⛏️ A Basic Commodity Primer

How a Laptop Full of Secrets Revealed the Hidden Architecture of Commodity Markets

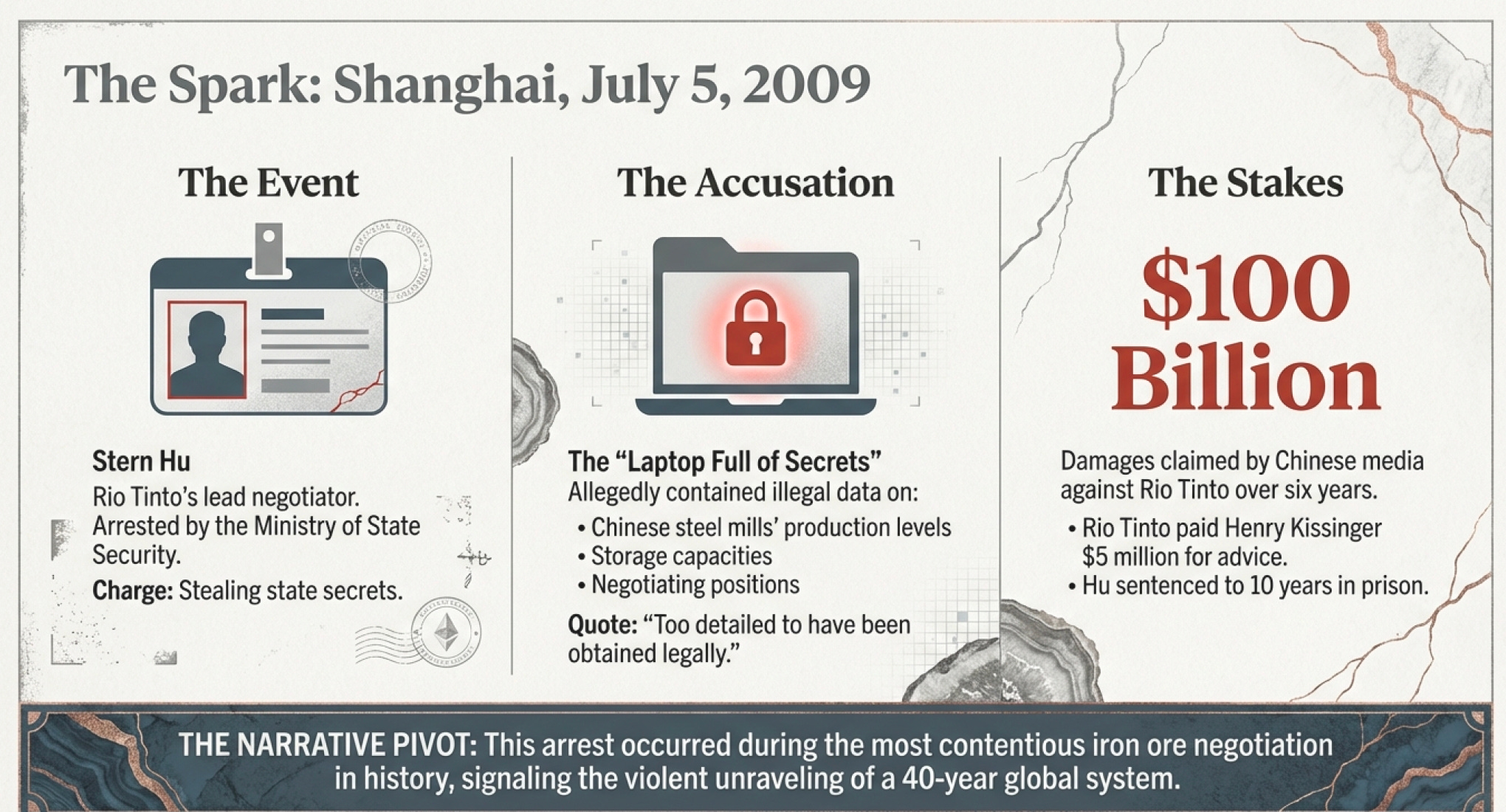

Shanghai, July 5, 2009

Stern Hu didn’t know it that Sunday morning, but he was about to become the most famous commodity trader in the world.

The Australian mining executive—born in Tianjin, trained at Peking University, Rio Tinto’s general manager for iron ore in Shanghai and their lead price negotiator with Chinese steel mills—was arrested by China’s Ministry of State Security along with three Chinese colleagues. The initial charge: stealing state secrets. The accusation: that Hu’s laptop contained information about Chinese steel mills’ production levels, storage capacities, and negotiating positions that was “too detailed to have been obtained legally.”

Within weeks, Chinese state media would accuse Rio Tinto of causing $100 billion in damages to the Chinese economy over six years. Rio Tinto would pay Henry Kissinger $5 million to advise them on damage control. And by March 2010, Hu would be sentenced to 10 years in prison for bribery and stealing commercial secrets—though notably, the espionage charges would be quietly dropped.

But here’s what makes this more than just another corporate scandal: Stern Hu’s arrest happened to occur during the most contentious iron ore price negotiations in modern history, just weeks after those negotiations had spectacularly collapsed, and mere months after Rio Tinto had walked away from a $19.5 billion investment from China’s state-owned Chinalco—a decision that enraged Beijing.

The timing was, shall we say, interesting.

What unfolded over the next nine months wasn’t just a legal drama. It was the violent unraveling of a 40-year system that had kept commodity markets stable, civilized, and predictable. And buried in the wreckage of that system—in the accusations, the laptop data, the failed negotiations, and the prison sentence—lies the clearest X-ray image you’ll ever see of how commodity markets actually work, who controls them, and why some moats in business are measured not in competitive advantages, but in the geological accidents of deep time.

This is that story. And it starts, like so many commodity stories do, with a hole in the ground.

