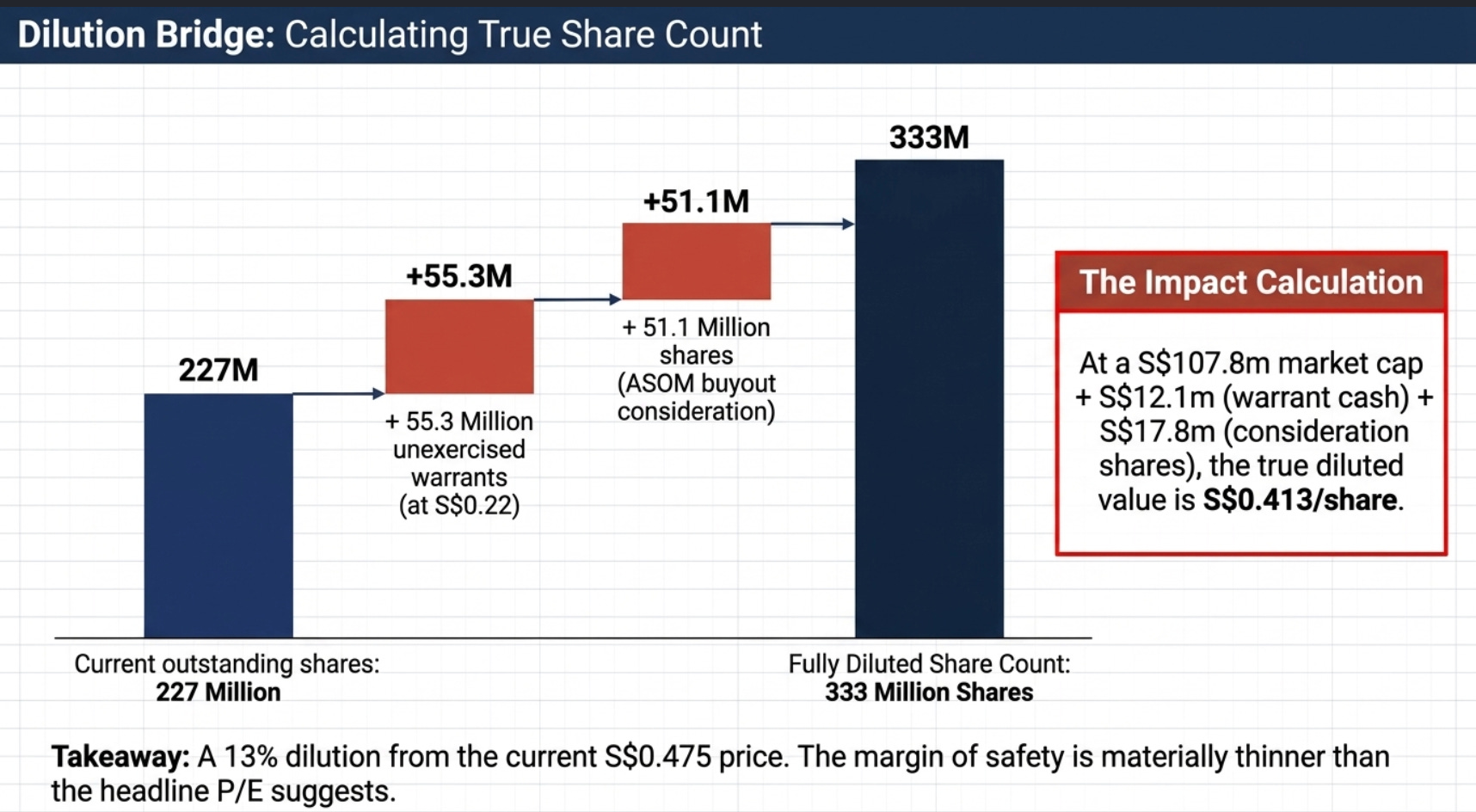

The Dilution Problem: Looking the Elephant Directly in the Eye

Here is where I have to slow down and be honest with myself, because this is the part of the analysis where the story gets less clean. Beng Kuang has a dilution problem. It is not a catastrophic one, but it is real and material, and ignoring it in the name of a compelling narrative would be exactly the kind of motivated reasoning that leads to expensive mistakes.

