Investment Reflection #3 — Four Lessons the World’s Best Business Schools Won’t Teach You

A White Paper on Petrodollar Power, Social Marketing, Monetary Architecture, and the Slow Poison of Modern Finance

“The goal of education is not to fill a bucket but to light a fire. The goal of this document is to hand you the flint and tell you where the kindling is.”

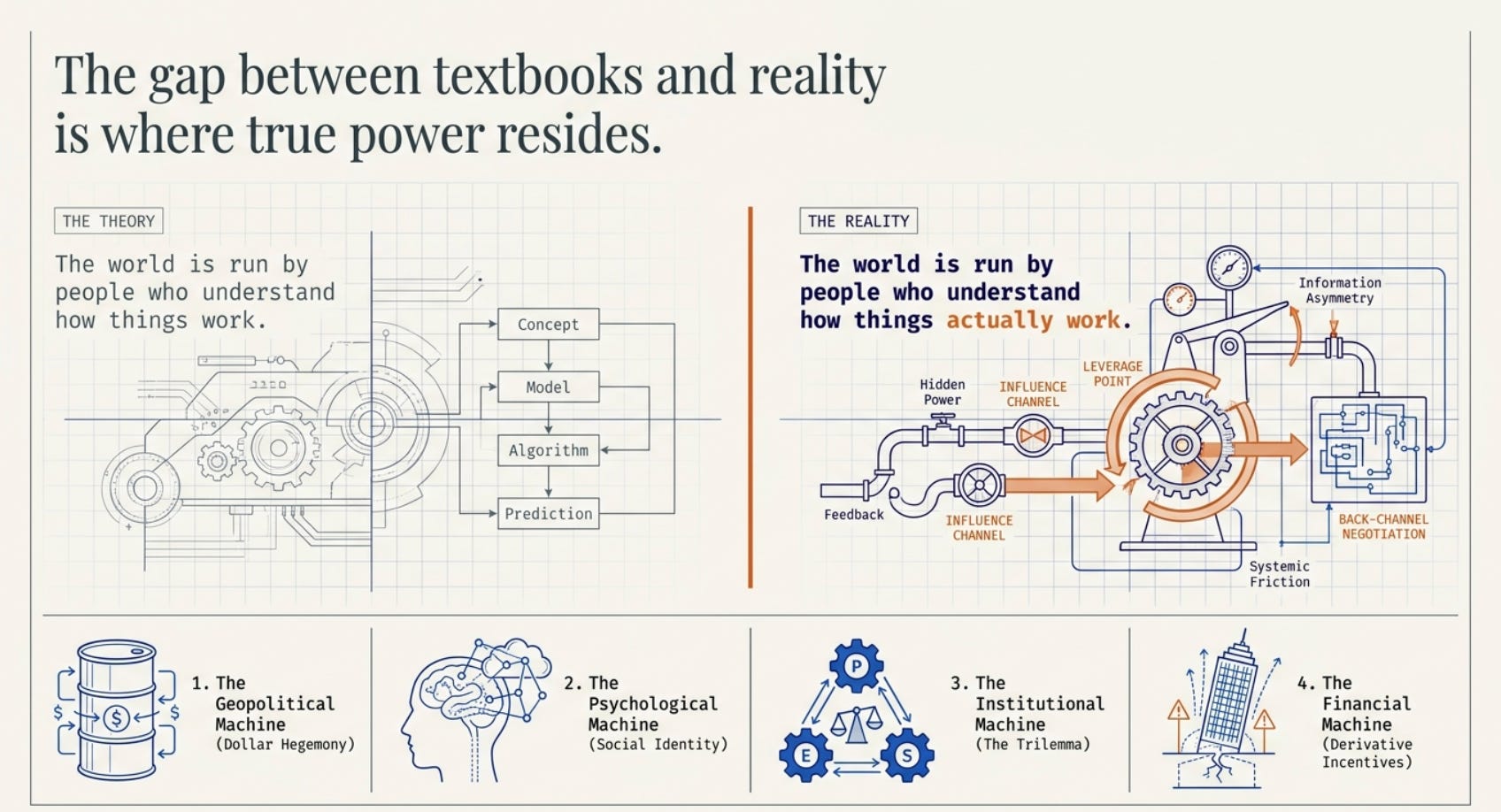

PART ONE: THE INVISIBLE EMPIRE

How America Discovered It Could Print Money and Make the World Pay for It

The Setup: A World That Needed Rules

Imagine you have just survived the most destructive war in human history. You are sitting in a conference room in Bretton Woods, New Hampshire, in July 1944. The war in Europe is not yet over. The Pacific war has more than a year to run. But you — representing one of the 44 Allied nations — are already solving the problem of what comes after.

The question on the table is deceptively simple: how should the world conduct trade?

It sounds like a technical question. It is not. It is the most political question imaginable, because whoever designs the answer to that question designs the power structure of the next century.

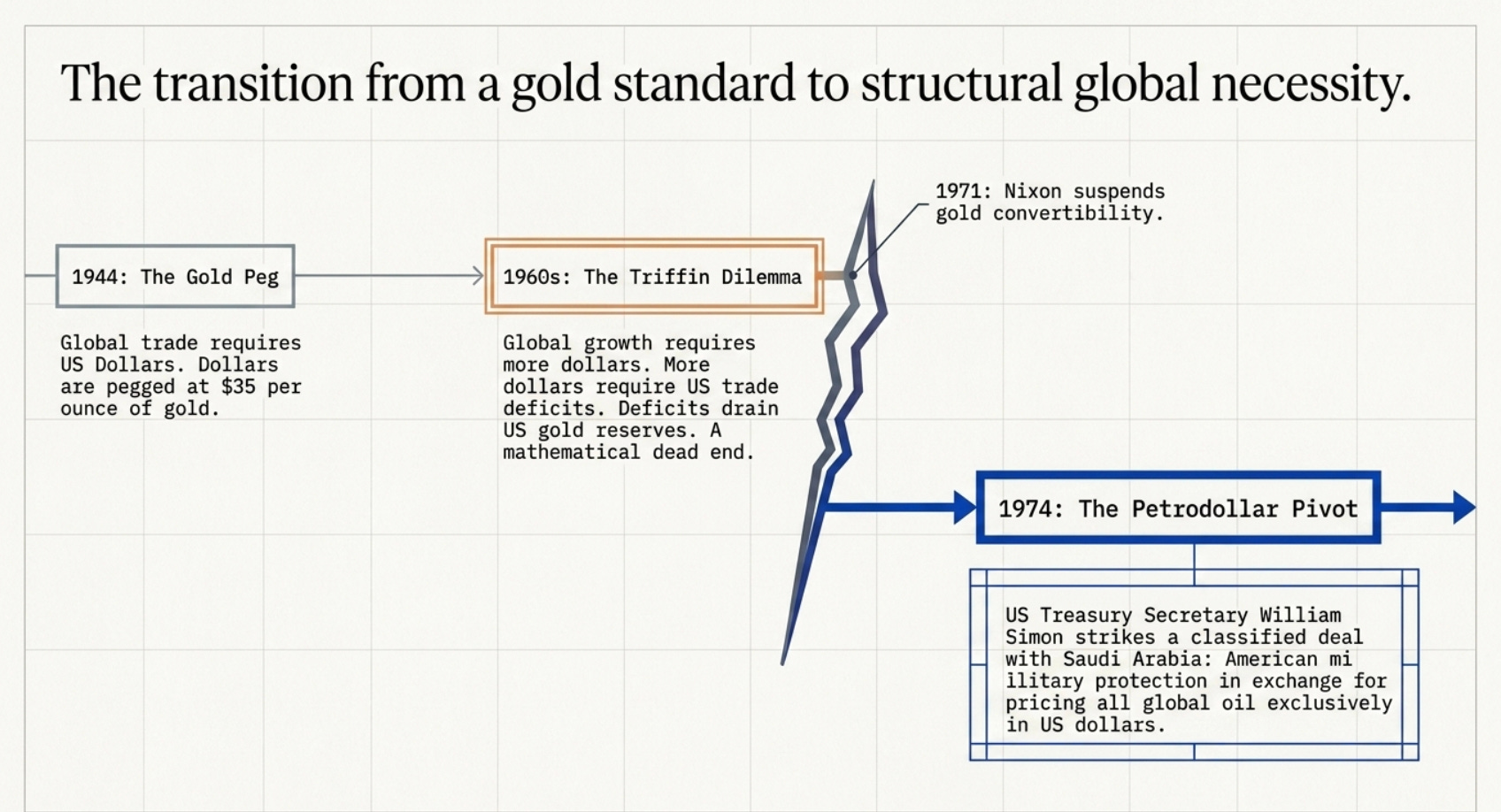

The answer chosen at Bretton Woods was this: every currency would be pegged to the US dollar at a fixed exchange rate, and the dollar would be redeemable for gold at $35 per ounce. Every country that wanted to trade internationally needed dollars. The dollar was the world’s reserve currency — the language every economic transaction had to be spoken in.

This arrangement — the Bretton Woods system — worked extraordinarily well for 25 years. The world economy grew. Trade expanded. The dollar was trusted because it was redeemable for gold, and the United States held the majority of the world’s monetary gold in the vaults at Fort Knox.

But here is the trap that was built into the system from the very beginning, identified by Belgian economist Robert Triffin in 1960, and known ever since as the Triffin Dilemma:

For the world to grow economically, it needs more dollars. For more dollars to exist, the United States must run trade deficits — spend more abroad than it earns. But if America runs persistent deficits, foreign nations accumulate dollars and begin to wonder: is there really enough gold at Fort Knox to back all of these? When they begin to wonder, they begin to redeem. When they redeem, the gold runs out. When the gold runs out, the system collapses.

By the late 1960s, America was spending on Vietnam, on the Great Society, on the Space Race. Dollars flooded the world. France — led by a President who deeply resented American financial dominance — began redeeming dollars for gold in massive quantities. American gold reserves were draining at an alarming rate.

America had to make a choice. It could discipline its spending to preserve the gold peg. Or it could do something audacious: simply change the rules of the game.

On August 15, 1971, President Nixon went on television and announced that the United States was suspending the dollar’s convertibility into gold. Just like that, with one speech, the entire framework that had governed global finance for 27 years was gone. Currencies would now float freely against each other. The dollar was backed by nothing but faith.

The world screamed. Economists panicked. And then... something remarkable happened. Nothing collapsed. The dollar remained the dominant reserve currency. International trade continued to use dollars. The system survived the removal of its supposed foundation — gold — without missing a beat.

Why? Because America had, quietly and without formal announcement, already found something better than gold to back the dollar. Something every industrial economy needed even more desperately than it needed gold.

It had found oil.

The Birth of the Petrodollar: The Deal That Changed Everything

To understand the petrodollar system, you need to understand Saudi Arabia in 1973.

Saudi Arabia had been sitting on the world’s largest oil reserves for decades. But the price of oil had been set, not by Saudi Arabia, but by Western oil companies operating in the country under concession agreements negotiated in the colonial era. Saudi Arabia received royalties; the oil companies — and their Western shareholders — captured most of the value.

In October 1973, the Arab-Israeli War broke out. Arab members of OPEC declared an oil embargo against nations that had supported Israel, and simultaneously cut production. Within months, the price of oil quadrupled from roughly $3 per barrel to $12. The industrial world — which ran entirely on cheap oil — experienced an economic shock unlike anything since the Great Depression.

In this moment of chaos, the United States and Saudi Arabia sat down and made a deal. The precise details were classified for decades, but the broad structure has been confirmed by declassified documents, former officials, and investigative reporting.

The deal had two sides:

What Saudi Arabia promised: it would price all of its oil sales exclusively in US dollars. Since Saudi Arabia was the world’s dominant oil producer, and since the other Gulf states followed its lead, this meant that all global oil transactions would be conducted in dollars. Any country in the world — whether it was Japan, Germany, India, or Brazil — that needed to buy oil had to first acquire dollars. The dollar became not just a reserve currency but a necessary tool for economic survival.

What America promised: it would provide military protection to the Saudi regime — specifically, security guarantees including arms sales and an implicit promise to defend Saudi Arabia against external threats and internal challengers. American military presence in the Gulf was the price America paid for the petrodollar arrangement.

This deal was consummated formally in June 1974, when US Treasury Secretary William Simon signed a series of agreements with Saudi Arabia covering economic cooperation and military sales. What was not in the signed documents — but was understood by both sides — was the oil-pricing-in-dollars agreement.

The petrodollar system was born.

How the Machine Actually Works

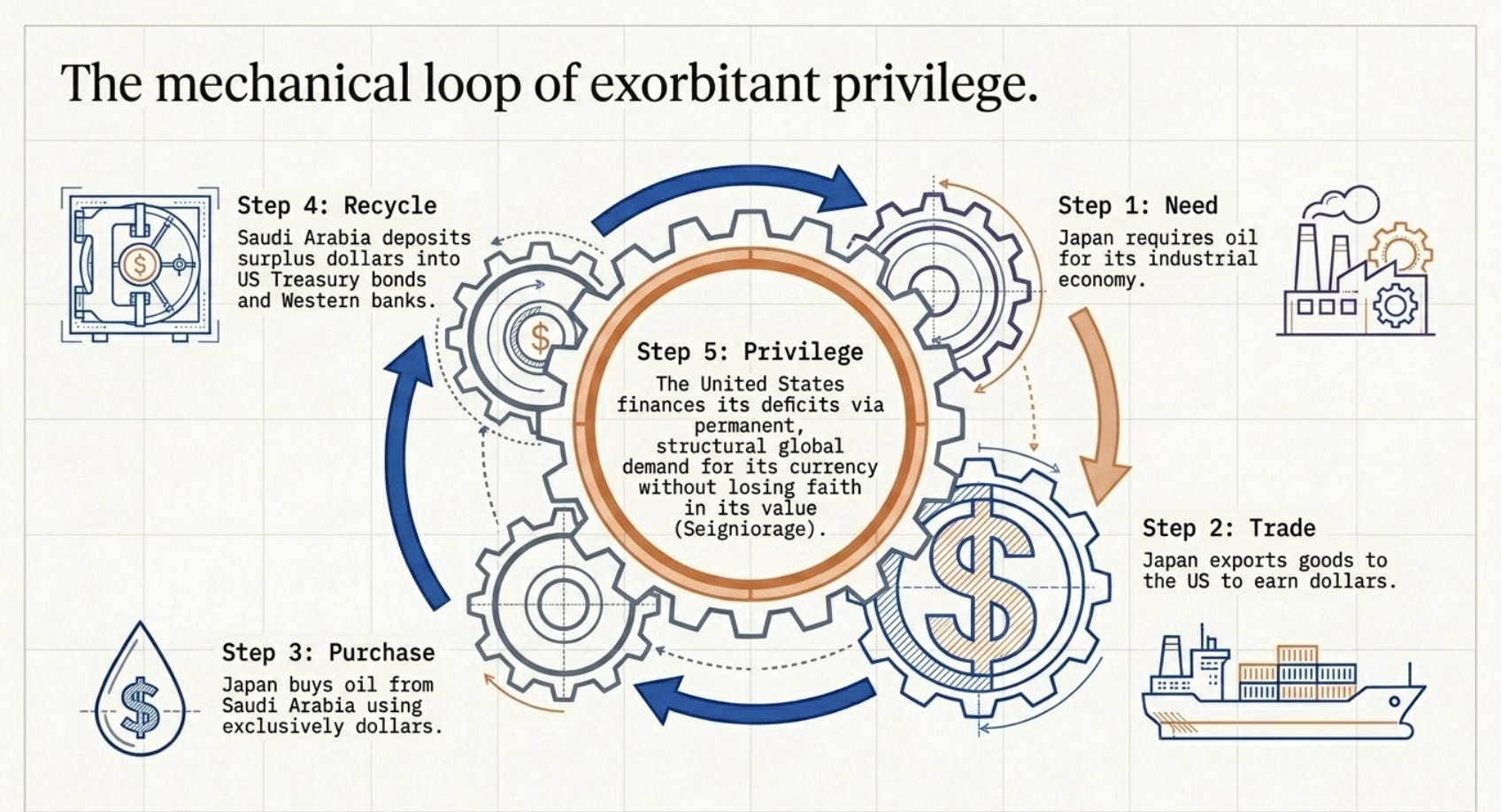

Now let’s trace the money. This is where the real education begins, because the mechanism is elegant in a way that almost no textbook adequately explains.