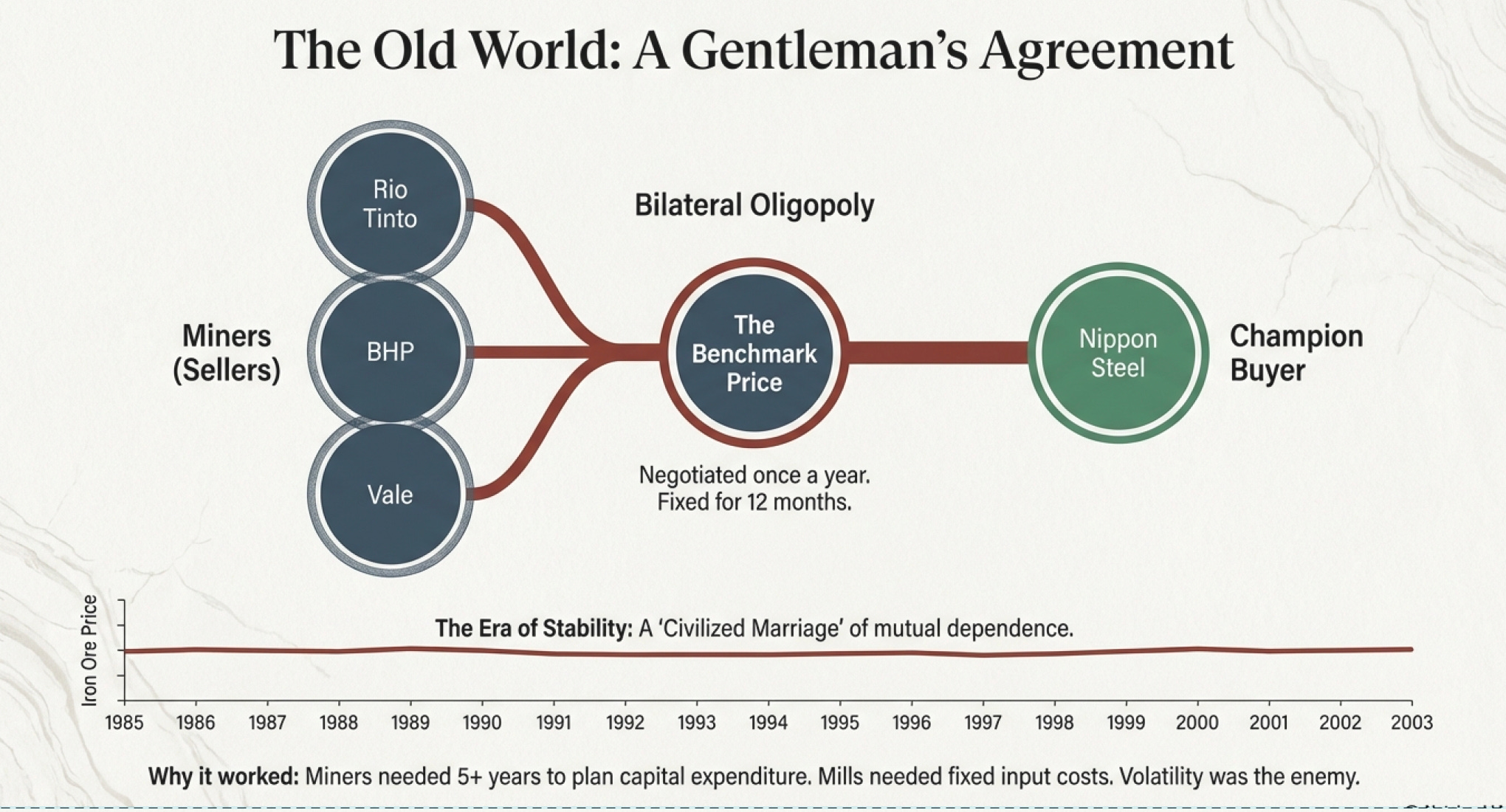

The Gentleman’s Agreement: How to Run a Cartel Without Calling It One

For 40 years before Stern Hu’s arrest, the global iron ore market had operated under a system so elegant, so mutually beneficial, and so obviously cartel-like that everyone simply agreed never to use the word “cartel” to describe it.

Here’s how it worked:

Every year, three mining companies—Rio Tinto and BHP Billiton of Australia, and Vale of Brazil—would sit down with representatives from major steelmakers to negotiate a “benchmark price” for iron ore. Traditionally, the negotiation would be led by Japan’s Nippon Steel (representing buyers) and Australia’s Rio Tinto (representing sellers). Once these champion negotiators reached an agreement, that price would become the benchmark that every other steel mill and mining company would use for the next 12 months.

Notice what’s happening here: The sellers spoke with one voice. The buyers spoke with one voice. And everybody honored the result.

It was, in the language of economics, a beautiful example of bilateral oligopoly—a market dominated by a small number of sellers facing a small number of buyers, all sophisticated enough to realize that peaceful cooperation beats mutually assured commercial destruction.

Why did it work?

Because both sides needed stability. Steel mills need to know their input costs to plan production and price contracts. Mining companies need to justify investments in projects that take five years minimum to build and decades to pay off. Violently fluctuating prices help nobody except speculators, and neither steel mills nor miners wanted to hand their economic fate to traders with Excel spreadsheets.

The system kept iron ore prices remarkably stable in nominal terms from the late 1980s through the early 2000s. It was, in its own way, the commodity market equivalent of a good marriage: built on mutual dependence, maintained through regular communication, occasionally boring but reliably functional.

Then China woke up.

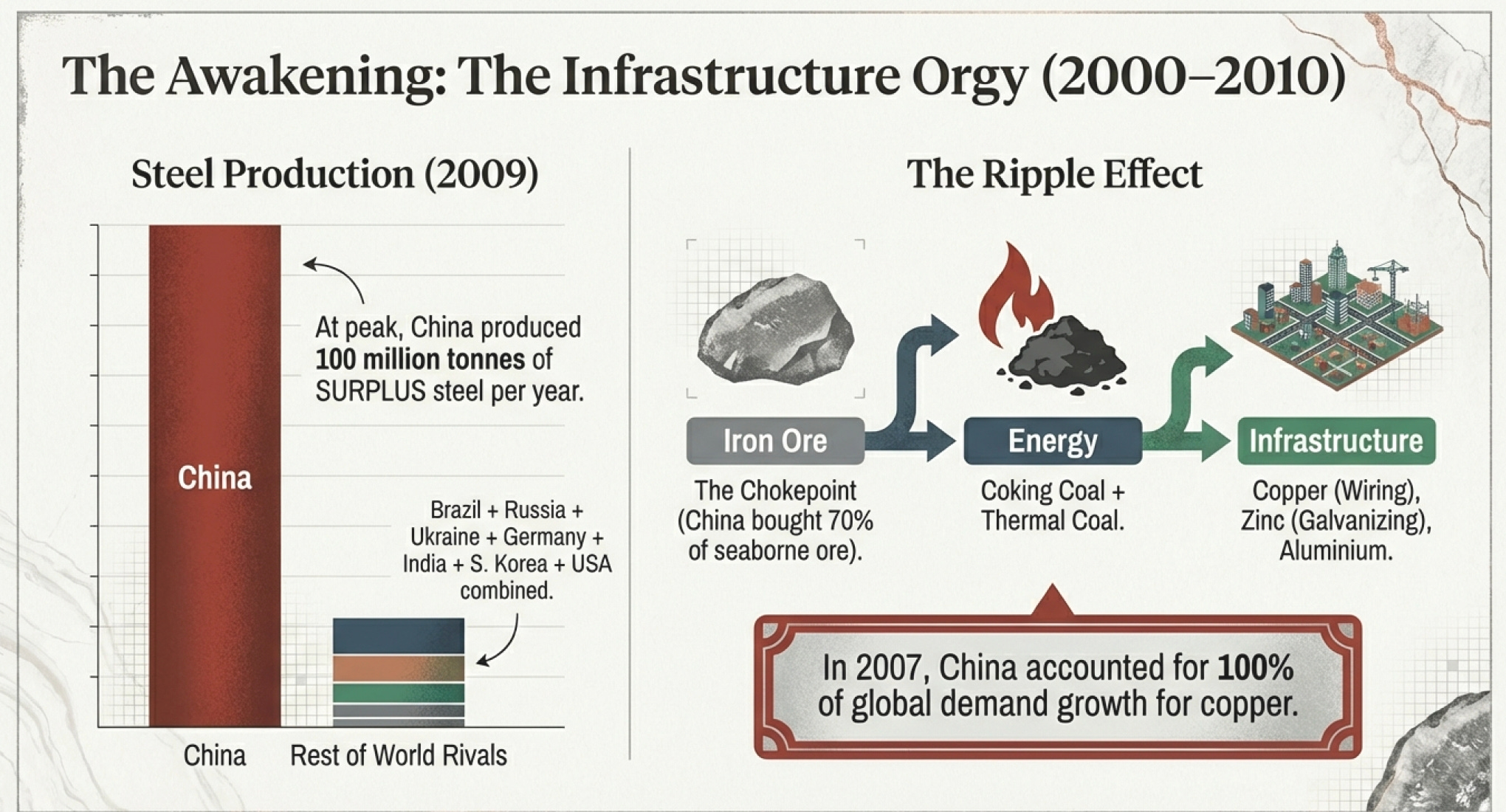

The Infrastructure Orgy: What Happens When You Try to Build 800 Cities at Once

Between 2000 and 2010, China undertook the largest, fastest, most resource-intensive infrastructure build in human history.

The numbers are almost meaningless because they’re too large to visualize: By 2009, China produced more steel than Brazil, Russia, Ukraine, Germany, India, South Korea, and the United States combined. Over 700 steel mills. Nearly 7,000 companies bending, shaping, and forming steel. At the peak, China was producing over 100 million metric tons of surplus steel per year—more than total U.S. production.

Now here’s a thought experiment: What does it take to make steel?

Start with iron ore. To produce one ton of steel, you need about 1.6 tons of iron ore. But that ore has to come from somewhere—and a typical ore contains only 0.5% to 2% copper, with similar dilution factors for iron. So you’re hauling massive quantities of rock out of the ground just to get the metal-bearing ore.

Then you need to get that ore from Australia or Brazil to China. That requires ships—big ships, specialized for bulk cargo, sailing across oceans. Every ship needs fuel (oil). Every port needs infrastructure to load and unload hundreds of millions of tons per year.

Once the ore arrives in China, you need to turn it into steel. The most common method is the basic oxygen furnace, which requires coking coal—a special metallurgical grade of coal that’s converted into coke for steelmaking. Metallurgical coal represents only 15% of global coal usage but it’s absolutely essential. China had to import massive quantities from Australia, Canada, and the U.S.