As of April 23, 2026, there are 227 million ordinary shares outstanding. There are also 55.3 million outstanding warrants exercisable at S$0.22 per share — a price well below the current trading price of S$0.475 — which means they will almost certainly be exercised, adding approximately S$12.1 million to the company’s treasury while issuing 55.3 million new shares. Additionally, the ASOM acquisition involves the issuance of approximately 51.1 million new consideration shares at S$0.35 per share. When I add all this up — current shares, warrant dilution, and ASOM consideration shares — the total diluted share count rises from 227 million to approximately 333 million shares.

On a fully diluted basis, assuming the current market capitalization of approximately S$107.8 million, the effective diluted market cap including all pending share issuances becomes approximately S$137.7 million (adding the S$12.1 million from warrant exercise and S$17.8 million from consideration shares at market), spread across 333 million shares. This implies a diluted value of approximately S$0.413 per share — a roughly 13% dilution to the current share price of S$0.475.

Thirteen percent dilution is not the end of the world, particularly if the acquisition it is partly funding is value-accretive. But it is a number you need to hold in mind. The question is not simply “is the business good?” but “is the business good enough to justify the price I am paying after full dilution?” And at S$0.475 per share — a P/E of approximately 18 on the core business before full ASOM consolidation, and a diluted value closer to S$0.413 — the margin of safety is thin.

What makes this more nuanced is that some of the dilution was genuinely structural and arguably necessary. The company issued a large tranche of warrants as part of the BKM 2.0 restructuring — not because the business model was failing to generate cash, but as part of the capital restructuring that funded the transformation from asset-heavy to asset-light. In that context, the dilution is the cost of the turnaround, not evidence of a business that cannot fund itself.

The harder question, which I think the market has not yet fully answered, is whether the future dilution risk is structural or temporary. I identify three conditions under which further dilution becomes likely: the business requires liquidity for working capital because its cash conversion cycle is lumpy (which is true for project-based service businesses operating in complex international locations), the acquisition strategy is aggressive enough to outpace internally generated capital, and the new asset-light model has not yet proven it can generate sufficient free cash flow to fund growth organically. All three of these conditions apply to Beng Kuang, at least partially, at the moment. That means the dilution story is not entirely over, even as the ASOM consolidation closes a major chapter of it.

Management Alignment: The Question That Keeps Me Up at Night

Peter Lynch once said that one of his most important tests of a business is whether the people running it think like owners. It is a simple test. Are they eating their own cooking? Do their interests align structurally with yours as a minority shareholder?

This is where I want to be transparent about what I found in Beng Kuang’s cap table, because the picture is mixed in ways that matter.

The known insider equity stakes are as follows: CEO Yong Jiunn Run holds approximately 5.3%, Chairman Chua Beng Yong holds 4.8%, COO Chua Beng Hock holds 4.2%, and Executive Director Chua Meng Hua holds 4.4%. Together, and including the speculative stake of co-founder of Labroy Marine Chan Kwan Bian at 12.5%, total insider ownership reaches approximately 30% of the cap table. Without Chan Kwan Bian — whose classification as an “insider” is less certain — it is closer to 18.7%.

This is not low. But it is not the 50-60% insider ownership I look for in companies where I have the highest conviction. Compare it, for example, to businesses where the founding family essentially runs the company and holds the majority of economic interest in it. In those situations, the incentive alignment is almost automatic — what is good for shareholders is good for the founders, and what is bad for shareholders is correspondingly painful for the founders. Beng Kuang’s insider ownership is meaningful, but it does not clear that bar.

What concerns me more is the compensation structure. The top four executive officers have almost or more than 50% of their total remuneration tied to “Bonus.” That means the majority of their take-home pay is variable, performance-linked income. In principle, this is good — it means they are incentivized to perform. But the critical question is: what are the performance metrics that trigger these bonuses? Revenue? EBITDA? Return on equity? Earnings per share? Free cash flow per share? These different metrics lead to very different behaviors. A management team rewarded on revenue growth might be incentivized to grow aggressively even at the expense of shareholder dilution. A management team rewarded on free cash flow per share would never do something dilutive unless it was clearly accretive on that metric.