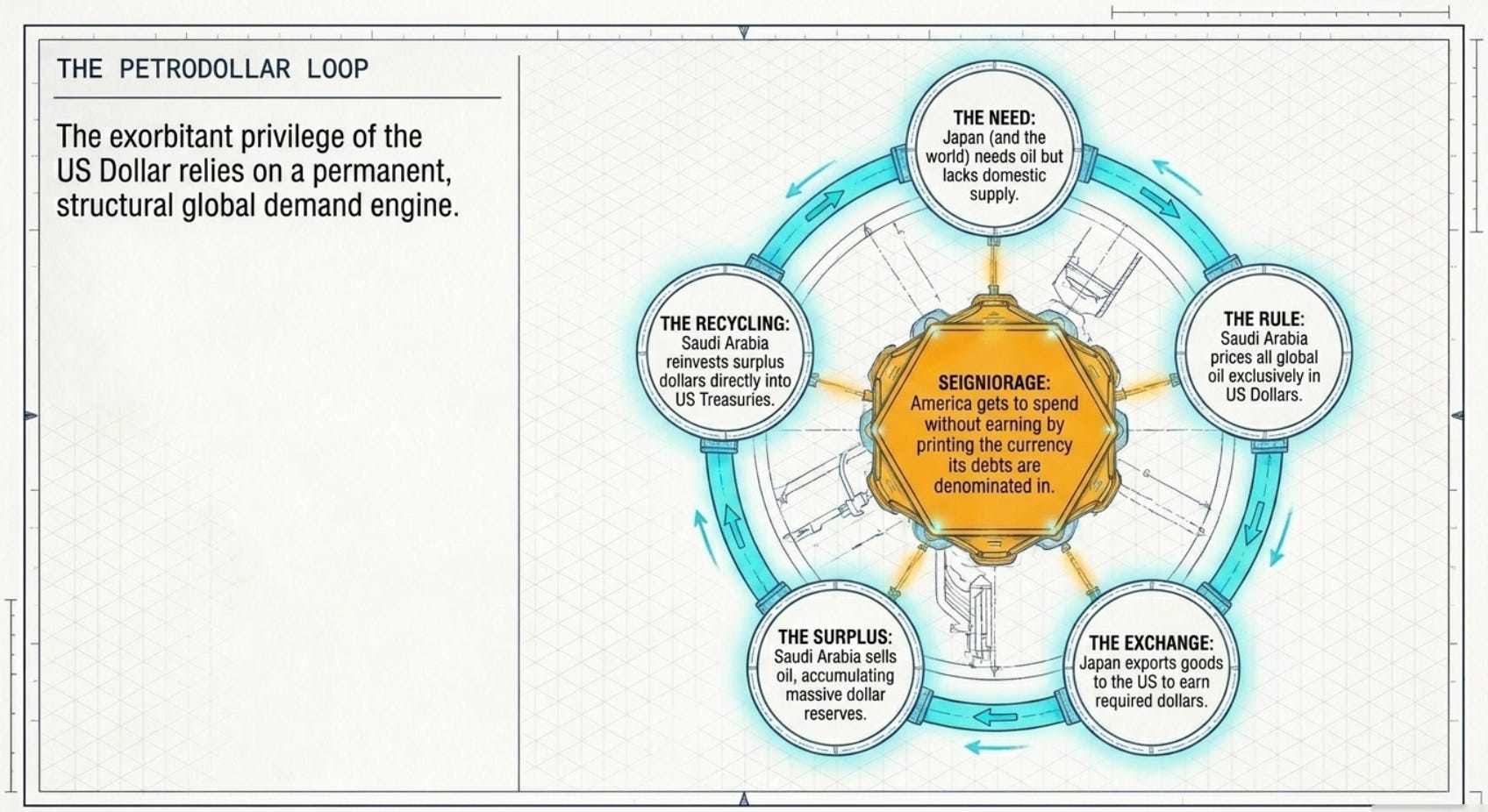

Step One: Japan needs oil. Japan is an industrial economy with almost no domestic oil production. It imports virtually all of its oil. To buy that oil, it needs dollars — because Saudi Arabia will only accept dollars.

Step Two: Japan earns dollars. Japan exports cars, electronics, and machinery to the United States and receives dollars in payment. These dollars are now available to buy oil.

Step Three: Saudi Arabia receives dollars. Saudi Arabia sells oil, receives dollars, and now has a problem: it has more dollars than it can spend domestically. Saudi Arabia’s economy, despite its oil wealth, is not large enough to absorb the dollars it earns.

Step Four: Saudi Arabia recycles petrodollars. Saudi Arabia deposits its surplus dollars in American banks (primarily in New York and London). It buys US Treasury bonds — lending money to the US government. It buys American real estate, American stocks, American companies. The dollars flow back to America.

Step Five: America gets to spend without earning. This is the magic. Because every country in the world needs dollars to buy oil, there is permanent, structural global demand for dollars. This means America can print dollars — run budget deficits, trade deficits — and the world will absorb those dollars without losing faith in them. America is the only country in the world that can pay its debts by printing the same currency its debts are denominated in, and have the world accept this as payment.

The formal name for this privilege is seigniorage. The informal name is exorbitant privilege — a term coined by French Finance Minister Valéry Giscard d’Estaing in the 1960s to express France’s fury at America’s ability to finance itself on the world’s dime.

The petrodollar system turns this privilege into a permanent structural advantage. Every oil transaction anywhere in the world is, in effect, a vote of confidence in the dollar. Every barrel of Saudi crude sold to China, every barrel of Emirati crude sold to South Korea, every barrel of Kuwaiti crude sold to Germany — all of it maintains global demand for dollars, which allows America to spend more than it earns, indefinitely.

To understand the scale of this privilege: the United States runs a current account deficit — imports more than it exports — of roughly $800 billion to $1 trillion per year. In any other country, this would trigger a currency crisis within years, as the world would lose confidence in a currency that was being chronically oversupplied. For America, it barely makes the news. The petrodollar system is the reason.

America’s Weapons: What Dollar Hegemony Lets America Actually Do

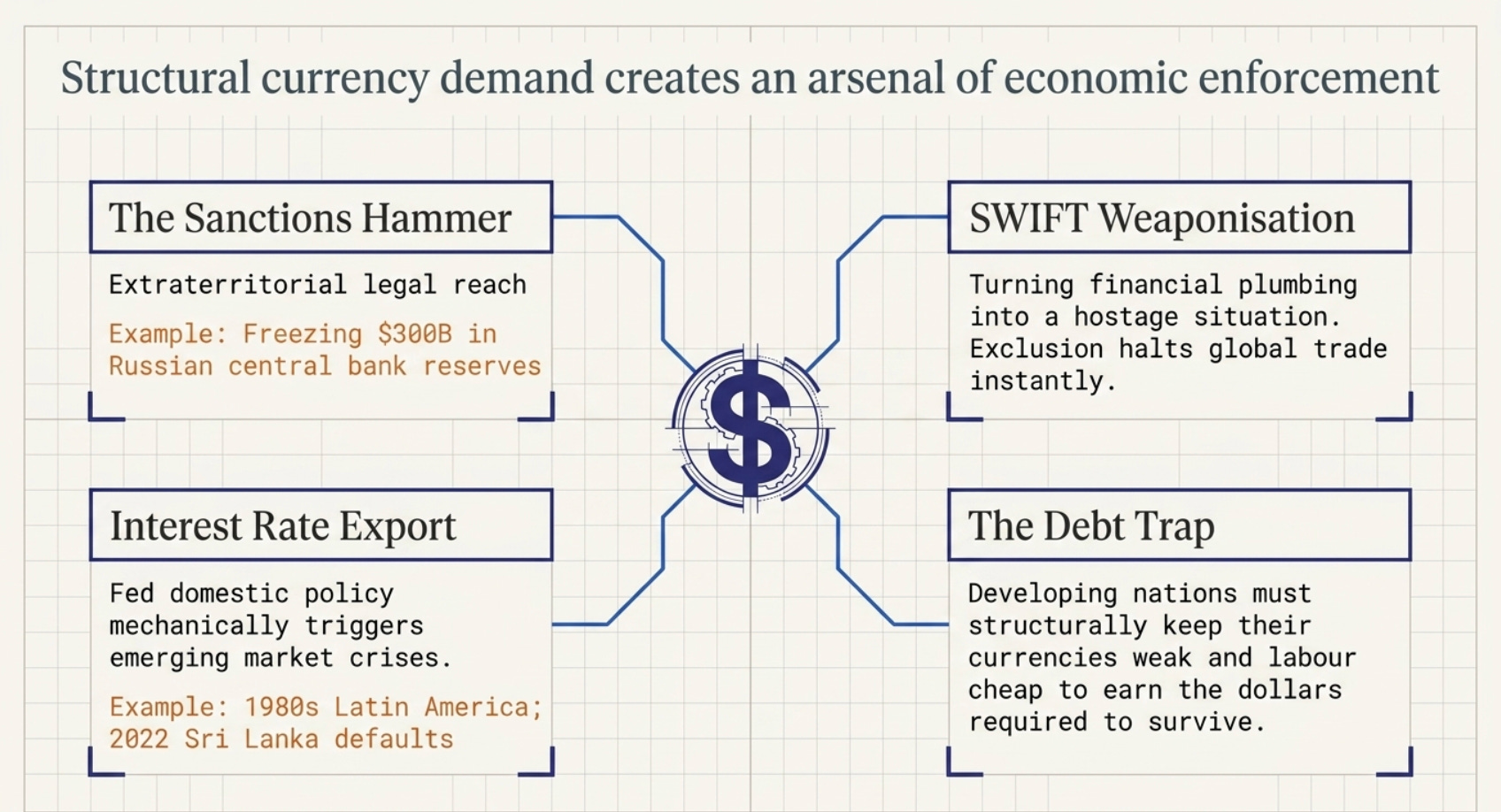

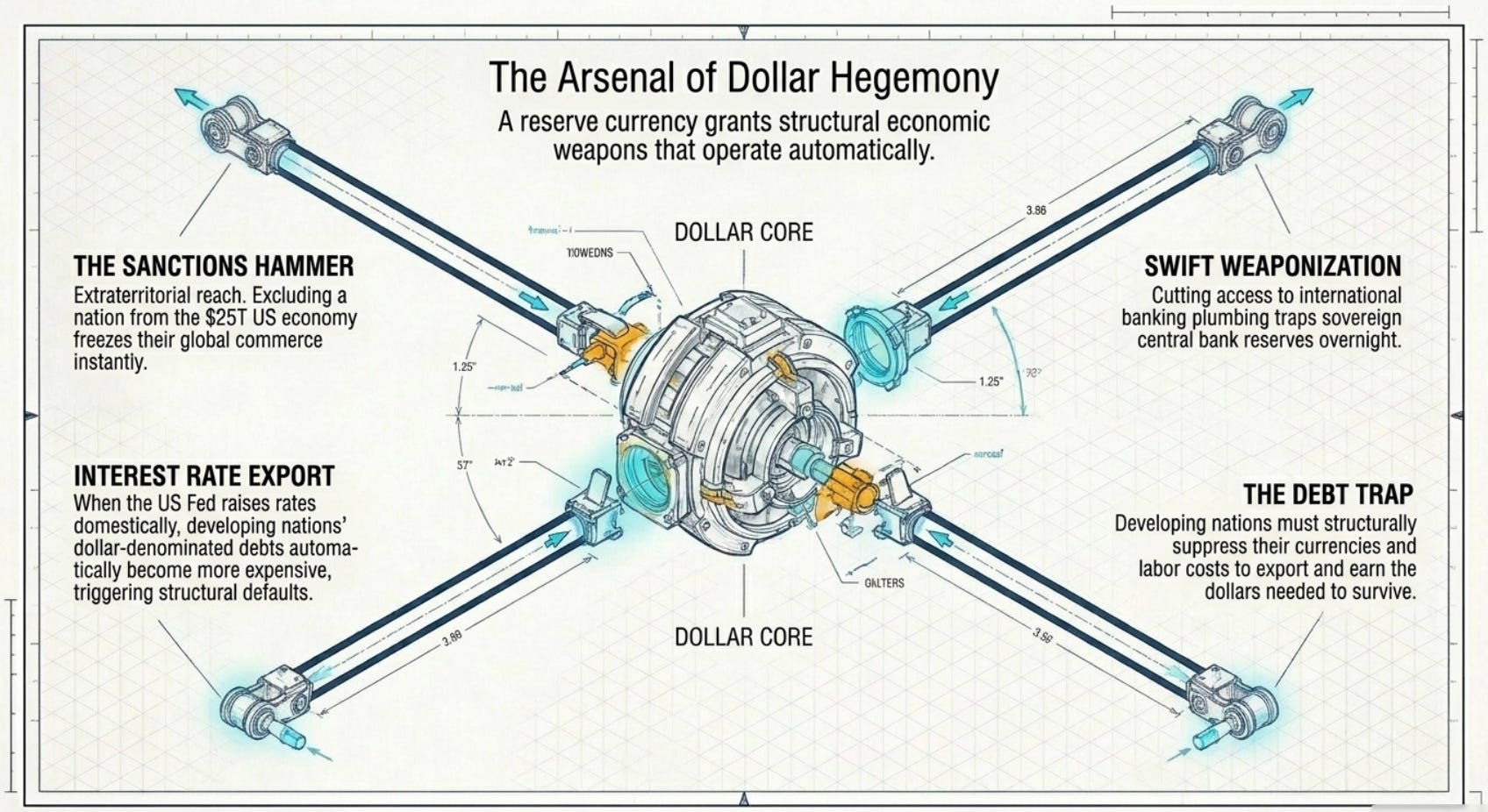

Here is where the story gets genuinely dangerous. Because the petrodollar system is not just about America’s ability to finance itself cheaply. It gives America an arsenal of economic weapons that no previous empire in history has possessed.