But wait—you can’t just run steel mills. You need electricity to power them. In 2009, 80% of China’s electricity came from coal—thermal coal this time, accounting for 85% of coal usage. So now you need even more coal, plus the infrastructure to burn it.

And you’re still not done. What are you building with all this steel?

Buildings. Bridges. Power lines. Electrical grids. And all of that requires copper—prized for its electrical conductivity and corrosion resistance. During the 2007 bull market, China accounted for nearly 100% of global demand growth for copper. One hundred percent! If global copper demand was growing, it was because China was buying.

The buildings need to be lit (copper wiring), heated and cooled (aluminum ducting, zinc-galvanized steel), plumbed (copper pipes, zinc coatings), and furnished (every metal you can imagine). The workers building all this need to be fed, which means surging demand for grain, pork, coffee, sugar, and every other food commodity.

This is why Stern Hu’s arrest mattered. Iron ore was the chokepoint—the essential raw material that everything else depended on. And China had a problem: They were buying 70% of all seaborne iron ore, but they were negotiating from a position of spectacular weakness.

Why?

The Pain of Pricing Power: Why Geography Is Destiny

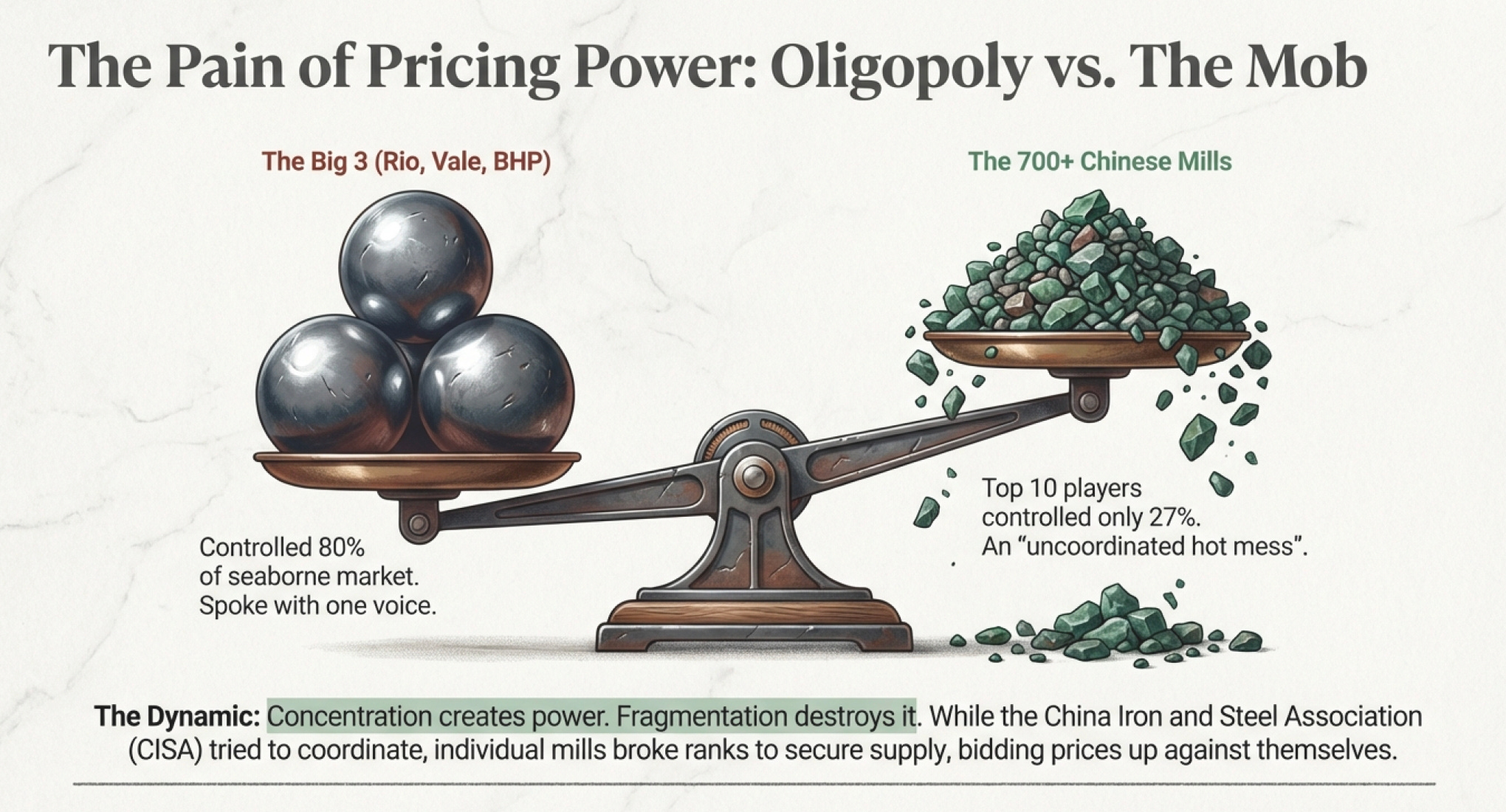

Remember our bilateral oligopoly? Three miners on one side, organized and coordinated. And on the other side... hundreds of Chinese steel mills all competing with each other to secure supply.

The miners spoke with one voice through Rio Tinto, Vale, and BHP. The Chinese mills didn’t speak at all—they screamed individually, each trying to make sure they had enough ore, even if that meant their competitor-neighbors paid less.

This is the beautiful, brutal logic of oligopoly. In copper mining, the top 10 producers control 57% of global mine supply. In iron ore, just three companies—Vale, Rio Tinto, and BHP—controlled nearly 80% of the seaborne market. But in steel production, even the top 10 players accounted for only 27% of world production.

Concentration creates power. Fragmentation destroys it.

The Chinese steel industry was—and this is not a technical term but it should be—an uncoordinated hot mess. The China Iron and Steel Association (CISA) tried to coordinate purchases, but individual mills kept breaking ranks to secure supply, bidding prices higher, and ensuring that China as a whole paid more.

This phenomenon earned its own phrase in Chinese media: “the pain of pricing power.” Whatever China bought, the price went up.

But here’s where the story gets interesting. China’s problem wasn’t just organizational. It was structural, built on barriers to entry so fundamental that no amount of organizational improvement could overcome them.

Let me explain.

The Moat That God Built Three Hundred Million Years Ago

The first and most brutal barrier in commodities is this: You either have it or you don’t.