The annual report does not disclose the specific bonus metrics. I find that frustrating. I do not think the company is being evasive — this is a common disclosure gap in smaller Singapore-listed companies — but the absence of that information means I cannot verify that management’s incentives are structurally aligned with mine. And I am not willing to speculate my way into conviction on something this important.

There is one bright spot here. COO Chua Beng Hock owns a 4.8% stake worth approximately S$5.1 million at current prices, while his annual wage (approximately 30% of the S$750,000 to S$1,000,000 band) is roughly S$300,000. That means his equity stake is worth approximately 17 years of his base salary, excluding bonus. That is skin in the game. That is a man who has a personal financial reason to not blow up the business. But it does not, by itself, answer the question of whether the bonus structure rewards the right behaviors at the company-wide level.

Contrarian Risks: What If Everything I Believe About the Moat Is Wrong?

Investing is an exercise in calibrated confidence. You are never certain. You are only ever more or less certain, and the discipline of great investing is knowing how certain you should be and what price compensates you for your uncertainty. One of the most useful exercises I know is to take your investment thesis and deliberately try to destroy it — to think about the scenario in which you are most wrong, and ask how likely that scenario is.

Here is my attempt at destroying the Beng Kuang thesis.

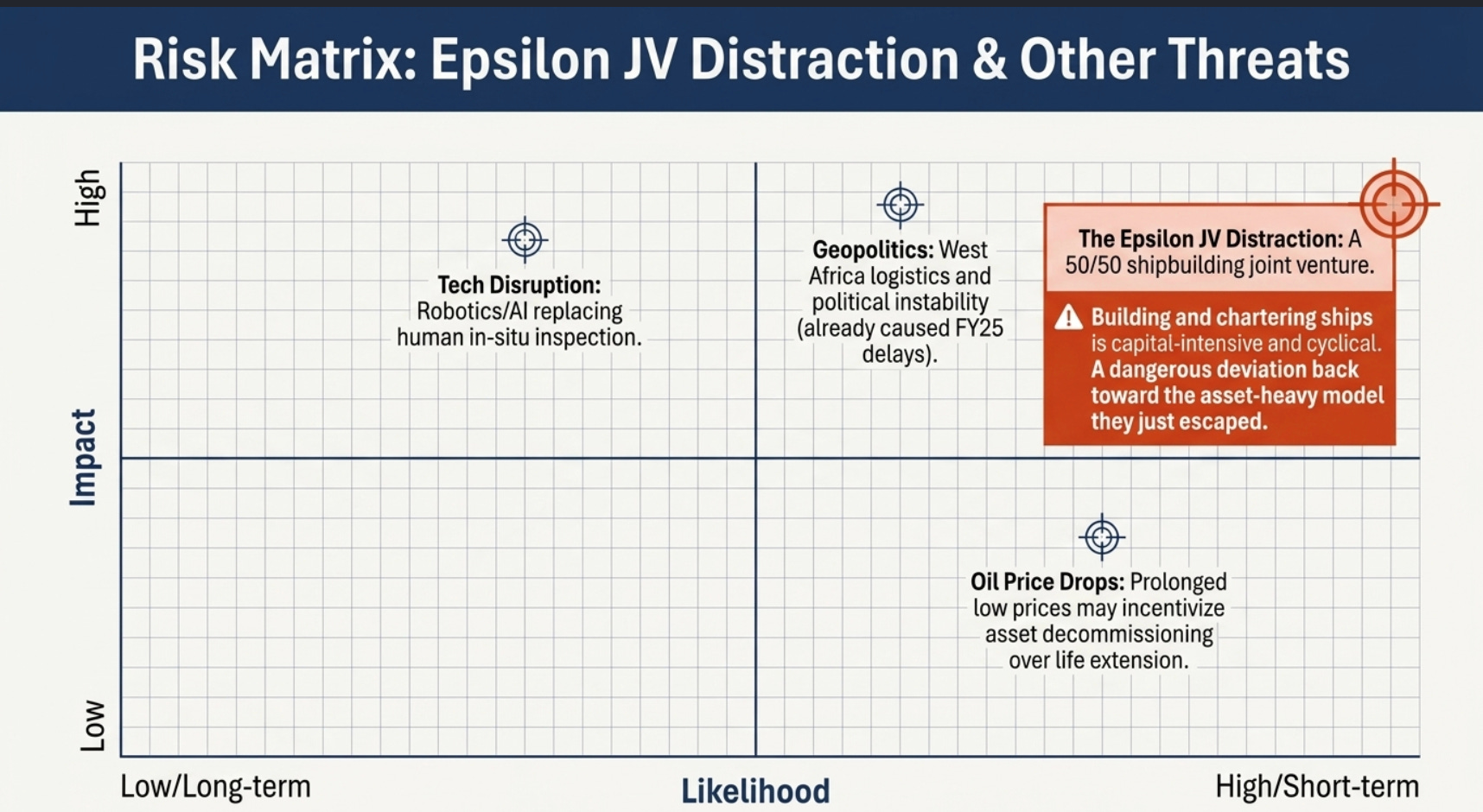

The first risk I will consider is the technological disruption risk. The moat I described — embedded knowledge, multi-disciplinary teams, regulatory incumbency — is real and durable today. But durability has limits. The offshore oil and gas industry is beginning to experiment with robotics and remote inspection technologies. Companies are developing autonomous underwater vehicles for hull inspection, drone-based topside surveys, and AI-powered corrosion detection systems. If these technologies mature to the point where they can replace a significant portion of the in-situ inspection and maintenance work that human teams currently do, then the multi-disciplinary team moat begins to erode. I do not think this is a near-term risk — the regulatory frameworks are not yet ready to accept robotic-only inspection for class purposes, and the structural repair and corrosion mitigation work remains physically intensive — but it is a 10 to 15 year risk that any investor with a long time horizon needs to hold in mind.