Weapon One: The Sanctions Hammer

Because international trade — especially commodity trade — runs on dollars, because international banking transactions clear through American correspondent banks, and because the SWIFT international payment system operates in the dollar ecosystem, any nation that America excludes from the dollar system is effectively cut off from global commerce.

When America imposed sanctions on Iran, it was not just banning American companies from trading with Iran. It was threatening to exclude from the American financial system any bank anywhere in the world that continued doing business with Iran. European banks, Asian banks, Japanese banks — all of them faced the choice: do business with Iran, or do business with the United States. The United States is a $25 trillion economy. Iran is a $300 billion economy. The choice was not difficult.

This is the extraterritorial reach of dollar hegemony. American law effectively governs global financial behavior — not because countries agree to it, but because they cannot afford to be excluded from the dollar system.

When Russia invaded Ukraine in 2022, America took this a step further: it froze approximately $300 billion of Russian central bank assets held in Western financial institutions. The Russian central bank — the sovereign monetary authority of a nuclear-armed nation — suddenly could not access its own reserves. This had never been done before at this scale. It worked because those reserves were held in dollar-denominated accounts in Western institutions that fell under American and European jurisdiction.

Weapon Two: Interest Rate Export

When the United States Federal Reserve raises interest rates — a domestic monetary policy decision made for domestic reasons — it affects every developing nation in the world.

Here is why. Developing nations have borrowed trillions of dollars of debt denominated in US dollars. When American interest rates rise, the dollar strengthens (because investors move capital to dollar assets to earn higher returns). A stronger dollar means that developing nations’ dollar debts become more expensive relative to their local currencies. At the same time, capital flows out of developing markets back toward the higher-yielding American market, weakening developing currencies further.

This is not a conspiracy. It is not intentional targeting. It is simply the mechanical consequence of dollar hegemony. The Federal Reserve raises rates to fight American inflation, and Sri Lanka defaults on its sovereign debt. The Federal Reserve raises rates to cool the American economy, and Argentina faces a currency crisis. The mechanism is automatic, structural, and unavoidable for any nation that has borrowed in dollars.

The 1980s debt crisis in Latin America and Africa? Triggered by the Federal Reserve raising rates to 20% to fight American inflation. The 1997 Asian financial crisis? Exacerbated by dollar strength and capital flight. The 2022 emerging market debt distress? Directly linked to the Fed’s rapid rate increases.

Weapon Three: The Weaponization of SWIFT

SWIFT — the Society for Worldwide Interbank Financial Telecommunication — is the messaging network that coordinates international bank transfers. It is the plumbing of the global financial system. Without SWIFT access, a country’s banks cannot send or receive international payments. Goods cannot be paid for. Trade cannot happen.

Excluding Iran from SWIFT in 2012, and Russia from SWIFT in 2022, effectively turned this infrastructure into an economic weapon. Nations that have been excluded from SWIFT have seen their economies immediately and severely damaged.

The lesson every nation in the world drew from the Russia exclusion was profound and deeply uncomfortable: if your currency reserves are held in Western institutions and denominated in dollars, you are a hostage. The moment your government does something the United States seriously objects to, those reserves can be frozen. Your central bank’s war chest — built up over decades of export surpluses to protect against currency crises — can be rendered inaccessible overnight.

Weapon Four: The Debt Trap Mechanism

The petrodollar system creates a structural mechanism by which developing nations perpetually run dollar deficits. They must earn dollars to buy oil. To earn dollars, they must export. To export at competitive prices, they must keep labor costs low and currencies weak. Keeping currencies weak means their purchasing power remains low, making it expensive to import the capital goods they need to industrialize.

This is not an accident. It is the mathematical consequence of a reserve currency system combined with oil pricing. The nations that benefit from breaking this cycle are the ones that develop alternative energy sources (reducing oil import dependence) or that join the reserve currency club (which only happens through extraordinary economic and political development).

The Cracks: The Coming Challenge to Dollar Hegemony

The petrodollar system has lasted 50 years. It will not last forever, and the cracks are visible.

The most significant crack is China. China is now the world’s largest oil importer. For decades, it paid for oil in dollars, like everyone else. But since around 2018, China has been systematically building an alternative: the petroyuan. Saudi Arabia has begun accepting yuan for some oil sales to China. Russia — cut off from the dollar system — now invoices much of its oil in yuan. The Shanghai International Energy Exchange trades oil futures contracts priced in yuan.

None of this is an existential threat to the dollar’s dominance today. The yuan is not freely convertible. China’s capital markets lack the depth and transparency of American markets. There is no yuan-denominated alternative to US Treasury bonds as a safe reserve asset.

But the marginal erosion matters. Every barrel of oil priced in yuan is one fewer barrel reinforcing global dollar demand. Over decades, marginal erosion compounds. The dollar’s share of global reserve holdings has already declined from roughly 72% in 2000 to approximately 58% today. The direction of travel is clear, even if the destination is distant.

The BRICS nations — Brazil, Russia, India, China, South Africa, with recent expansions — have explicitly discussed developing an alternative reserve currency or payment system. The practical obstacles are enormous. But the political motivation has never been stronger.

What happens if dollar hegemony erodes significantly? America would have to compete like every other nation. It would have to balance its budgets. It would have to pay global market interest rates. Its military reach would be constrained by the actual size of its tax base. The exorbitant privilege would end. It would be, in a word, an ordinary nation.

Which is why America will defend the petrodollar system with every tool at its disposal. Understanding this is understanding the last 50 years of American foreign policy.

PART TWO: THE MARKETING MASTERCLASS

Why Every Brand That Has Ever Confused Demographics for Identity Has Left Money on the Table

The Dangerous Map

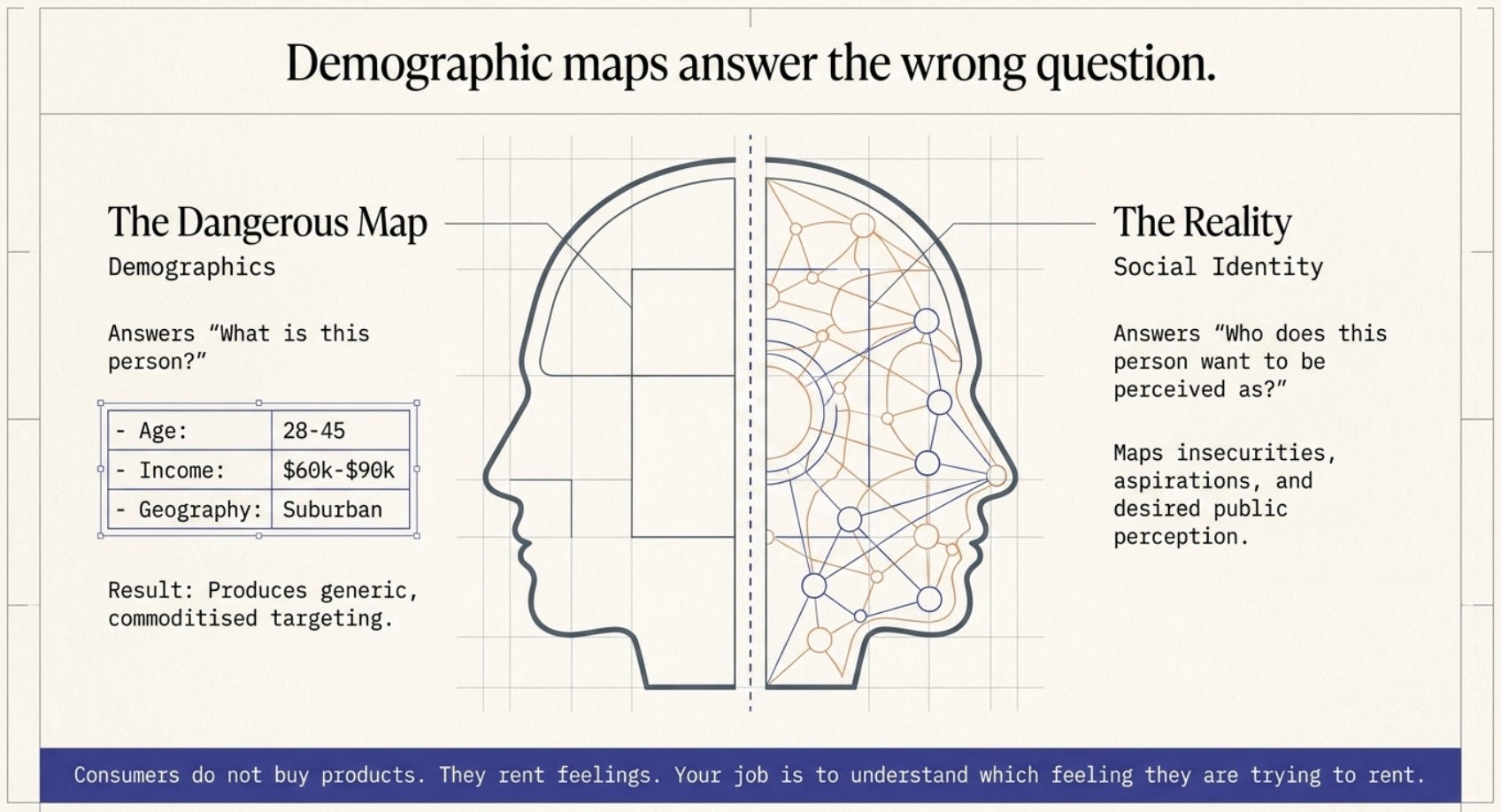

In marketing classrooms around the world, the demographic targeting framework is taught as the foundation of customer strategy. Segment your market. Age, gender, income, geography. Build your persona. Target accordingly.

Krispy Kreme’s story — reveals why this framework is dangerously incomplete. And the gap between where Krispy Kreme is and where it could be is measured not in distribution points or production capacity, but in the failure to understand who their customer socially is, rather than what their customer demographically looks like.

Let me show you exactly what I mean.

The Social Identity Framework: What Demographics Miss

Demographics answer the question: what is this person? Age 28–45. Household income $60,000–$90,000. Female. Suburban. Two children.

Social identity answers a different question: who does this person want to be perceived as?

These are not the same question. And in the war for consumer attention, the second question wins every time.

Consider Starbucks. The company describes itself as “a premium experience, community, and a moment of personal relaxation for white collar prestige.” That phrase — white collar prestige — is the entire insight. Starbucks does not sell coffee to office workers. It sells a social signal to people who want to be seen as having sophisticated taste, modern values, and professional status.

Here is the proof: a Starbucks customer does not hide their cup. They carry it conspicuously. The cup is part of the costume. When Niccol (Chairman & CEO) restored handwritten names on cups, he was not improving customer service. He was reinforcing the social ritual of a prestigious white collared individual — the personal acknowledgment, the belonging, the sense that the barista knows you. That feeling, extended publicly through a walking advertisement, is the actual product.

Now look at what Krispy Kreme sells. A donut. A beautiful, glazed, instantly recognizable donut. But ask the honest question: what social identity does carrying a Krispy Kreme box signal? What story does the buyer tell themselves — and others — about who they are when they choose Krispy Kreme?

The answer, currently, is muddled. And that muddledness is perhaps the most expensive strategic problem Krispy Kreme has, because no amount of distribution expansion fixes it. You can put Krispy Kreme in every Walmart in America. If the social identity of the purchase is unclear, consumers will still choose Entenmann’s (comfort, value, familiar), or Starbucks (prestige), or the Walmart bakery (practical). They will not choose Krispy Kreme with the emotional momentum that drives true brand loyalty.

The Three Social Identities of Consumer Brands

Before we examine how the world’s best brands have solved this problem, let me give you the foundational framework — the map that the best marketers in the world actually use, even if they never formally name it.

Case Study One: How Apple Sold Status Through Simplicity

In the mid-1990s, Apple was demographically targeting creative professionals. The advertising showed designers, artists, musicians. The computers were positioned as tools for creative work. This was a demographic frame — here is the audience, here is the tool, here is the functional benefit.

Apple was struggling. The demographic was too narrow. The message was too rational.

Then came the “Think Different” campaign, and everything changed. The campaign did not target demographics. It did not mention features. It showed Einstein. It showed Gandhi. It showed Miles Davis and Maria Callas. It said: the people who are crazy enough to think they can change the world are the ones who do. And then: Think Different.

The campaign was not selling computers to creative professionals. It was selling a social identity — the identity of being someone who sees the world differently, who doesn’t follow the crowd, who has the courage and intelligence to reject the mainstream. Every person who bought an Apple product after that campaign was buying membership in that social identity.

Then Apple did something truly brilliant with the iPod and its white earbuds. Black earbuds were the industry standard. Apple made them white — not for technical reasons, but for social ones. White earbuds were visible from across the room. They were a tribal signal. They said, without words: I have an iPod. I am that kind of person.

Apple was not selling music players to 18–35-year-olds. It was selling a social identity signal that could be worn publicly. The demographic analysis of who bought an iPod would have told you nothing useful. The social identity analysis told you everything.

Case Study Two: How Patagonia Sold Guilt-Free Affluence

Patagonia’s target customer, demographically, is a wealthy outdoor enthusiast. Household income $120,000+. College-educated. Liberal values. Urban or suburban, with access to outdoor recreation.

But Patagonia does not market to this demographic. It markets to a social identity: the person who wants to consume without feeling complicit. The person who wants to buy things — which is a very human desire — but who also carries a genuine anxiety about what consumption does to the planet.

Patagonia’s famous “Don’t Buy This Jacket” advertisement in the New York Times — which asked customers not to buy its products unless they absolutely needed them, and explained the environmental cost of its own manufacturing — is the masterclass in social identity marketing.

On the surface, it is self-defeating. You are telling your customers not to buy from you. Logically, this should reduce sales.

In practice, it increased sales significantly. Why? Because it answered the social identity need of its target customer with complete precision. The Patagonia customer wanted to buy a $300 jacket and feel good about themselves. Patagonia’s environmentalism, transparency, and “Don’t Buy This Jacket” message gave them the permission structure they needed. This brand shares my values. This brand is honest. I can buy from them without compromising my identity.

The customer bought the jacket. And told all their friends about it.

Note what is happening here: Patagonia is not solving a functional problem for its customer. Gore-Tex from any brand will keep you warm and dry. Patagonia is solving a social-psychological problem — the need to consume without cognitive dissonance.

Case Study Three: How Supreme Manufactured Scarcity to Create a Religion

Supreme is a skateboarding apparel brand. Demographically, its audience is young males, urban, 16–28, with a strong concentration in the US and Japan. This demographic has moderate to low purchasing power.

Yet Supreme built a global brand worth over $2 billion, with customers paying $500 for a hoodie that costs $30 to make, and lining up overnight for the right to spend $150 on a box logo T-shirt.

How? Supreme did not target demographics. It targeted the social identity of the insider — the person who knows about things before they become mainstream, whose taste defines the culture rather than following it. Supreme’s entire model rested on deliberate, manufactured scarcity. It would release (”drop”) a small quantity of new items on a fixed schedule. The items would sell out immediately. The secondary market would drive prices 3-5x higher.

The purchase signal was not “I bought Supreme.” The purchase signal was “I got Supreme.” The distinction is everything. Getting it required knowing about the drop in advance, being in the right network, having the social access to insider information. It was an admission ticket to a cultural in-group.