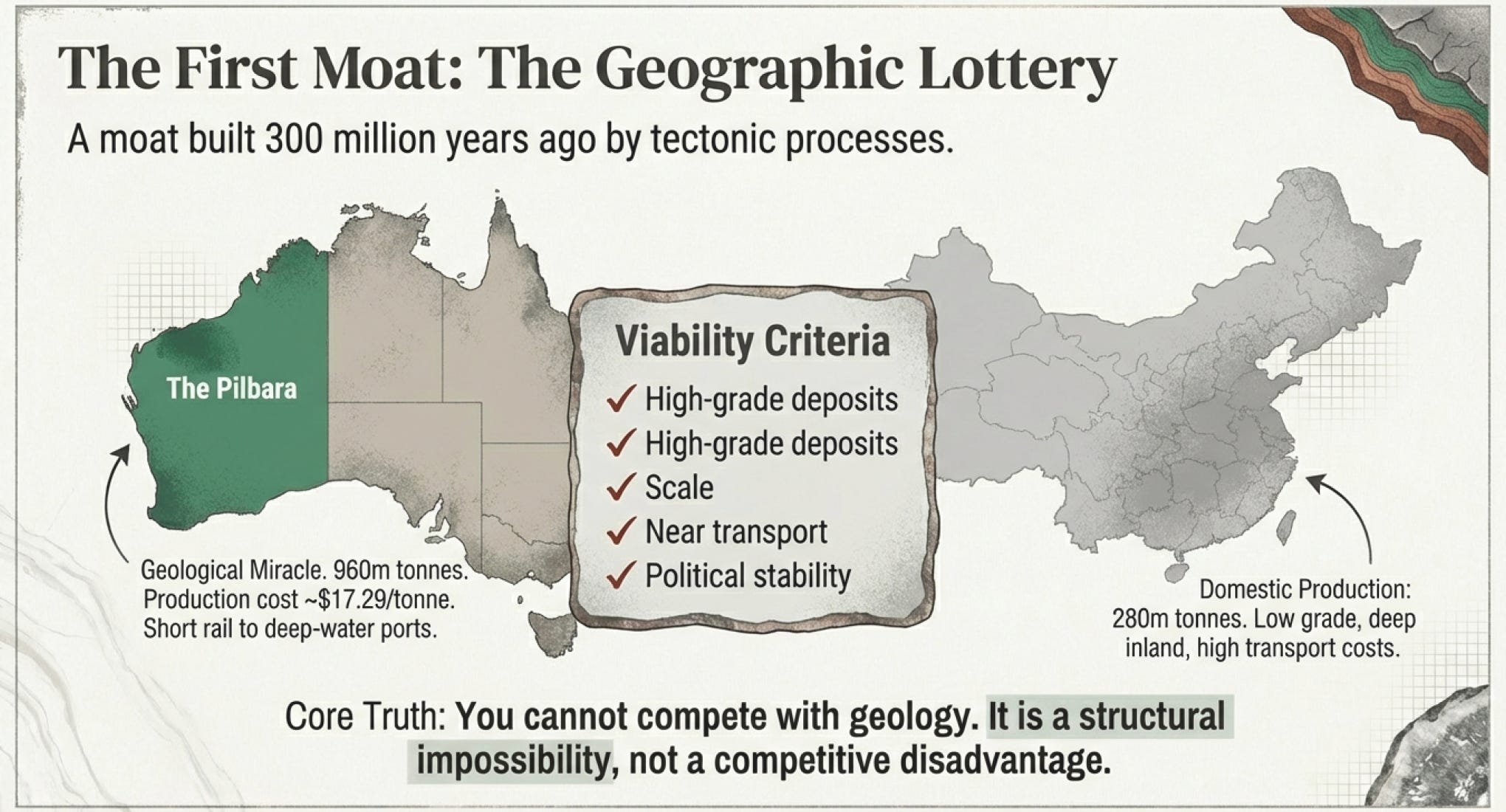

Australia produces 960 million tonnes of iron ore annually—nearly 40% of global production. Brazil produces 440 million tonnes. Together, these two countries—and specifically, the three mining giants operating there—control the majority of the world’s economically viable iron ore deposits.

Why economically viable? Because iron ore is actually quite common—it constitutes 5% of Earth’s crust. But iron ore you can profitably extract, process, and ship is vanishingly rare. You need:

High-grade deposits (the ore needs sufficient iron content to justify extraction)

Accessible deposits (not buried under mountains or oceans)

Deposits at scale (big enough to justify infrastructure investment)

Located near transportation (ports, railways, roads)

In politically stable regions (or at least regions that won’t nationalize your mine)

BHP’s Pilbara operations in Western Australia aren’t just good mines. They’re geological miracles located in a mining-friendly jurisdiction with existing rail lines to ports designed for bulk ore carriers. Rio Tinto’s deposits sit right next door. Together, they ship hundreds of millions of tons per year through Port Hedland with production costs around $17.29 per ton.

Can China compete?

China tried. By 2009, China’s domestic iron ore production was about 280 million tons annually. But Chinese deposits are lower grade, more expensive to extract, and located far inland, requiring expensive rail transport to ports. Even with 280 million tons of domestic production, China still needed to import 70% of its seaborne iron ore.

This is what I call the Geographic Lottery—a moat that was built for you 300 million years ago by tectonic processes you didn’t control, can’t replicate, and which your competitors cannot overcome no matter how smart they are or how hard they work.

You can’t compete with Australia’s iron ore if you don’t have iron ore of equivalent quality, scale, and accessibility. It’s not a competitive disadvantage. It’s a structural impossibility.

The same logic applies everywhere. The Ivory Coast supplies 37% of the world’s cocoa not because Ivorian farmers are better, but because that’s where the trees grow. South Africa supplies 76% of platinum because that’s where the platinum is. Russia provides 52% of palladium through a single company—Norilsk Nickel—because geological processes concentrated palladium deposits in Norilsk.

Saudi Arabia gets to be rich because ancient seas deposited organic material that, under pressure and time, became oil. Your backyard doesn’t.

Geography is destiny. And in 2009, China’s destiny was to be the world’s largest buyer with minimal ability to develop alternative suppliers.

Why You Can’t Just Decide to Compete

But surely, you might think, if iron ore prices were high enough, new competitors would emerge. New mines would open. Supply would increase. That’s how markets work, right?

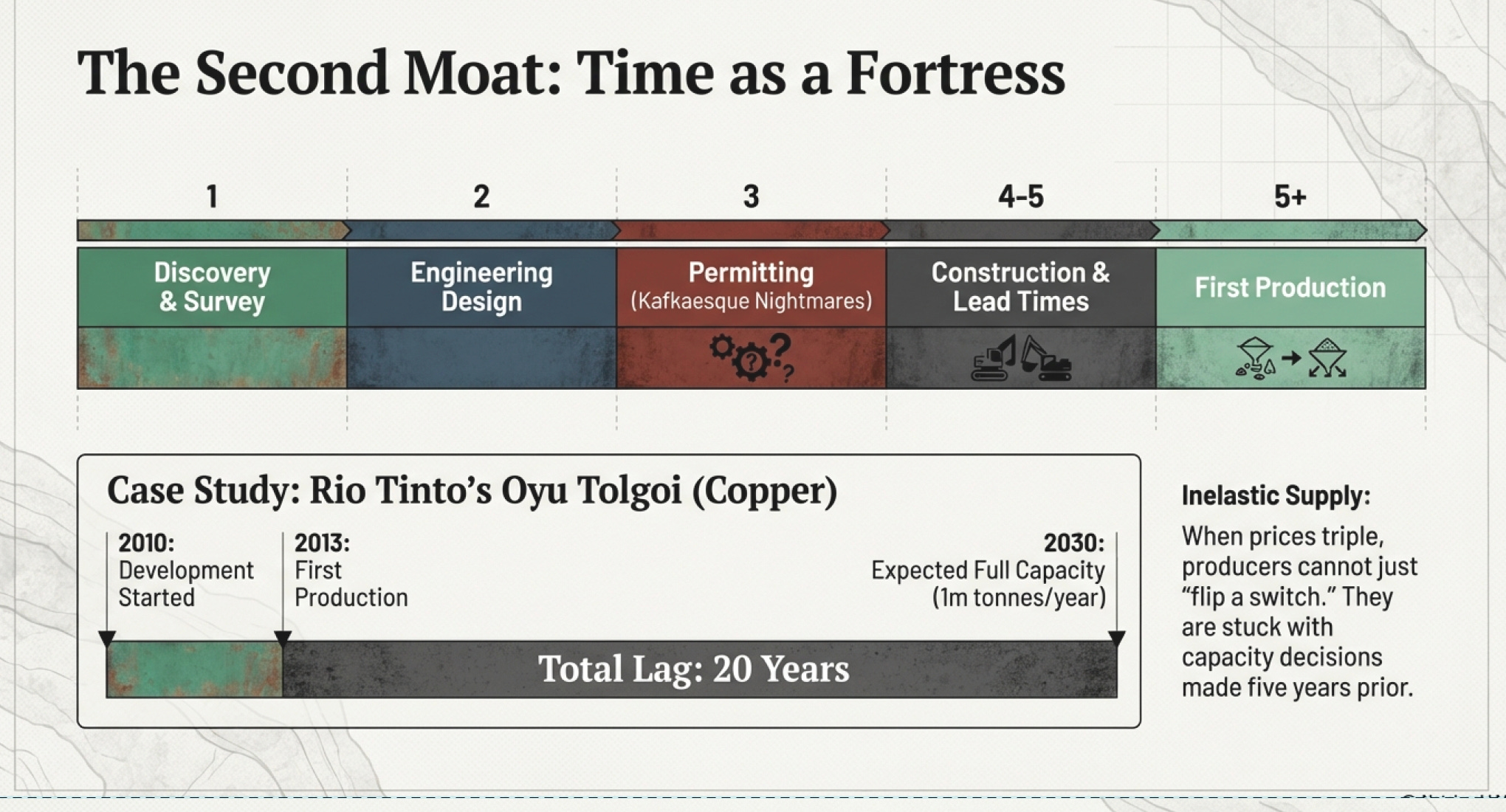

Right. Except for one tiny problem: It takes a minimum of five years to bring a new mine into production—and that’s after you’ve discovered economically viable reserves, which itself can take decades.