The second risk is geopolitical and operational concentration. A significant portion of Beng Kuang’s revenue through ASOM comes from West Africa — Angola, Ghana, Guinea — and South America. These are jurisdictions that carry elevated risks of political instability, currency devaluation, regulatory unpredictability, and logistical disruption. The FY2025 revenue decline was itself partly caused by “logistical challenges associated with the deployment of accommodation barges” in West Africa. That is operational risk manifesting in real-time. One project delay can compress a year’s revenue recognition, as happened in FY2025. More serious disruptions — a change in government policy, a currency crisis, a security incident — could impair ASOM’s ability to operate in its core markets.

The third risk is the ASOM acquisition itself. Beng Kuang paid approximately S$60 million for the remaining 49% of ASOM, at a valuation representing approximately 8x FY2025 profit after tax for the full business — or approximately 2x the intrinsic value when measured by net asset plus normalized profit. This is not a bargain acquisition. The price assumes ASOM continues to grow, that the West Africa delays are genuinely temporary, and that the FY2026 and FY2027 earn-out targets are achievable. If ASOM’s earnings disappoint over the next two years, the earn-out payments decline, which is structurally protective, but the equity Beng Kuang has already issued in consideration does not disappear. The dilution is permanent. The benefit is contingent.

The fourth risk, which I find most unsettling because it cannot be quantified, is the oil price risk. I know what Beng Kuang’s management says — that their revenue is OPEX-driven and compliance-mandated, not subject to the boom-and-bust of oil prices. This is largely true. But “largely” is doing meaningful work in that sentence. While a sharp and sustained drop in oil prices below US$50 per barrel remains a tail risk that could weaken spending on asset maintenance, more subtly, a prolonged period of oil price weakness could incentivize FPSO operators to delay non-mandatory maintenance, renegotiate contract terms, or accelerate the decommissioning of aging assets rather than extending their lives. This would compress Beng Kuang’s addressable market. It would not destroy the business, but it would impair growth.

The fifth risk is the one that is most embarrassing to articulate but most important to name: the shipbuilding distraction. The company has entered into a 50/50 joint venture with Epsilon for shipbuilding in Batam, with a strategy of building vessels and then chartering them. This is exactly the opposite of an asset-light model. Owning and chartering ships is capital-intensive, cyclical, and full of the kind of balance sheet risk that Beng Kuang spent five years trying to escape. Management describes it as “strategic optionality” and “platform optionality, activated selectively, not core.” But the fact that they pursued it at all tells me something about the discipline — or absence of discipline — in capital allocation. A small distraction today can become a large problem tomorrow if the incentives shift or the opportunity looks bigger than it is. A management team that is truly committed to asset-light thinking does not dip its toes into asset-heavy models, no matter how attractive the narrative.