Supreme’s marketing budget was essentially zero. It did not advertise. The scarcity and the resulting resale market were the marketing. Every sold-out drop was a news story. Every person wearing Supreme was walking advertising that communicated: I was there. I have access. I belong.

What social identity are you changing (increasing, maintaining, reducing)?

Now Apply This to Krispy Kreme

Krispy Kreme’s social identity crisis is clearly readable in the competitive document. The DFD (Delivered Fresh Daily) model puts Krispy Kreme boxes in grocery store bakery sections — next to Entenmann’s on the shelf, competing on freshness. The hub-and-spoke model means the product travels from production facilities to distribution points, with quality (warmth, freshness) degrading along the way.

The McDonald’s partnership collapse is instructive: the idea of putting Krispy Kreme donuts in McDonald’s sent a confused signal. McDonald’s customers are not there for premium treats. They are there for fast, familiar, inexpensive food. A $3 Krispy Kreme donut in a McDonald’s bag sits in a social context that works against the Krispy Kreme brand identity, not for it.

Here is what the data actually tells us about Krispy Kreme’s true social identity, if you read it through the right lens:

Krispy Kreme has an existing social identity that its strategy is not fully leveraging: the shared joy ritual. The box of Krispy Kreme donuts brought to the office meeting. The dozen glazed donuts as a birthday surprise. The family tradition of hot glazed donuts still warm from the light. These are not individual consumption moments — they are social events. They are moments of generosity, celebration, and community.

Krispy Kreme is the friend who shows up to the party with the best thing anyone has brought. The social identity is “I am someone who makes moments better for the people I care about.”

This identity has a name in marketing literature: the gifting economy or social currency through generosity. It is the same identity that drives Costco muffins being bought for office teams, that drives Shake Shack becoming the restaurant you tell people about, that drives craft beer being brought to someone’s house as a host gift rather than just bought for yourself.

The implication for Krispy Kreme’s marketing strategy is profound:

Stop marketing the product. Market the moment. Do not show a donut. Show the face of the person who receives the box. The social identity is not “donut lover.” It is “person who knows how to make people happy.” That identity is not demographic. It cuts across age, income, geography, gender. It speaks to a fundamental human desire: to be the one who brings delight.

Reclaim the freshness signal as theater. Krispy Kreme’s Hot Light — the light that shines in its own stores when donuts are coming fresh off the line — is perhaps the most underleveraged brand asset in the food industry. It is a real-time, location-based, social-media-ready moment of shared joy. The Hot Light is a social event, not a product alert.

Engineer the gift-giving occasion, not the impulse purchase. The Walmart DFD strategy is correct in its ambition (ubiquity) but wrong in its execution framing. The box at Walmart should not look like a grocery item. It should look like a gift. The branding, the packaging, the shelf placement — all of it should say: this is something you buy for someone else. Because when the purchase is framed as a gift, price sensitivity drops dramatically, the social identity benefit activates, and the brand occupies an occasion that Entenmann’s can never compete in.

The Master Framework: How to Think Innovatively About Marketing

The billionaire’s insight — the one Harvard won’t teach, because it cannot be put in a framework without losing its aliveness — is this:

Consumers do not buy products. They rent feelings. Feelings associated to status. Your job is to understand which feeling they are trying to rent, and whether your product is the best vehicle for that rental.

The feeling can be: prestige, belonging, love, excitement, competence, rebellion, comfort, safety, nostalgia. The product is merely the mechanism. The moment you confuse the mechanism for the feeling — the moment you think your business is about donuts rather than shared joy — you have become a commodity. And commodities are priced at margins that slowly destroy you.

PART THREE: THE SINGAPORE MIRACLE

How a City-State Without Water, Without Land, and Without Resources Became the Financial Nerve Center of Asia

Why Singapore Matters More Than Its Size Suggests

Singapore is 733 square kilometers. It has no oil. No significant minerals. No agricultural land. No river large enough to matter. Its population is about 6 million people — roughly the size of Houston, Texas.

And yet it has one of the highest per capita incomes in the world. Its currency — the Singapore dollar — is one of the most stable in Asia. Its port is one of the busiest on earth. Its financial sector manages trillions of dollars of regional and global capital. Its airport was, for decades, rated the world’s best.

How? The honest answer is: through a combination of ruthless strategic clarity about what Singapore’s role in the global economy should be, and a monetary policy framework so sophisticated that it has essentially no equivalent anywhere in the world.

That framework is called the Nominal Effective Exchange Rate (NEER) system, and understanding it teaches you more about monetary economics than most PhD programs do in their first two years.

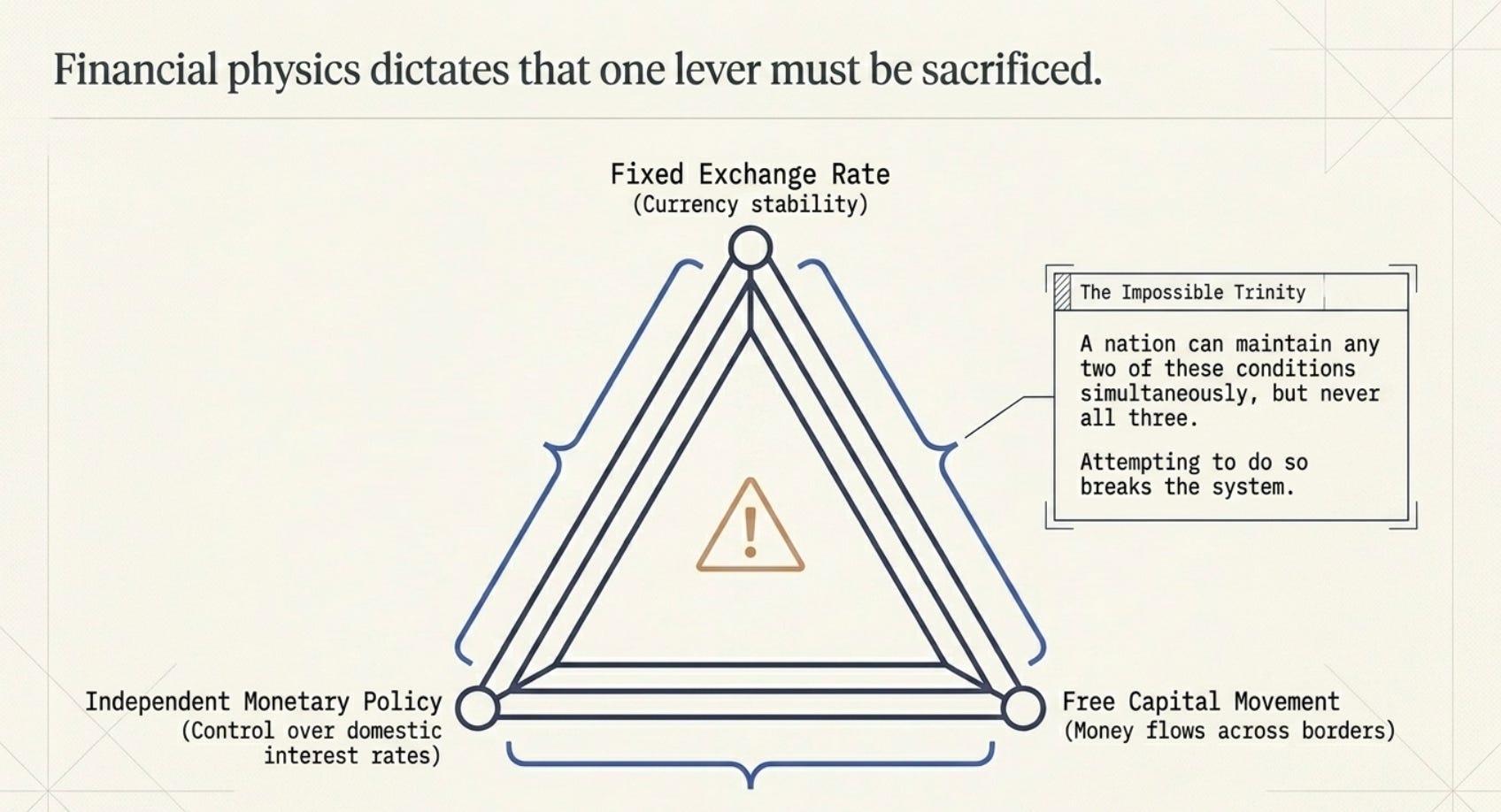

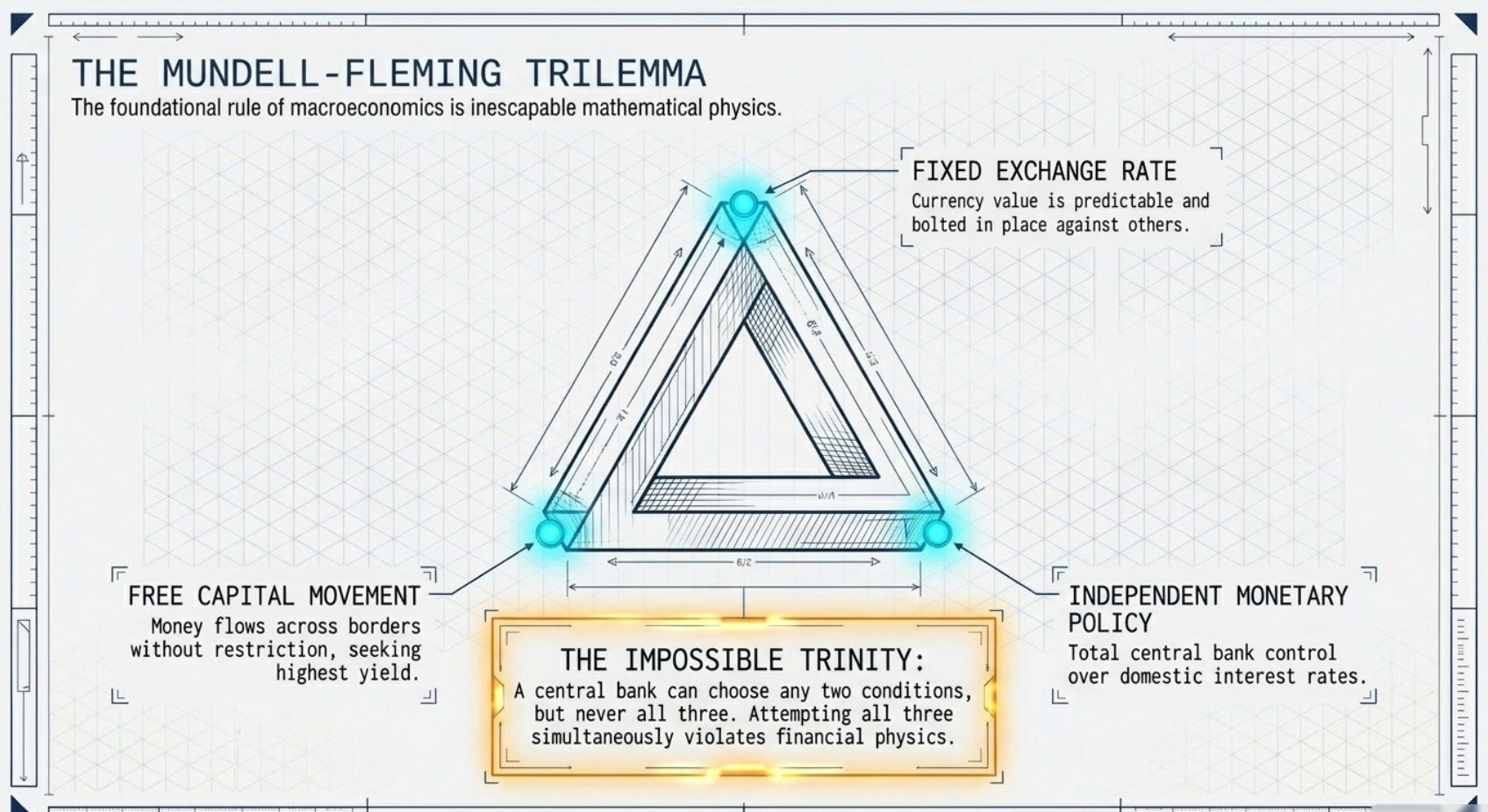

The Impossible Trinity: The Constraint That Governs Every Central Bank on Earth

Before we can understand Singapore’s solution, we need to understand the problem every central bank in the world faces.

The Impossible Trinity — also called the Trilemma — is one of the most elegant and unforgiving theorems in all of economics. It was formalized by economists Robert Mundell and Marcus Fleming in the 1960s, and it states:

A country cannot simultaneously maintain all three of the following:

A fixed exchange rate (your currency’s value relative to other currencies is stable and predictable)

Free capital movement (money can flow freely in and out of the country)

Independent monetary policy (you can set your own interest rates to manage your domestic economy)

You can have any two of these three. Never all three. Pick two, lose one. The Trilemma is not a policy recommendation — it is a mathematical fact. Attempting to maintain all three simultaneously is like trying to simultaneously push and pull the same object in two directions. Physics — or in this case, financial mechanics — prevents it.

The Impossible Trinity, Explained Properly

Before we touch the Trilemma at all, let’s understand what a central bank is for, because the Trilemma is really just a description of the constraints that make a central bank’s job hard.

A central bank has one fundamental job: keep the domestic economy healthy. That means roughly stable prices (not too much inflation), reasonable employment, and steady economic growth. Its primary tool for doing this is the interest rate — specifically, the rate at which it lends money to commercial banks, which then ripples through the entire economy.

When the economy is overheating and inflation is rising, the central bank raises interest rates. Borrowing becomes more expensive. Businesses borrow less, invest less, hire less. Consumers borrow less, spend less. The economy cools. Inflation falls.

When the economy is slowing and unemployment is rising, the central bank cuts interest rates. Borrowing becomes cheaper. Businesses borrow more, invest more, hire more. Consumers borrow more, spend more. The economy picks up.

This is the core tool. And in a closed economy — one that doesn’t trade internationally and doesn’t have capital flowing in and out — it works beautifully. You raise rates, the economy slows. You cut rates, the economy accelerates. Simple, clean, effective.

The moment you open your economy to the rest of the world, something changes. And understanding what changes is the entire Trilemma.