Let me walk you through what those five years actually mean.

Year 1: Extensive geological surveys and drilling programs to confirm the deposit’s size, grade, and characteristics. You’re not just looking for iron ore; you’re mapping out exactly where it is, how deep, what impurities exist, and whether the rock formations will cooperate with extraction.

Year 2: Engineering and design. Mines are not holes in the ground—they’re complex industrial systems. You need to design extraction methods (open pit or underground?), processing facilities (to separate ore from waste rock), power systems (mines are incredibly energy-intensive), water systems (for processing and dust suppression), and transportation infrastructure (how do you get millions of tons per year from the mine to the port?).

Year 3: Environmental studies and permitting. In Australia, this is difficult but manageable. In many other countries, it’s a Kafkaesque nightmare that can stretch for years as you navigate overlapping jurisdictions, indigenous land rights, environmental concerns, and the personal preferences of whichever officials happen to be reviewing your application.

Year 4-5: Construction. And here’s where it gets really fun. The lead times for major mining equipment are measured in years, not months. Want a massive haul truck capable of carrying 400 tons of ore? Get in line behind everyone else who decided to build a mine when prices were high. Need a ball mill for crushing ore? Hope you ordered it when prices were low because when prices are high, everybody wants one. Require a smelter? Start planning now for your grandchildren’s retirement party.

This creates what economists call “inelastic supply response”—a fancy term meaning that even when copper prices double or iron ore prices triple, producers can’t just flip a switch and double production. They’re stuck with whatever capacity decisions they made five years ago.

Rio Tinto’s Oyu Tolgoi copper mine in Mongolia started serious development in 2010. First production came in 2013. The mine is expected to reach 1 million tons of annual copper production by 2030—twenty years from start to full capacity. BHP approved $498 million for the North Rim Skarn project at Kennecott, but production won’t start until Q1 2026, with a two-year ramp-up period after that.

Now consider what this meant for the 2009 iron ore negotiations.

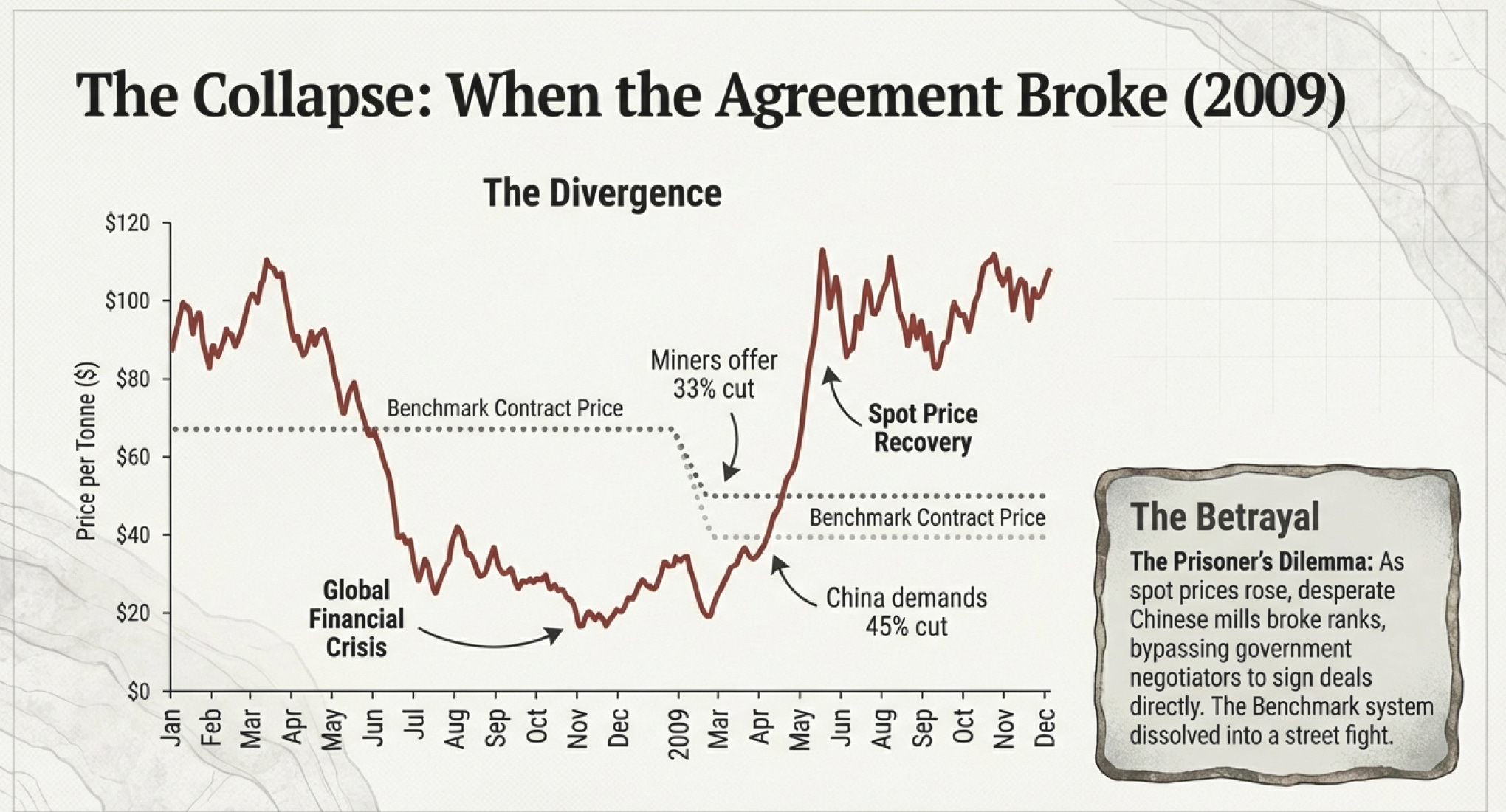

Iron ore prices had surged in 2008 as China’s infrastructure boom accelerated. But in late 2008, the global financial crisis hit. Spot prices for iron ore tumbled 70% from 2007 to 2008. Chinese steel mills, seeing the crash, demanded price cuts of 40-45% in the 2009 benchmark negotiations.

But here’s what the miners knew: The supply that would come online in 2014 was being determined by investment decisions being made in 2009. If they accepted a 45% price cut, they’d be signaling to the market—and to their own boards—that iron ore was worth 45% less. Projects would be canceled. Capital expenditures would be slashed. And when demand inevitably recovered (as it always does), there would be no new supply to meet it.

Meanwhile, spot prices were already recovering. By March 2009, spot iron ore had risen to $110 per ton—about 40% higher than a year earlier and double the 2009 contract price. The miners could see demand coming back in real time, and they were being asked to lock in low prices for the next 12 months.

So Rio Tinto, representing the sellers, offered China the same deal they’d given Japan: a 33% cut from 2008 levels.

China refused. CISA insisted on 40-45% cuts. And here’s where it got nasty.

When the Gentleman’s Agreement Became a Street Fight

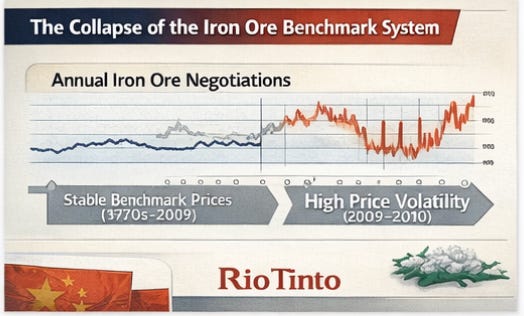

The 40-year benchmark system depended on everyone honoring the agreed price. But as negotiations dragged on through early 2009, something unprecedented happened: Chinese steel mills started breaking ranks.

Individual mills, desperate to secure supply, began signing contracts directly with the miners at the 33% cut that Japan had accepted. They were defecting from CISA’s coordinated strategy because they valued guaranteed supply over collective bargaining power.

Meanwhile, the spot market exploded. In 2008, spot sales accounted for about 30% of iron ore trades in China. By 2009, spot sales had jumped to 60%. And those spot prices were running 40% higher than the proposed contract prices.

This created a vicious dynamic: Chinese mills that honored CISA’s position and refused the 33% cut were forced to buy on the spot market at higher prices. Mills that defected got cheaper ore. The incentive to defect became overwhelming.