The Structural Tailwind: Why the Market Will Eventually Pay Attention

Having been honest about the risks, let me now be equally honest about why this company remains firmly on my watchlist.

The structural tailwind is real and it is compounding. ABS data shows that 55 FPSO units in the global fleet are reaching the end of their design life in the next five years, with a further five already having life extension in place and 19 currently being evaluated for life extension. This is not speculative demand. These are physical assets with legal inspection requirements approaching. The operators of these assets will need to choose between decommissioning (expensive, revenue-terminating) and life-extension (cheaper, keeps revenue flowing). Given that life extension costs only 30 to 50% of the price of a newbuild, which can cost between US$1 billion and US$3 billion, the economic incentive to extend rather than replace is overwhelming in most environments. Beng Kuang, through ASOM, is one of the few qualified providers who can execute this work on-site, in-situ, without bringing the vessel to shore.

The forward contract visibility is also strengthening. As of week 13 of 2026, the company disclosed approximately S$51.2 million of FY2026 revenue already secured, distributed across three segments: approximately S$27.6 million from ASOM’s lifecycle engine, S$15.8 million from new shipbuilding in Batam, and S$12.5 million from Deck Equipment and Cranes. The ASOM component alone confirms the recurring nature of the business — 19 FPSOs and FSOs across 7 countries are contractually obligated to maintain continuous FPSO integrity programmes with Beng Kuang. This is not a company scrambling for orders. It is a company managing a pipeline.

Upon completion of the ASOM acquisition, BKM’s earnings base will materially expand while shifting towards recurring offshore asset lifecycle services, improving earnings visibility and supporting a structural re-rating of the group. The analyst who initiated coverage on the stock in March 2026 placed a target price of S$0.535 against a then-price of S$0.365, representing potential upside of 46.6%, on the basis of 12x blended FY2026 and FY2027 earnings — a modest multiple for a business of this quality, if you believe in the model.

I find the target price plausible. I find the timing uncertain.