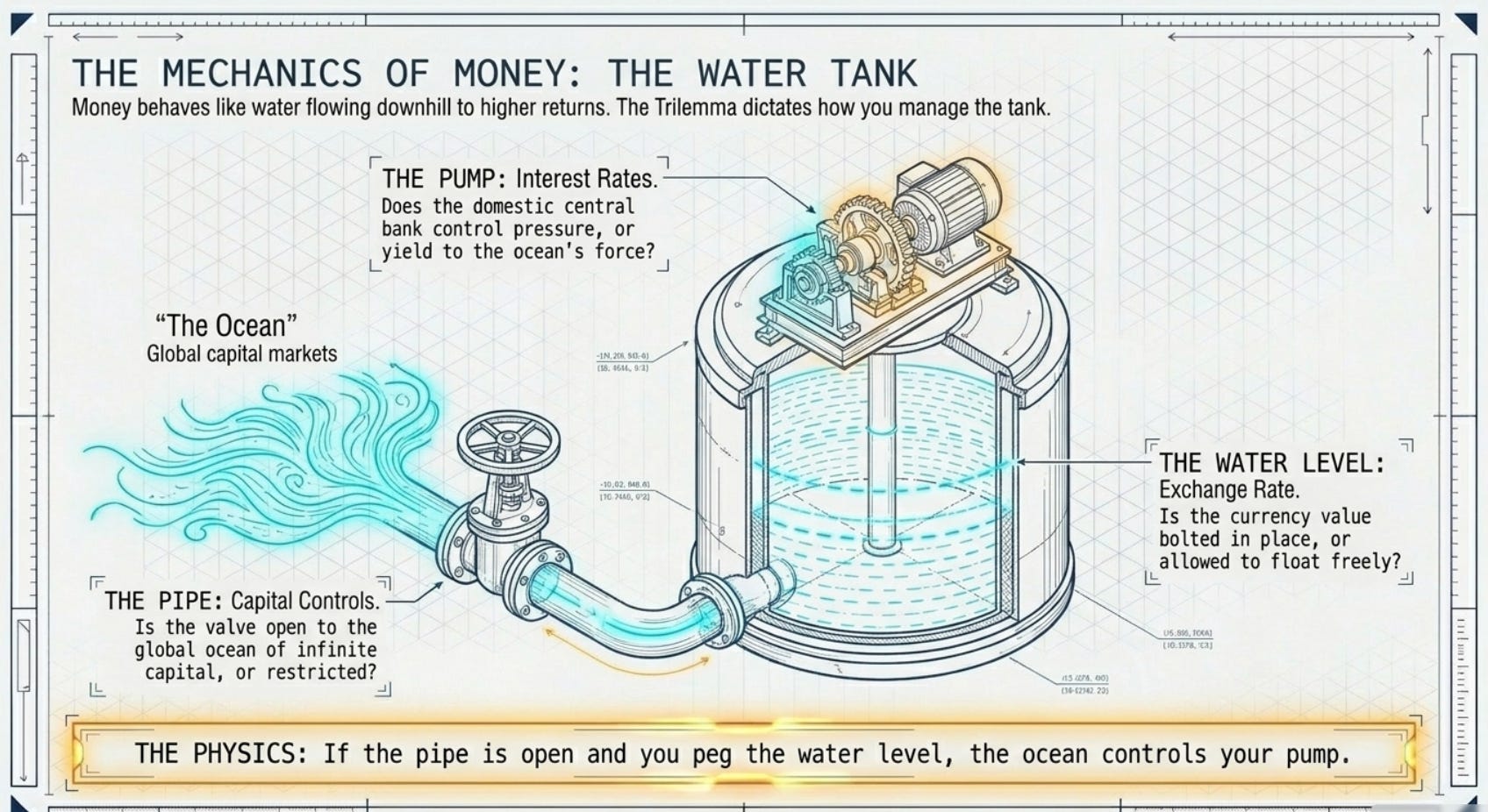

The Water Tank: An Analogy That Actually Works

Imagine your country’s currency as the water level inside a large tank. The water level represents your exchange rate — how much your currency is worth relative to everyone else’s. Higher water = stronger currency. Lower water = weaker currency.

Your central bank is a pump. It can push water in (cut interest rates — more money in the system, currency weakens) or drain water out (raise interest rates — less money in the system, currency strengthens). This is how it controls the water level, and by extension the exchange rate and the general health of the economy.

Now add one more element: your tank has a pipe connecting it to the ocean. The ocean is global capital markets — the enormous pool of money that moves around the world looking for the best return. The ocean is effectively infinite — trillions of dollars managed by pension funds, hedge funds, sovereign wealth funds, and banks worldwide.

Here is the critical insight that makes the Trilemma click: water always flows from high to low. That is physics. And money — like water — always flows toward higher returns. This is not greed. It is arithmetic. If your tank offers a 5% interest rate and the ocean offers a 3% interest rate, money flows from the ocean into your tank until the rates equalize or something stops it.

Now you have three choices about how to manage this tank, and the Trilemma says you can pick any two but never all three.

Choice One: Do you want the water pipe to be wide open (free capital movement), or do you want a valve that you can close (capital controls)?

Choice Two: Do you want to keep the water level fixed (fixed exchange rate), or do you let the water level float (floating exchange rate)?

Choice Three: Do you want to control the water pump yourself (independent monetary policy), or does the ocean’s pressure determine your water level for you?

The Trilemma says: if the pipe is wide open and you insist on keeping the water level fixed, you cannot control the pump. The ocean controls your level. This is not a policy choice. It is physics. Let me show you why with a concrete scenario.

The Moment the Trilemma Bites: A Concrete Example

Suppose your country pegs its currency to the US dollar at a rate of 10 to 1 (your currency is worth one-tenth of a dollar). Your capital markets are open — money flows freely in and out. And now you, as central bank governor, decide to cut interest rates from 5% to 2% to stimulate a slowing economy.

The moment you do this, here is what happens in the next 24 hours.

Every international investor who has money in your country is now earning 2% from you when they could earn 5% from America or elsewhere. So they start moving money out. They sell your bonds, take their cash, convert it back to dollars, and move it to higher-yielding markets. This is not conspiracy — this is just money behaving like water flowing downhill.

All of this selling of your currency puts downward pressure on your exchange rate. Your currency starts weakening — moving away from the 10-to-1 peg you promised to maintain.

Now, to defend the peg, you have two options. First, you can buy your own currency using your foreign exchange reserves — selling dollars and buying your currency to prop up the price. But your reserves are finite. You can do this for weeks, maybe months, but not forever. Second, you can raise interest rates back up to make your currency attractive to investors again, stopping the outflow. But that means abandoning the rate cut you just made to stimulate the economy. You’re back to square one.

Notice what happened: you tried to control the pump (cut rates) while keeping the pipe open (free capital) and the water level fixed (currency peg) — and the ocean simply would not allow it. The moment rates diverged, capital fled, the peg came under attack, and you had to choose: defend the peg or defend the rate cut. You could not do both.

This is the Trilemma. Not as an abstract principle, but as a mechanical, unavoidable consequence of how money moves.

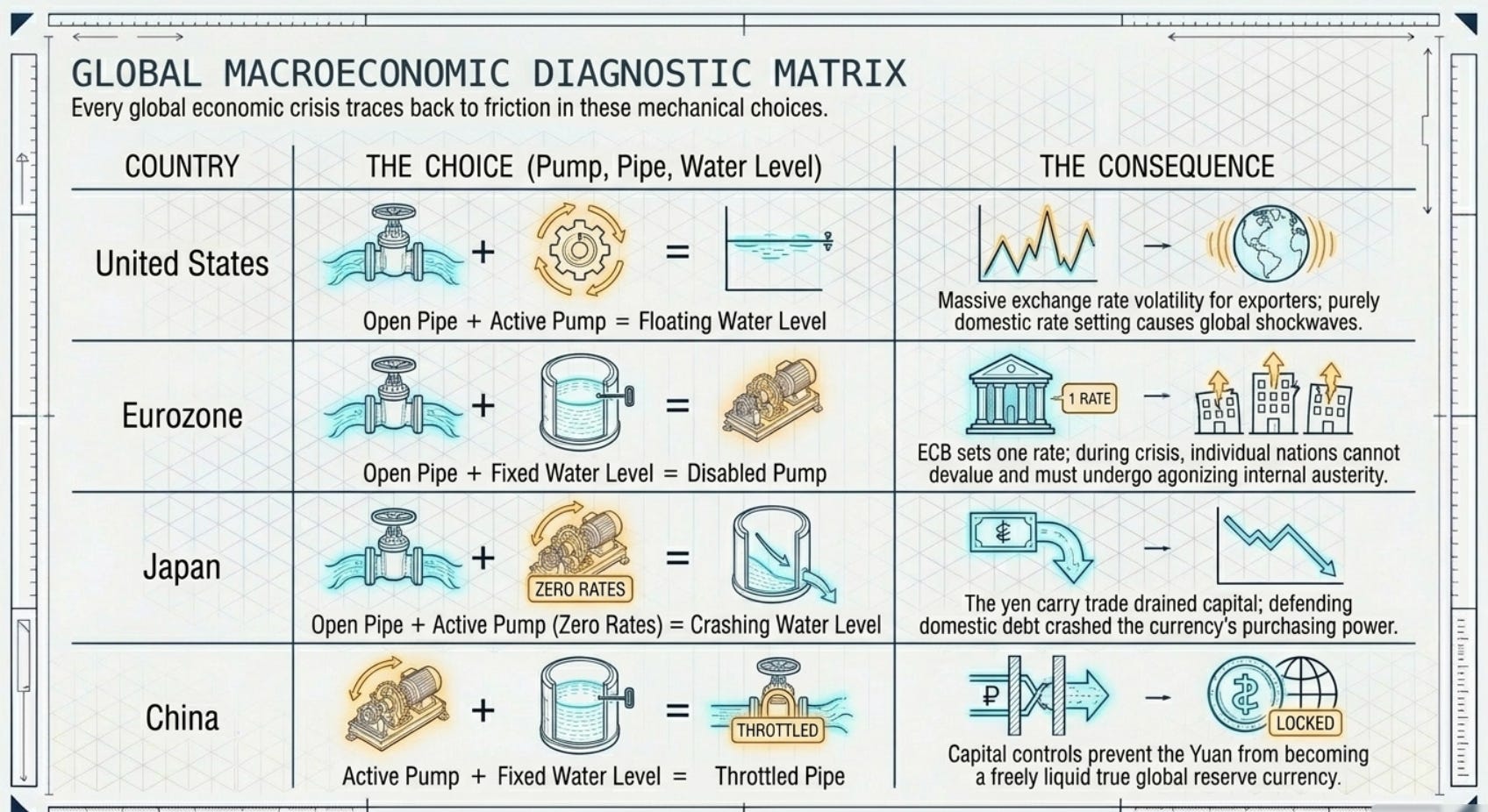

Now Let’s Walk Through Each Country — Using the Tank

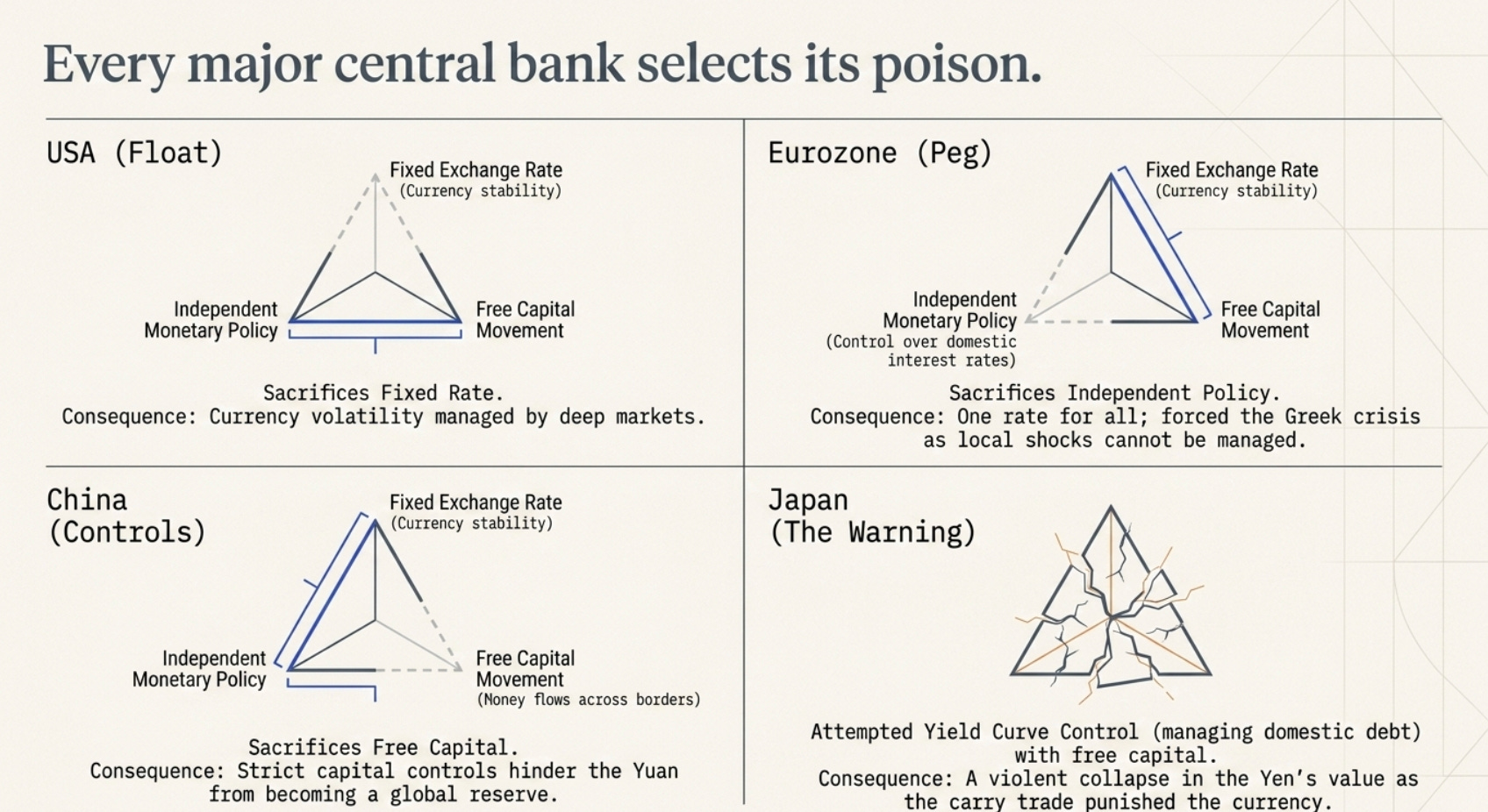

The United States chose: Open pipe + Control the pump = Let the water level float.

America keeps its capital markets completely open — no valve on the pipe, money flows in and out freely. And America insists on controlling its own interest rates — the Federal Reserve sets them based entirely on American economic conditions. The trade-off it accepts is that the dollar’s value floats freely against every other currency. It goes up, it goes down, and American businesses that export or import have to deal with that uncertainty.

The consequence of this choice showed up most dramatically in 2022. The Federal Reserve raised interest rates aggressively to fight American inflation. Higher rates attracted global capital into dollar assets. The dollar strengthened sharply — rising 15-20% against many currencies in a single year. Countries that had borrowed in dollars now found those debts were suddenly much more expensive in local currency terms. Sri Lanka effectively went bankrupt. Pakistan needed an emergency IMF bailout. Argentina entered another debt crisis. The Federal Reserve made its pump decision for purely domestic reasons. The open pipe ensured the consequences rippled globally.

The Eurozone chose: Fixed water level between members + Open pipe = No pump.

This is the boldest experiment in the group. Twenty countries said: we will keep the water level between us permanently identical. One euro is one euro whether you’re in Germany or Greece. And we’ll keep the pipe fully open between member states — capital flows freely.