And there’s more. India, sensing opportunity, began selling more iron ore on the spot market. Indian ore was lower quality than Australian ore, but it was commanding higher prices than the benchmark because buyers were desperate. This encouraged the big three miners—Rio, BHP, and Vale—to sell more iron ore on the spot market too, further undermining the benchmark system.

BHP’s CEO Marius Kloppers began openly calling for a shift away from annual benchmarks to quarterly contracts based on spot prices. In July 2009, BHP announced it would sell 30% of its ore through spot market and quarterly contracts, breaking with 40 years of tradition.

From China’s perspective, this was the worst of all worlds:

They were paying higher prices than they’d paid in 2008

Their mills were competing against each other, driving prices up

The benchmark system was collapsing

The miners were capturing the upside of the spot market while China bore the risk

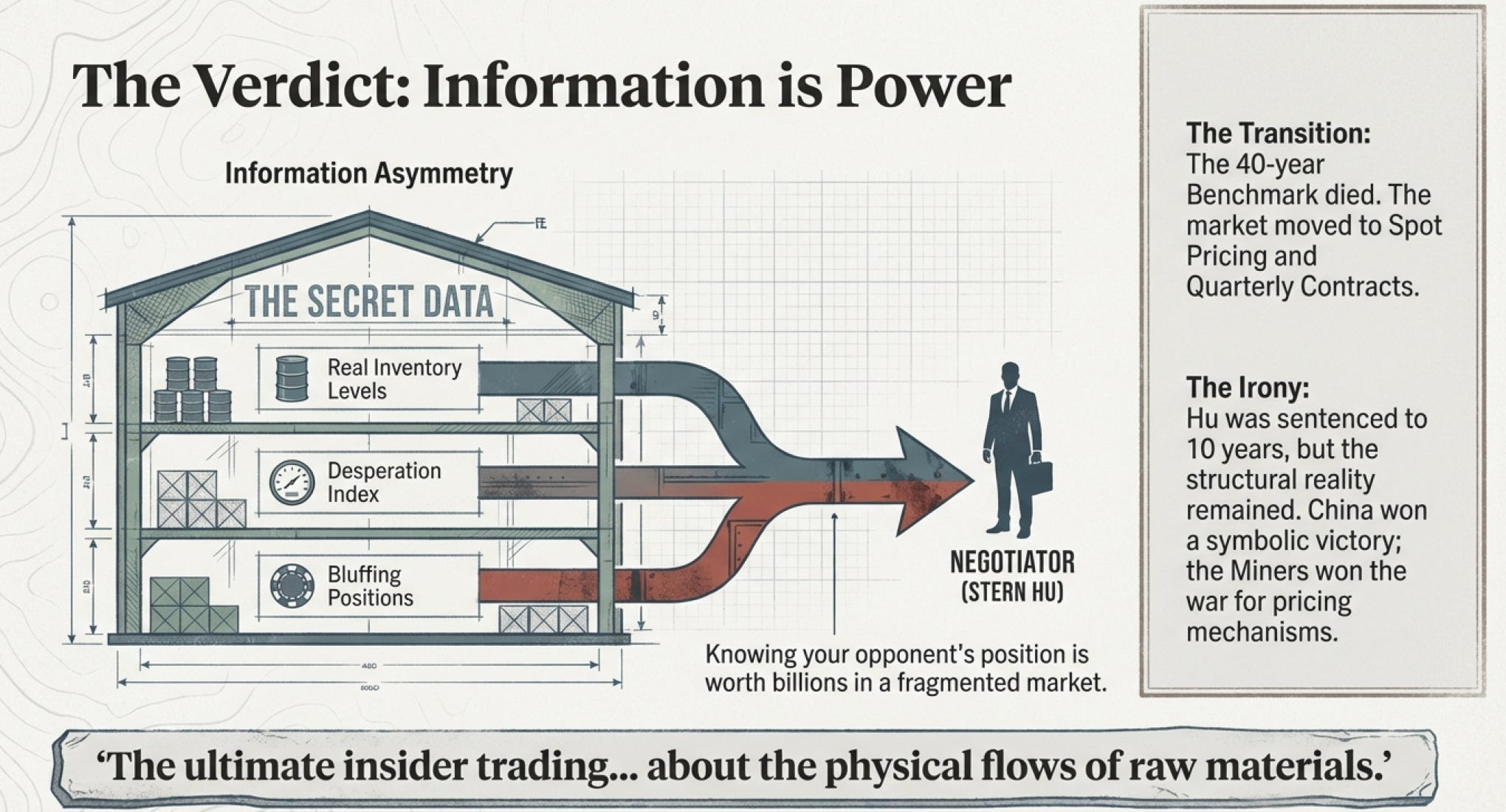

Stern Hu, as Rio Tinto’s lead negotiator, was in the middle of all this. And according to Chinese authorities, he had something very interesting on his laptop: detailed information about Chinese steel mills’ production levels, inventory, and negotiating positions.

How detailed? According to accusations, “too detailed to have been obtained legally.”

Why Information Is Absolute Power When You’re an Oligopoly

Think about what that information meant.

If you’re negotiating as one of three sellers against hundreds of buyers, knowing each buyer’s true position is worth billions. You know:

Which mills are desperate for supply and will pay premium prices

Which mills have inventory and can wait for better prices

Which mills are bluffing about alternative suppliers

How much ore is sitting in Chinese warehouses, signaling true demand

Which mills are financially stressed and might be willing to pay more to avoid production shutdowns

This is the ultimate insider trading—except it’s not about stocks, it’s about the physical flows of raw materials that constitute the foundation of industrial civilization.

The accusation was that Hu had obtained this information through bribery. Chinese prosecutors claimed he’d paid executives from 16 different Chinese steel mills for industry data. The data was allegedly found on Hu’s laptop, along with detailed information about production and sales plans from “several dozen major business partners.”

Here’s where it gets fascinating. During the trial, Hu admitted to accepting bribes but disputed the amounts. But notice the charge was accepting bribes, not paying them. Under Chinese law, bribery requires both a payer and a receiver. So if Hu was guilty of accepting bribes, someone must have been guilty of paying them.

Yet no Chinese executives were prosecuted until much later, and then only quietly. As one legal scholar asked during the trial: “Where is the prosecution against the bribers?”

The answer, of course, was political. The arrests happened just weeks after Rio Tinto walked away from Chinalco’s $19.5 billion investment. They happened during the most contentious iron ore negotiations in history. And they happened when China’s government was desperate to restore order to an iron ore market where hundreds of mills were competing against each other and driving prices higher.

Stern Hu became, in the words of one analyst, a “sacrificial lamb for China’s national security and the opaqueness of the relationship between the market and the state.”

But here’s what the case actually revealed: The value of information in commodity markets is so high that governments treat it as espionage.

The Aftermath

By 2010, the 40-year benchmark system was dead.

The miners had won the right to move to quarterly pricing based on spot markets. China had won nothing except the symbolic punishment of one negotiator. And both sides were worse off than they’d been under the old system.

Quarterly pricing based on spot markets meant prices became much more volatile. Steel mills faced unpredictable input costs, making it harder to price long-term contracts with customers. Miners faced unpredictable revenues, making it harder to justify long-term capital investments. And speculators entered the market through iron ore futures contracts, adding financial trading on top of physical trading.

In 2022, China tried again to consolidate bargaining power by creating the China Mineral Resources Group (CMRG)—a state-run buyer designed to coordinate purchases and negotiate as a single entity. In September 2025, Bloomberg reported that CMRG instructed Chinese mills to stop buying BHP products priced in U.S. dollars after negotiations broke down over pricing and discounts on medium-grade ore.

Sound familiar?

The same pattern: China tries to coordinate buyers. Mills break ranks when they need supply. Miners use information and negotiating leverage. Relationships deteriorate. Someone gets mad. Someone gets sanctioned. And the fundamental structure—three miners controlling 70% of supply, facing hundreds of mills who won’t cooperate—remains unchanged.

Because the structure isn’t about who’s negotiating. It’s about geology, time, and the brutal logic of oligopoly.

What Stern Hu’s Laptop Revealed About Every Commodity Market

Let’s zoom out from iron ore and look at what this story reveals about commodity markets generally.