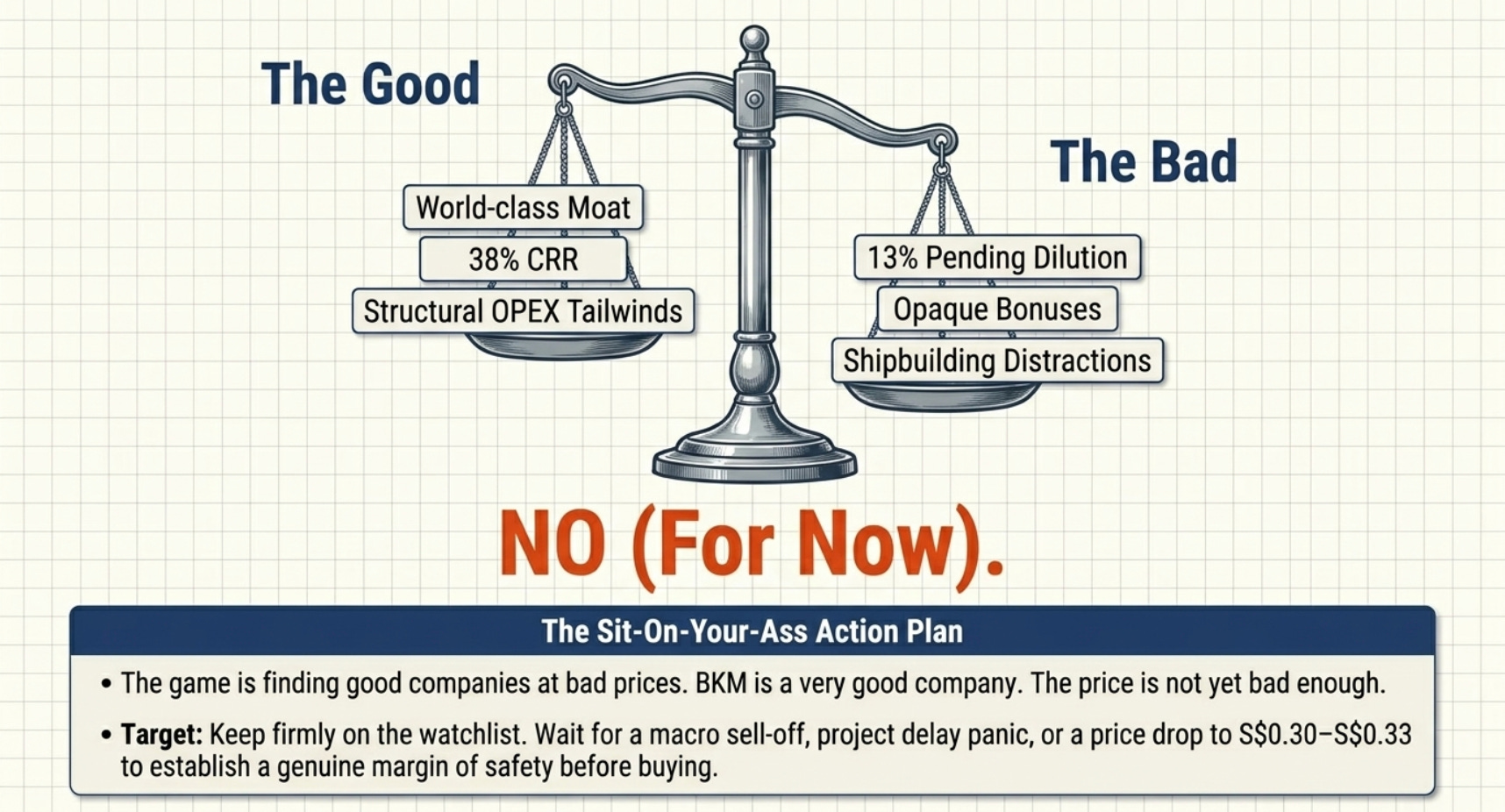

Why the Conclusion Is Still No (For Now)

Here is the honest summary of where I land.

This is a good business. It has a real moat — a sticky, compliance-driven customer base, embedded in safety-critical supply chains, with high switching costs and a specialized labor advantage that cannot be easily replicated. The structural tailwind — an aging global FPSO fleet, rising inspection mandates, cost economics that favor life extension over replacement — is not speculative. It is already happening. The transformation from an asset-heavy, loss-making shipyard business to a lean, recurring-revenue service model has been executed well by a CEO who deserves credit for the turnaround.

But the price at S$0.475, with a P/E of approximately 18 on the current earnings base and an adjusted diluted value of S$0.413, does not offer the margin of safety I require. The dilution is meaningful. The management alignment is incomplete. The compensation structure’s opacity is a genuine concern. The shipbuilding joint venture is a distraction from a thesis that depends on disciplined capital allocation.

More fundamentally: the opportunity does not yet look like the kind of world-class compounders I compare every business against. At 38% CRR, it is a very good business. At a P/E of 18, it is a fairly priced one. The price I would need to see to feel genuinely excited — the price that would make the margin of safety obvious and the opportunity feel like finding a $100 bill on the sidewalk — would require either a pullback in the share price to closer to S$0.30 to S$0.33, or a demonstrable acceleration in earnings that brings the forward P/E down to 10 to 12 times on fully diluted EPS. At that price, with these business economics, I would not hesitate.

What this company is doing right now is what the best watchlist candidates do: it is proving the model, demonstrating earnings quality, and growing into a valuation that is still slightly ahead of where the fundamentals have arrived. The market has already re-rated this company significantly — from S$0.22 to S$0.475 over the past year, a return of over 73% — which means many of the obvious catalysts have already been priced in. The remaining catalysts — full ASOM consolidation, West Africa contract renewals, Deck Equipment order growth — are real, but they are now already embedded in market expectations.

The game of investing is not about finding good companies. It is about finding good companies at bad prices. Beng Kuang is a good company. The price is not yet bad enough.

This analysis was written based on my own research and the information available as of April 2026. It does not constitute investment advice. All investment decisions carry risk, and readers should conduct their own due diligence or consult a licensed financial advisor before making any investment.