What they surrendered was the pump. There is no Greek central bank setting Greek interest rates, no Italian central bank managing Italian borrowing costs. The European Central Bank makes one decision for all twenty economies simultaneously.

The catastrophic problem with this reveals itself the moment you ask: what happens when Germany’s economy is booming while Greece’s economy is collapsing at the same time?

The ECB cannot simultaneously raise rates to cool Germany (which would make Greece’s depression worse) and cut rates to revive Greece (which would overheat Germany further). It sets one rate for both. In the 2010-2015 Eurozone crisis, the ECB set rates appropriate for Germany’s relatively stable economy, which were far too high for Greece’s devastated one. Greece could not devalue — the fixed water level agreement prevented it. Greece could not cut rates — it had surrendered the pump. The only adjustment mechanism left was to make Greek wages and prices fall through austerity — cutting government spending, cutting salaries, reducing pensions. This is called internal devaluation, and it is economically equivalent to lowering the water level by removing water one bucket at a time rather than opening a drain. It took years of agonizing pain to accomplish what a currency devaluation could have done in weeks.

Japan chose: Control the pump + Open pipe = Lost control of the water level.

Japan has approximately 250% debt-to-GDP — the highest among developed economies. This matters enormously for the Trilemma because Japan’s government owes so much money that even a modest rise in interest rates would make its debt service costs catastrophically expensive. So Japan kept rates near zero — and even went below zero — for decades to manage this debt burden.

Japan has open capital markets. The pipe is wide. So when Japan kept rates near zero while the rest of the world was offering better returns, money flowed steadily out of Japan through the open pipe. This is the famous yen carry trade: investors borrow yen at near-zero interest, convert it to dollars or Australian dollars or whatever currency offers better yields, invest there, and pocket the difference. This is not complex — it is just exploiting the water differential between tanks.

The mechanical consequence: persistent capital outflow weakened the yen. Between 2021 and 2022, the yen fell from roughly 110 to the dollar to 150 to the dollar — a 36% decline. Japan’s water level crashed. Imports became dramatically more expensive. Japanese citizens found that food, energy, and everyday goods cost far more in dollar terms, eroding living standards.

When Japan finally began raising rates in 2024, the adjustment was violent. Investors who had borrowed yen to invest elsewhere suddenly needed to pay back those loans — which required buying yen. The yen surged sharply in a short period, causing enormous losses for those carry traders, and sending shockwaves through global markets. This is what the Trilemma looks like when it corrects suddenly rather than gradually.

China chose: Fixed water level + Control the pump = Valve on the pipe.

China’s choice is the most explicit and deliberate. It wants to maintain a managed exchange rate — the People’s Bank of China sets a daily fixing rate for the yuan and only allows it to move within a narrow band around that rate. And it wants to set Chinese interest rates based on Chinese economic priorities — not be dictated to by global capital markets.

To have both, it must restrict the pipe. Capital controls in China are extensive: there are limits on how much money Chinese citizens can move abroad, restrictions on foreign investment in Chinese capital markets, and bureaucratic approval processes for large cross-border transactions. The valve is not fully closed, but it is substantially throttled.

The trade-off: the yuan cannot become a true global reserve currency while the pipe is throttled, because international investors will not hold large amounts of an asset they cannot freely convert and repatriate. This is precisely why the yuan represents only about 3% of global reserve holdings despite China having the world’s second or third largest economy. Everyone knows China has enormous economic strength — but if you can’t freely access your yuan-denominated assets when you need to, holding them carries a fundamental liquidity risk.

China is now trying to slowly and carefully open the valve without losing control of the water level — a delicate balancing act that has no good historical precedent for an economy of China’s scale and political structure.

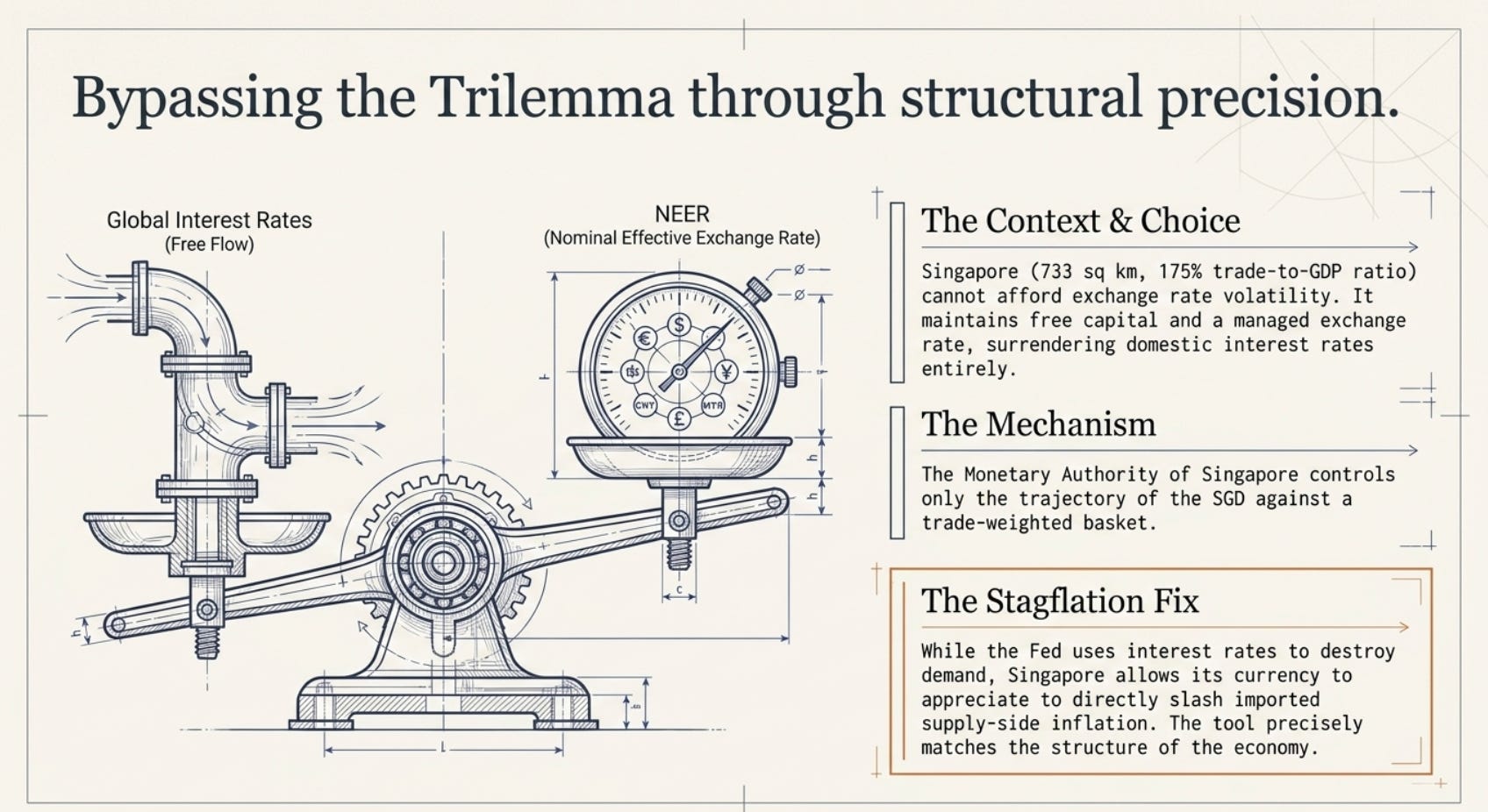

Singapore’s Elegant Escape: The Third Option Nobody Else Thought Of

Now you understand exactly why Singapore’s solution is so clever, because you can see what problem it was solving.

Singapore looked at the Trilemma and recognized its constraints honestly. It is a tiny city-state where roughly 175% of GDP is trade — the entire economy lives and breathes through its connections with the rest of the world. It absolutely cannot close the pipe: doing so would instantly destroy its role as a global financial hub and trading center. Open pipe is non-negotiable.

So Singapore accepted what the Trilemma makes mathematically inevitable: if the pipe is open (free capital flow) and you cannot control the pump (monetary policy), you can only manage your water level (currency). Singapore simply does not set its own interest rates in the way other central banks do. It let go of that tool deliberately. Singaporean interest rates are determined by global market forces — specifically, they track closely to whatever the market demands given global conditions and Singapore’s credit quality.

But here is the creative leap: instead of managing a fixed water level (which proved catastrophic for the Eurozone countries in crisis), Singapore manages a gently moving water level — one that shifts gradually in a controlled direction, rather than being bolted in place.

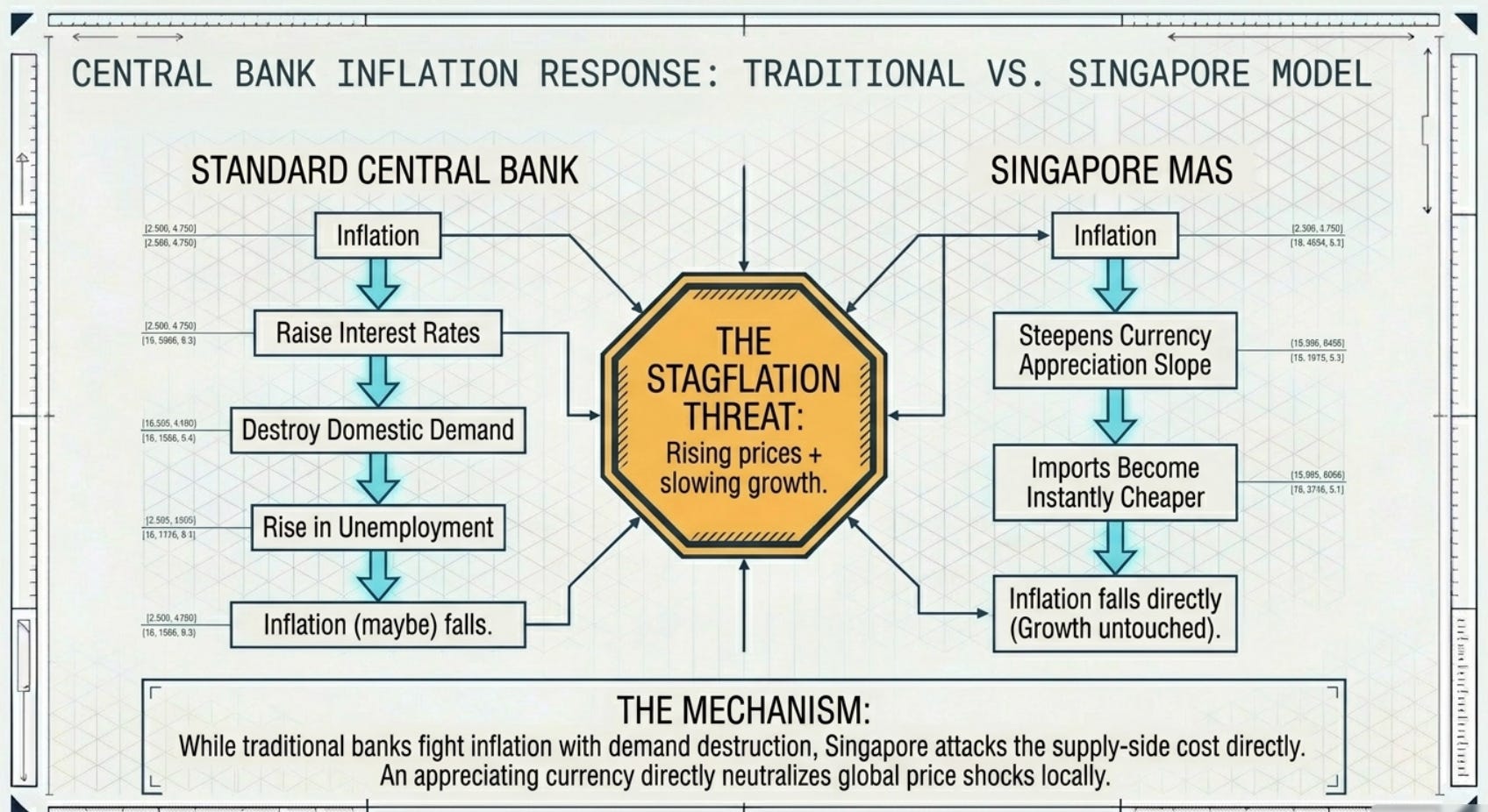

The Monetary Authority of Singapore specifies three things every six months: the center point of the target range, the slope (is the currency being guided to gently appreciate, gently depreciate, or stay flat), and the width of the band (how much can the actual rate deviate from the center before the MAS intervenes). This is the NEER framework — the Nominal Effective Exchange Rate — and the rate in question is not against a single currency but against a basket of currencies weighted by how much Singapore trades with each country.

What this means practically: Singapore fights inflation not by raising interest rates, but by adjusting the slope of the currency upward. When inflation rises — when goods prices are climbing — the MAS steepens the appreciation slope of the Singapore dollar. A stronger Singapore dollar immediately makes imports cheaper in local currency terms. Since Singapore imports almost everything, cheaper imports mean lower prices almost immediately across the whole economy. Inflation falls.

Think about how different this is from what the US or UK does. America fights inflation by raising interest rates — making borrowing more expensive, slowing investment and consumption, accepting higher unemployment as the price of lower prices. This is a slow, blunt instrument that works primarily through demand destruction. Singapore fights inflation by making the currency appreciate — directly reducing the cost of everything imported. It attacks the price level directly, through the supply side, without needing to crash domestic demand or cause unemployment to rise.

This is why Singapore has consistently maintained lower inflation than comparable economies, and why it has managed the stagflation risk — the nightmarish combination of rising prices and slowing growth — better than most. When global commodity prices rise (oil, food, raw materials), a country like the US faces a painful choice: raise rates to fight the inflation and risk recession, or accept the inflation and let it erode purchasing power. Singapore can simply appreciate its currency, making those globally-priced commodities cheaper domestically, without sacrificing domestic growth.

The one thing Singapore truly surrenders — and it surrenders it completely — is the ability to independently set interest rates for domestic stimulus purposes. If Singapore’s economy slows, the MAS can adjust the currency slope downward (allowing gentle depreciation to boost export competitiveness), but it cannot do what America does and slash rates from 5% to near zero to flood the economy with cheap money. The open pipe means global capital markets would immediately arbitrage away any rate that diverges meaningfully from global equivalents.

Singapore decided that this was an acceptable trade-off — indeed, the only sensible trade-off for an economy of its structure. And by making that decision clearly, deliberately, and institutionally (the MAS is among the most credible and independent central banks in the world), Singapore has for fifty years maintained one of the most stable and prosperous monetary environments in Asia.

The One-Sentence Summary to Lock This In

The Trilemma says you have three things you might want — a stable exchange rate, free-flowing capital, and the ability to set your own interest rates — and you get to pick exactly two. America picked free capital and independent rates, so it floats its currency. The Eurozone picked a fixed currency exchange rate between members and free capital, so it surrendered its member nations’ interest rates. Japan picked independent rate management and free capital, and watched its water level crash. China picked a managed currency rate and independent independent rates, so it has to regulate its capital flows (no free capital). And Singapore picked free capital and a managed (but not rigidly fixed) exchange rate, and voluntarily surrendered interest rate control — replacing that lost tool with the more precise and better-suited instrument of exchange rate slope management.