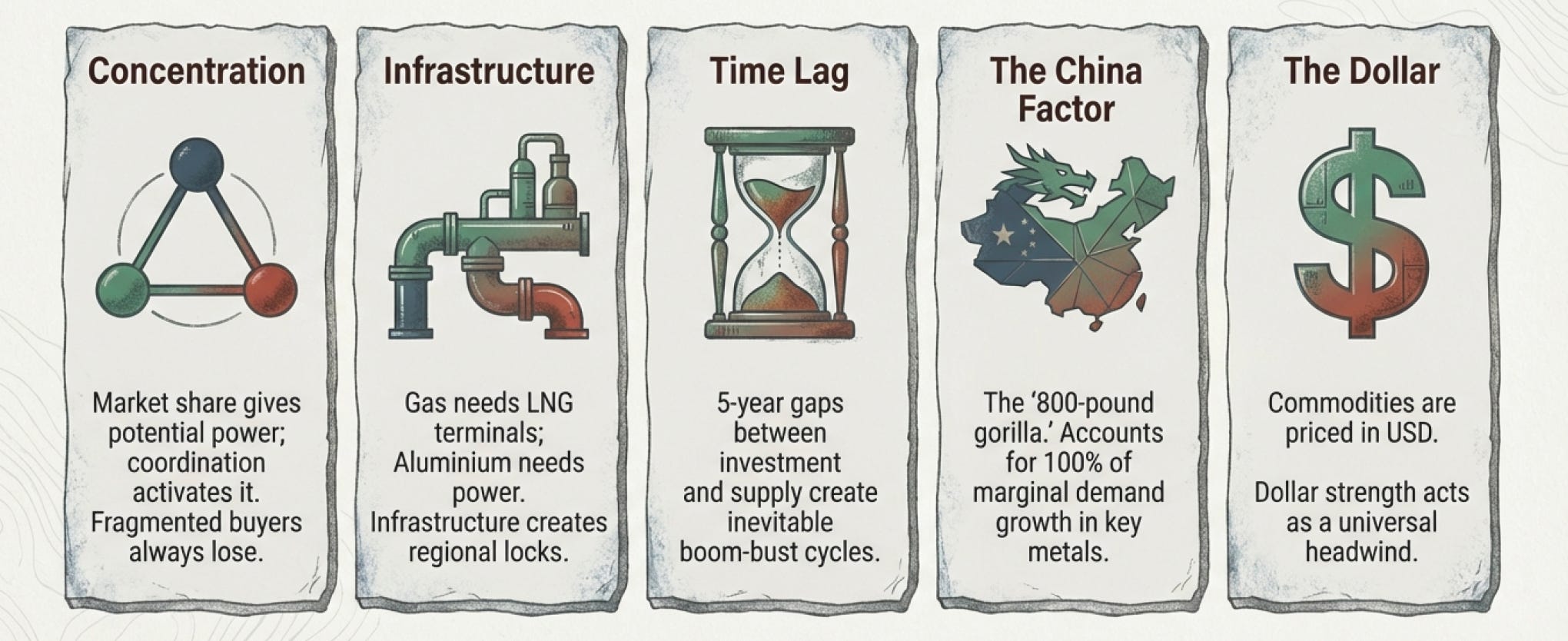

First: Supply concentration creates pricing power, but only if suppliers coordinate.

In copper, the top 10 producers control 57% of global supply. In palladium, Norilsk Nickel alone produces 45% of world output. In cocoa, the Ivory Coast and Ghana combine for 57% of global production. In iron ore, three companies control 70-80% of seaborne supply.

But concentration alone isn’t enough. Chinese steel production is massive—more than all of North America and Europe combined. But with 700+ mills and 7,000 companies forming steel, China’s fragmentation destroys its bargaining power. The top three Chinese steel producers account for only 20% of total output. Compare that to South Korea, where two mills account for 87% of production.

The lesson: Concentration creates the potential for pricing power. Coordination activates that potential.

Second: Essential infrastructure creates sustainable moats.

Natural gas must be supercooled to -162°C, compressed to one six-hundredth its original volume, turned into LNG, and shipped on double-hulled vessels designed specifically for this purpose. Then receiving terminals must convert it back to gas for pipeline distribution.

This infrastructure is so specific, so capital-intensive, and so long-lived that it creates regional markets. The price of natural gas in Japan has limited impact on U.S. prices because the gas physically cannot move easily between markets. Oil, by contrast, is a global commodity because it’s relatively easy to ship and can be used in many markets.

Aluminum smelters require massive amounts of electricity—so much that the location of cheap power matters more than proximity to bauxite deposits. You’ll find smelters in Iceland (geothermal), Norway (hydro), and the Middle East (cheap natural gas), all far from major aluminum ore deposits. The infrastructure locks in competitive advantages that can last decades.

Third: Time is the most durable moat.

When copper prices rallied in 2024-2025, everyone could see massive demand coming from EVs (83 kg of copper per vehicle), data centers, and renewable energy. But supply couldn’t respond. Rio Tinto’s Oyu Tolgoi is ramping up, expecting to reach 1 million tons annually by 2030—but the project started in 2010. BHP’s projects won’t hit full capacity until the late 2020s.

This is why lithium producers saw such dramatic swings. Prices hit $70,000/ton in 2022, crashed to below $9,550/ton by February 2025, then rebounded 57% to $13,003/ton by November 2025. The boom prompted massive investment in new supply. But that supply all came online in 2023-2024, creating a glut. Now, with a third of global production unprofitable at low prices, supply growth has stopped. Forecasters predict deficits emerging in 2026.

The five-year lag between investment decision and production means markets constantly overshoot in both directions. And the companies that survive the busts—who can operate at high costs but have dormant capacity—become the biggest winners in the booms.

Fourth: Weather, China, politics, and the dollar.

Natural gas prices are 50-80% determined by weather—heating in winter, cooling in summer. Wheat depends on rainfall in both hemispheres. Coffee depends on Brazilian weather. These are risks you cannot hedge away.

China is the 800-pound gorilla in every commodity market. They consumed 100% of marginal copper demand growth in 2007. They import 75% of seaborne iron ore. They produce more steel than the next seven countries combined. When China’s property sector weakens (as in 2025), iron ore prices collapse. When China builds out EV infrastructure, lithium soars.

Politics determines whether you can extract resources at all. Zimbabwe’s 2009 seizure of 51% of foreign mining stakes without compensation destroyed investor confidence overnight. Saudi Arabia and Mexico have excluded foreign companies from oil for over 50 years. Russia’s resource wealth comes with political risk that’s impossible to quantify.

And the dollar—since most commodities are priced in dollars, dollar strength creates headwinds for all commodity prices simultaneously. This creates feedback loops with inflation that amplify both booms and busts.