Every monetary crisis you will ever read about — the 1992 British pound crisis, the 1994 Mexican peso crisis, the 1997 Asian financial crisis, the 2010-2015 Eurozone sovereign debt crisis — is, at its core, a story of a country that tried to have all three things at once.

PART FOUR: THE CASINO BUILT ON THE ECONOMY’S ROOF

When Finance Stops Serving Business and Starts Eating It

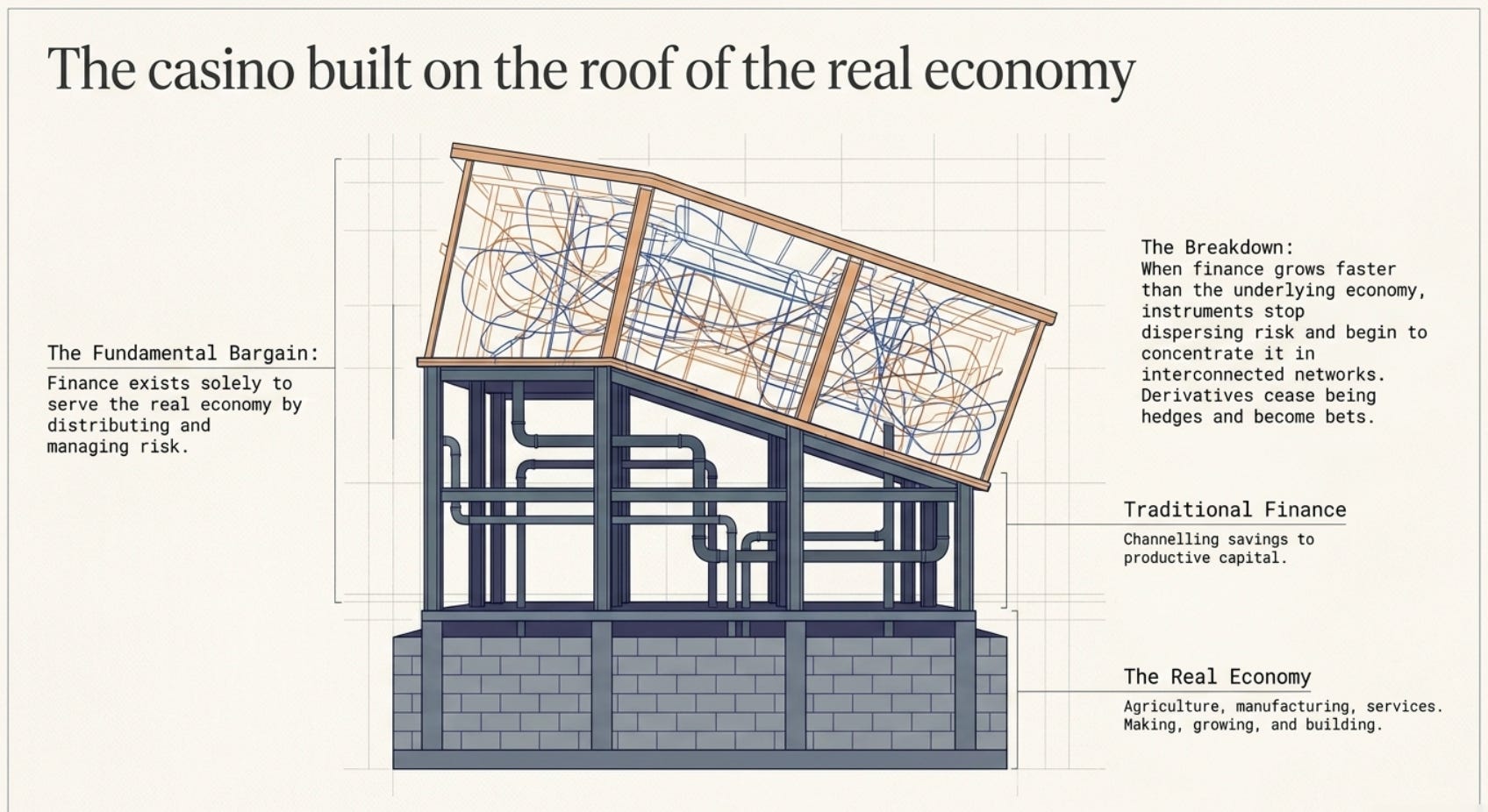

The Fundamental Bargain of Finance

There is a bargain at the heart of capitalism that almost nobody teaches explicitly, but which everything depends on.

The bargain is this: finance exists to serve the real economy. The real economy is people making things, growing things, building things, providing services — creating genuine value in the world. Finance — banking, insurance, investment — exists to channel the savings of those who have more than they need today toward those who need capital to create more value tomorrow. It is a service industry. A critical one.

When a bank lends money to a small business, it is performing this service. When a stock market allows investors to fund a company’s growth, it is performing this service. When an insurance company allows a farmer to plant without the existential risk of a bad harvest destroying them, it is performing this service.

The bargain works when finance serves the economy. It breaks when finance becomes the economy — when financial instruments stop being vehicles for channeling capital into productive activity and become ends in themselves, generating profits by trading with other financial instruments, creating complexity that nobody fully understands, and distributing risk in ways that concentrate it rather than disperse it.

When finance grows faster than the underlying economy it is supposed to serve, this breakdown accelerates. And the most dangerous tools in the breakdown are derivatives — financial instruments whose value is derived from the value of something else. Understanding three specific derivatives that are quietly building risk in today’s market is perhaps the most important financial literacy you can develop.

Derivatives: The Brilliant Idea That Keeps Being Abused

A derivative is not inherently evil. In its original, pure form, it is an extraordinarily useful risk management tool.

A farmer knows that oil prices will be in six months. It plants its crop now. If oil prices fall by the time the harvest comes, it might lose money on the crop that was expensive to produce. To protect against this, the farmer sells an oil futures contract — a derivative — that locks in the price today. If oil falls, the derivative gains in value, offsetting the loss on physical oil. The risk is managed. The farmer can plant without existential uncertainty.

This is a derivative performing exactly the function finance is supposed to perform: reducing uncertainty so that real economic activity (farming) can proceed more confidently.

The problem begins when derivatives are no longer used to hedge real economic risks but to create financial risks — when the derivative market becomes larger than the underlying market it is supposed to represent. When more oil is bought and sold in futures contracts than physically exists. When more credit risk is sold through credit default swaps than there are underlying bonds to insure.

At this point, derivatives stop dispersing risk and start concentrating it in hidden, opaque, interconnected ways. And when the underlying asset moves unexpectedly, the entire derivative edifice can collapse in ways that nobody anticipated, because nobody fully understood the aggregate exposure.

This is exactly what happened in 2008 with mortgage-backed securities and credit default swaps. Let us now examine the three modern instruments that are quietly building similar risks today.

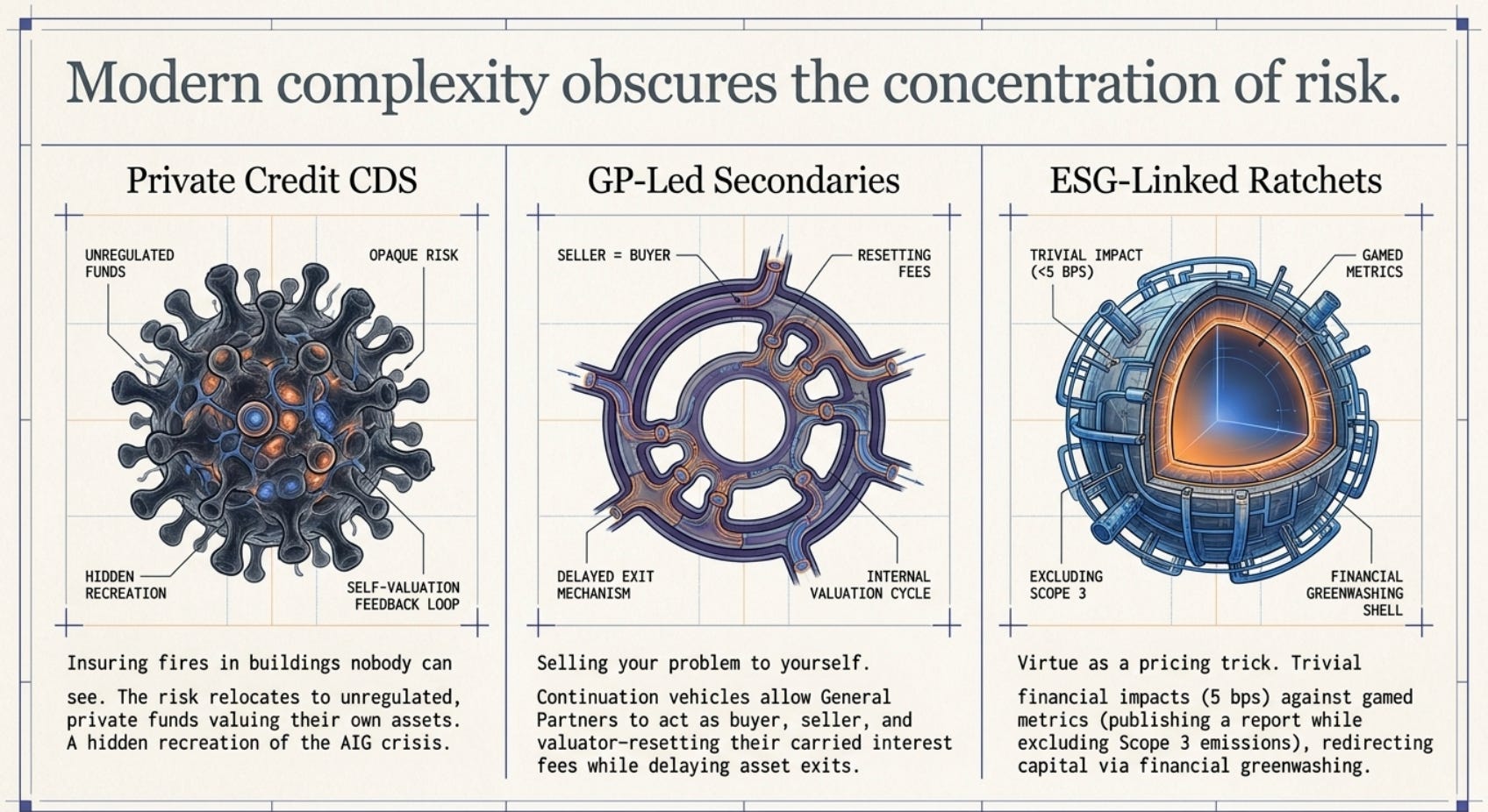

Instrument One: Private Credit Default Swaps — Insuring Against Fires in Buildings Nobody Can See

A Credit Default Swap (CDS) is essentially insurance against a borrower defaulting on its debt. You hold a bond issued by Company X. You are worried Company X might not be able to repay it. You buy a CDS from a counterparty who promises: if Company X defaults, we will pay you the face value of the bond. In exchange, you pay them a regular premium. This is conceptually identical to house insurance: regular premiums in exchange for protection against a catastrophic event.

Public CDS markets — on publicly traded bonds of listed companies — are regulated, reported, and reasonably transparent. Prices are available. Exposures can be tracked.

Private credit default swaps are a different species. They are customized, negotiated contracts between private parties, referencing privately held debt — loans made by private credit funds to private companies, outside the regulated banking system. This is the fastest-growing corner of global finance: private credit has grown from roughly $500 billion in 2012 to over $1.7 trillion by 2024, with private CDS exposure layered on top of this.

The problem with private credit CDS is what you do not know and cannot find out:

You do not know the total exposure in the system. Private CDS are not centrally reported. There is no comprehensive dataset. Regulators do not have a clear picture of who owes whom what in the event of defaults.

You do not know the quality of the underlying reference debt. Private loans are not rated by public agencies. They are valued by the very private credit managers who made them — a structural conflict of interest that tends to produce optimistic valuations during benign credit conditions and sudden, simultaneous write-downs when conditions deteriorate.

You do not know the interconnections. When many private credit managers have sold CDS protection to each other — each believing they are managing their risk — the system may actually be concentrating it. A default cascade in one sector of private credit can trigger margin calls on CDS across apparently unrelated funds.

The 2008 crisis had a villain that the public learned: AIG, the insurance giant, had sold $440 billion of credit default swaps insuring mortgage bonds — far more than it had capital to cover if those bonds defaulted. When the bonds defaulted, AIG was instantly insolvent. The American government had to bail it out to prevent the cascade from destroying the entire financial system.

Private credit CDS today is AIG’s story waiting to repeat, with two important differences: the actors are private funds rather than regulated institutions, so the exposure is less visible; and the underlying debt is private credit rather than public mortgages, so the quality of the underlying assets is even harder to assess.

The fundamental lesson: risk does not disappear when you insure it. It relocates. The question is always: where does the risk live now, and does the entity holding it have the capital to absorb a loss? In public markets, this question is answerable. In private markets, it often is not.

Instrument Two: GP-Led Secondaries (Continuation Vehicles) — The Art of Selling Your Problem to Yourself

This one requires more context, because it exists in the specialized world of private equity and most people have never encountered it. But it is becoming systemically important, and understanding it reveals something profound about how financial incentives distort behavior.

In a normal private equity fund, the mechanics are straightforward:

A General Partner (GP) — the private equity firm — raises a fund from Limited Partners (LPs) — pension funds, sovereign wealth funds, university endowments, insurance companies. The GP has typically 10 years to invest the capital, generate returns, and return the money to LPs. The GP’s incentive structure is called carried interest — typically, the GP keeps 20% of the profits above a certain return threshold. The other 80% goes to LPs.

The system is designed so that the GP’s interests are aligned with the LPs: the GP only makes real money if the investments perform well and are successfully exited (sold) at good prices within the fund’s life.

Here is the tension that creates GP-Led Secondaries: private equity funds are now holding assets for longer than originally planned. The typical fund life has effectively extended from 10 to 12-15 years, because exit markets have been difficult. LPs are getting frustrated — their capital is locked up, their returns are unrealized, and they need liquidity for their own obligations.

The GP faces a dilemma. It has portfolio companies it genuinely believes in — or at least claims to. It does not want to sell them at a discount in a difficult market. But its LPs need their money back.

The Continuation Vehicle (GP-Led Secondary) is the solution the industry invented:

The GP creates a new fund — the continuation vehicle. It then sells the assets from the old fund into the new fund. New investors come in to provide liquidity to the existing LPs who want out. The GP continues managing the same assets, but now for a fresh set of investors with a fresh set of fees and carried interest.

Read that again slowly, because the conflict of interest is serious: the GP is simultaneously the seller (representing the old fund), the buyer (representing the new continuation vehicle), and the fund manager of both. It sets the price at which the assets transfer from old to new. And it earns a new carry arrangement on the continuation vehicle.

In a world of perfect information and perfect GP integrity, this structure might be fine. In the real world, several problems emerge:

The valuation problem. The GP values the assets at a price that serves its interests — high enough that existing LPs get reasonable returns (keeping their goodwill for the next fundraise), low enough that the continuation vehicle has room to make its returns. There is no independent, arms-length party determining the fair price.

The carry reset problem. The old fund’s carry may be underwater or fully earned. The continuation vehicle resets the clock — the GP gets a fresh carried interest opportunity on assets it has already managed for a decade. This creates an incentive to transfer assets into continuation vehicles rather than exit them, even when exiting would serve LPs better.

The quality selection problem. GPs have discretion over which assets go into the continuation vehicle. The rational GP puts in the assets it believes will appreciate most — which are also the assets that existing LPs would most want to stay invested in. The assets sold off directly to new buyers tend to be the lower-quality assets. LPs who accept the continuation vehicle option are thus retaining exposure to the GP’s most promising assets (good), but they are doing so through a vehicle where price and terms were determined by the GP they are depending on (bad).

The systemic opacity problem. When billions of private equity assets move through continuation vehicles, valuations are not market-tested. The private equity industry’s reported returns — which are used by pension funds to justify their allocation to this asset class — are built on these self-determined valuations. When market conditions change and the assets are eventually tested against actual buyer prices, the reported returns may prove significantly optimistic.

The deeper lesson here is one of incentive architecture: financial structures create incentives, and those incentives shape behavior. When the incentive structure of continuation vehicles rewards GPs for extending their management period and resetting their carry, GPs will find reasons to believe their assets need more time — regardless of whether more time actually serves investors. The instrument is not inherently fraudulent. But it is structurally misaligned, and structurally misaligned instruments cause systemic problems when they become widespread enough.

Instrument Three: ESG-Linked Derivatives and Margin Ratchets

ESG-linked financing — loans and bonds where the interest rate is tied to the borrower’s Environmental, Social, and Governance performance — was presented to the world as capitalism’s conscience. Companies that improved their ESG metrics would be rewarded with cheaper borrowing. Those that failed to meet targets would pay more. Market forces would be harnessed for social good.

The reality of ESG-linked derivatives and margin ratchets has revealed something more complicated and less virtuous.

A margin ratchet in ESG financing works like this: a company borrows money under a revolving credit facility or term loan. The interest rate (margin) is linked to the company’s performance against agreed ESG metrics — carbon emissions, board diversity, safety records. If the company hits its targets, the margin falls by, say, 5 basis points (0.05%). If it misses targets, the margin rises by 5 basis points.

In principle: elegant. In practice: trivial in financial impact, easily gamed in metric design, and providing false credibility to borrowers who have not fundamentally changed their business.

The first problem: materiality. A 5 basis point change on a $500 million loan is $250,000 per year. For a large corporation generating billions in revenue, this is a rounding error. The incentive to genuinely transform business practices for a $250,000 annual saving is negligible. The ESG-linked structure creates a marketing benefit — the company can announce it has “ESG-linked financing” and signal its commitment to sustainability — at a cost that is operationally irrelevant.

The second problem: metric selection. The borrower and lender negotiate the ESG metrics together. The borrower has every incentive to select metrics that are easy to hit and difficult to verify. Metrics based on process (we published an ESG report) rather than outcome (our actual carbon emissions fell by X tons) are common. Scope 1 and Scope 2 carbon metrics (direct emissions and purchased energy emissions) are used while Scope 3 emissions (the full supply chain impact — often 70-90% of a company’s total carbon footprint) are excluded.

The third problem: derivative layering. On top of simple ESG-linked loans, more complex instruments have been constructed: ESG-linked derivatives where the payoff is tied to an index of ESG scores, ESG credit default swaps where the protection triggers on an ESG-related event (regulatory action, emissions violation), and structured products where tranches of ESG debt are bundled and resold with credit enhancement.

Each layer adds complexity. Each layer adds parties who have expertise in structuring but potentially less expertise in the underlying ESG claims. Each layer creates a gap between what the instrument is marketed as (ESG-positive financing that advances sustainability goals) and what it actually does (creates a modest interest rate ratchet against easily gamed metrics, with fee income at each structuring layer).

This is not merely financial cynicism. It has a name: greenwashing at the financial instrument level. And it has a systemic consequence: it redirects capital that might have funded genuine ESG innovation toward companies that are adept at meeting derivative trigger criteria, regardless of their actual environmental impact.

The deeper problem: when ESG-linked derivatives become large enough, they create perverse incentives at the corporate level. A company that has structured its borrowing costs around specific ESG metrics has an incentive to manage those metrics — not the underlying ESG performance. The metric becomes the goal, replacing the outcome it was supposed to measure. This is precisely Goodhart’s Law: when a measure becomes a target, it ceases to be a good measure.

The Grand Unified Theory: Why All Three Instruments Share the Same Root Cause

Private Credit CDS, GP-Led Continuation Vehicles, and ESG-Linked Margin Ratchets seem like three separate problems in three separate corners of the financial world. But they share the same root cause, and understanding that root cause is the real lesson of this section.

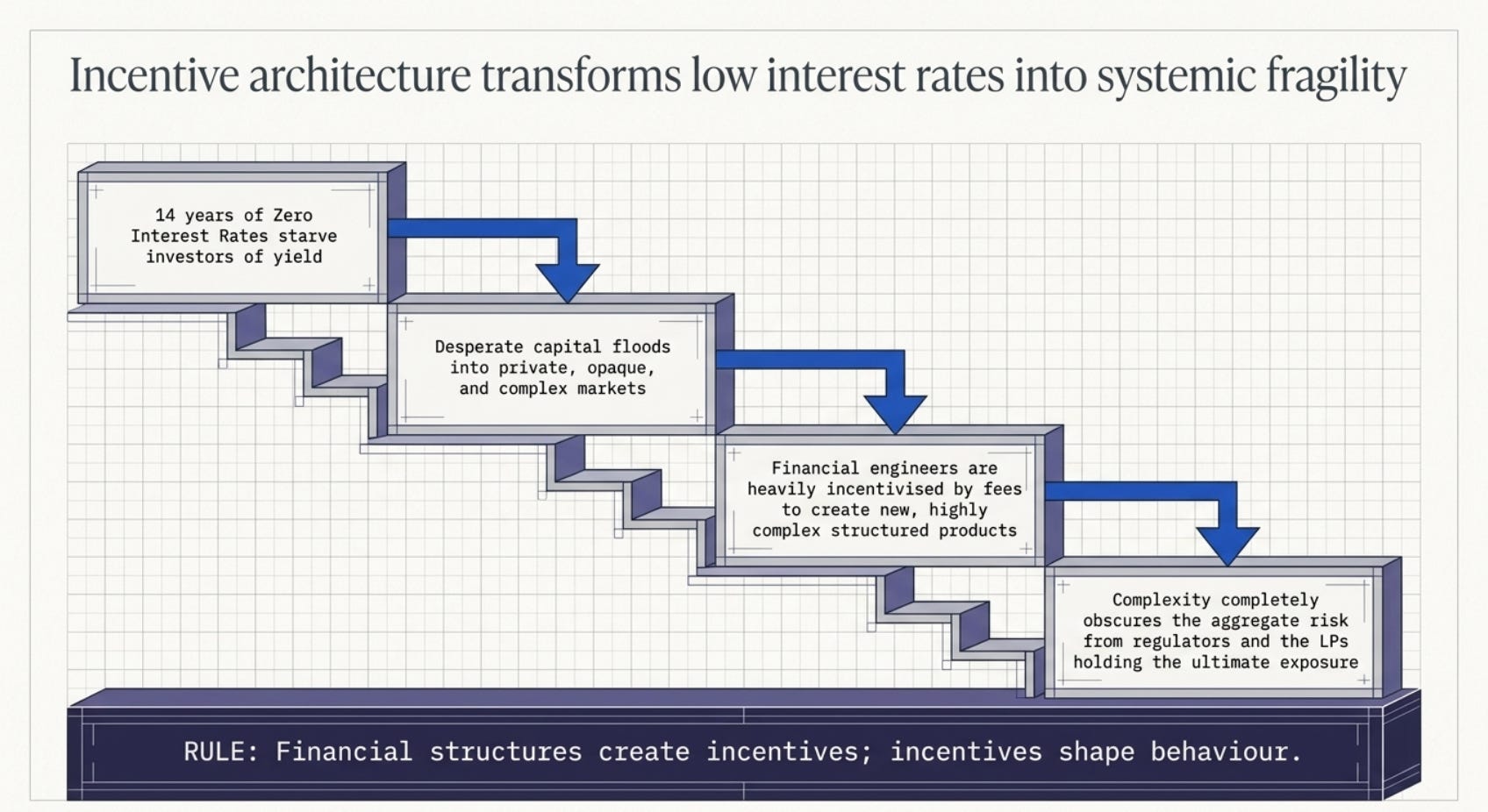

They are all products of finance growing faster than the economy it serves, in an environment of sustained low interest rates.

Here is the chain of causation:

When interest rates are near zero for over a decade (2009–2022), traditional financial instruments generate almost no return. A pension fund that needs 7% annual returns to meet its obligations cannot get there from government bonds yielding 1%. It must search for yield in less familiar, less liquid, less transparent markets.

This search for yield flows into private credit, private equity, and structured products. Capital floods into these markets, creating enormous fee income for the managers of these strategies. Enormous fee income creates enormous incentives to innovate — not in the sense of creating genuinely better instruments, but in the sense of creating new instruments that can be sold to yield-hungry investors.

The innovation is financial engineering, not economic value creation. Private credit CDS are created not because the world needs more insurance against private debt defaults, but because there is fee income in structuring and selling them. Continuation vehicles are created not because the world needs longer holding periods for private equity assets, but because GPs earn more fees by extending their management and resetting their carry. ESG-linked ratchets are created not because the world needs modest interest rate adjustments tied to easily gamed sustainability metrics, but because banks earn structuring fees and companies earn credibility at minimal cost.

The result: an ever-more-complex financial system in which the distance between where capital originates (pension fund members, insurance policyholders, ordinary savers) and where risk ultimately lives (private credit defaults, overvalued continuation vehicle assets, ESG metrics that measure nothing) is so great that nobody in the chain can trace it.

This is how financial crises are built. Not with dramatic announcements of recklessness, but with the quiet accumulation of complexity, each layer of which makes sense to the immediate parties while obscuring the aggregate risk from everyone with the authority to do something about it.

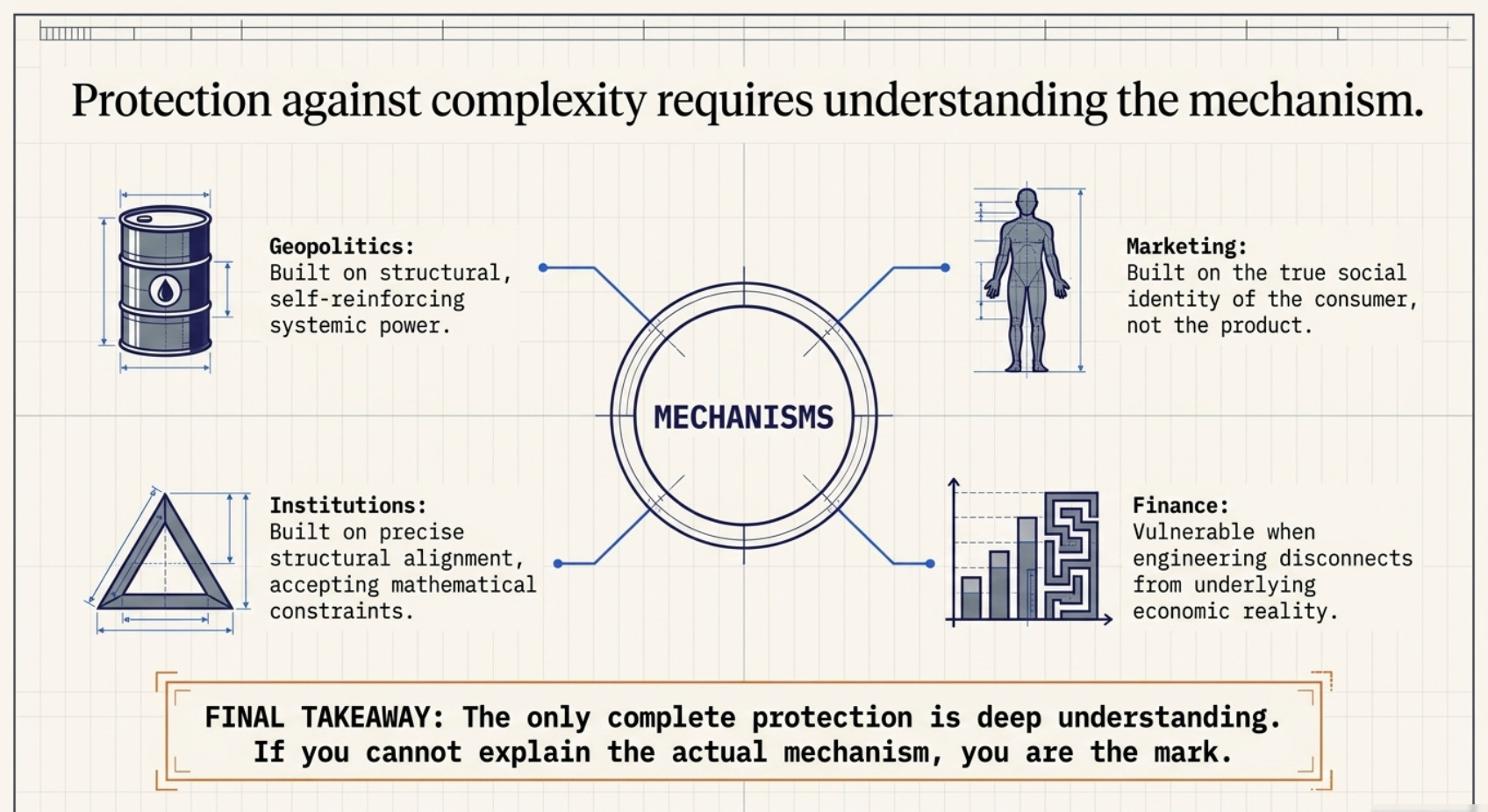

For investors: the most dangerous words in finance are “trust me, it’s complex but it works.” Every major financial crisis in the past 50 years has been preceded by the widespread belief that a new category of instrument was genuinely safer than it appeared, because smart people had engineered the risk away. The risk was not engineered away. It was hidden.

The only complete protection against financial complexity is deep understanding or deliberate abstention. Invest in what you understand. If you cannot understand something after a genuine effort, treat that as evidence that the instrument is not designed for your benefit.

Sources and Recommended Reading: Saifedean Ammous, “The Bitcoin Standard” (petrodollar context); Thorstein Veblen, “The Theory of the Leisure Class” (social identity as consumption driver); Eugene Fama and Kenneth French, foundational papers on capital market efficiency; MAS Monetary Policy Statements 2000–2024; Hyman Minsky, “Stabilizing an Unstable Economy” (financial fragility theory); Adam Tooze, “Crashed” (2008 crisis anatomy); Robert Kiyosaki’s conceptual framework on asset vs. liability thinking — see the original, not the popularizations; and the SEC EDGAR filings and earnings call transcripts cited throughout the Krispy Kreme competitive analysis referenced in the preparation of Part Two.