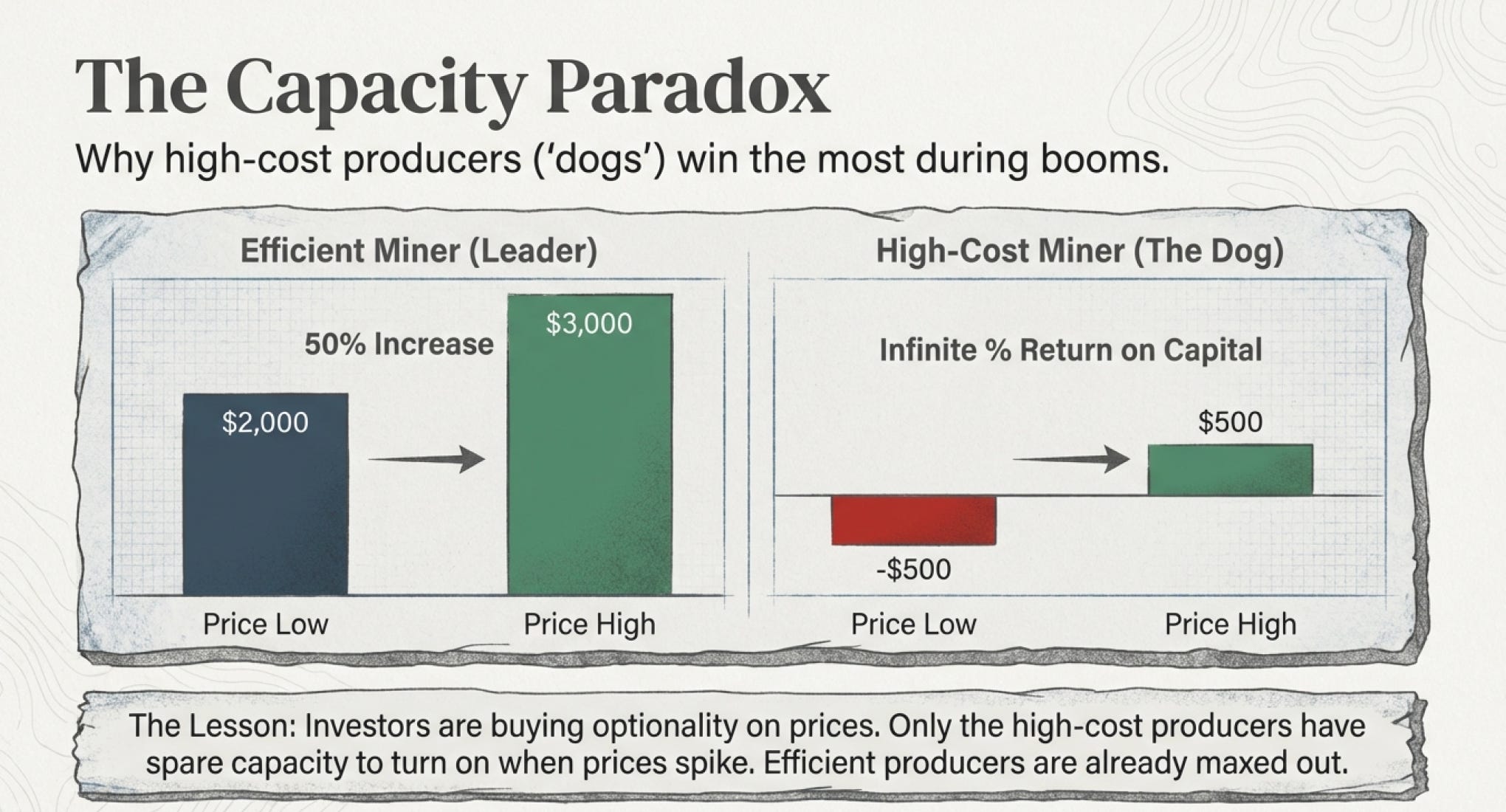

Fifth: The capacity paradox.

The most counterintuitive lesson: When commodity prices surge, the biggest winners are often the highest-cost producers—the ones who were losing money before the surge. Yes you heard right - at least in the stock market.

Why? Because the efficient producer goes from making $2,000/ton in profit to making $3,000/ton. That’s a 50% increase—nice. But the high-cost producer goes from losing money to making $2,500/ton on incremental production—infinitely better returns, mathematically speaking (in terms of %).

This is why the “dogs” of commodity sectors often outperform during booms. They have dormant capacity that becomes wildly profitable when prices spike. The efficient producers are already maxed out.

“If a company has maxed out their capacity, during a bull market they have little upside. But companies that haven’t maxed out capacity—which usually have lower margins or losses—have huge upside.”

You’re not buying current earnings in commodity stocks. You’re buying optionality on prices, with the strike price set at the company’s marginal cost of production.

Same Story, Different Chapter

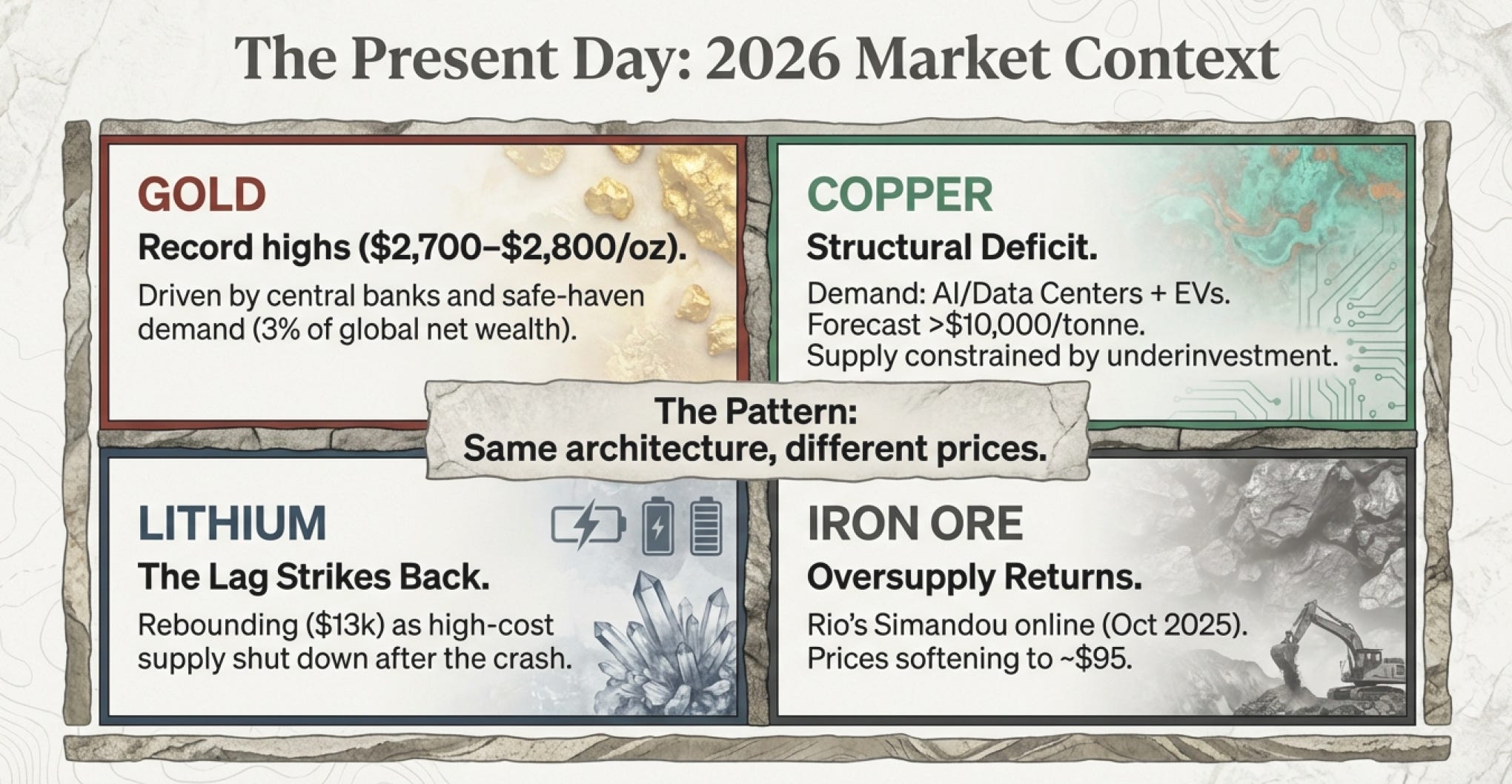

As I write this in early January 2026, the patterns revealed by Stern Hu’s arrest continue playing out.

Gold just hit records near $2,700-2,800/oz, driven by central bank buying and safe-haven demand. Silver rose 34% in 2025. These aren’t speculative bubbles—they’re responses to structural concerns about fiat currencies and geopolitical instability. Household gold holdings have reached more than 3% of net wealth, the highest in over 50 years.

Copper hovers around elevated levels despite coming off May 2024 highs. Deutsche Bank forecasts it could exceed $10,000/ton by end of 2026 as the market moves into structural deficit. The reason? Those five-year lags. Underinvestment in 2019-2021 means insufficient new supply in 2024-2026, just as AI data centers, EV adoption, and grid modernization accelerate copper demand.

Iron ore faces oversupply from new projects finally coming online—including Rio Tinto’s Simandou project in Guinea that began first ore loading in October 2025. Goldman Sachs forecasts prices declining to $95/ton in 2025. BHP’s iron ore contribution to earnings has shrunk to 53% versus copper’s 45%—a dramatic pivot for a company that built its fortune on Pilbara iron ore.

Oil markets show a persistent glut, with IEA forecasting demand growth under 1 million barrels/day in 2025. Yet geopolitical tensions create constant upside risk—sanctions, conflicts, OPEC+ decisions can flip sentiment overnight.

And lithium? After crashing from $70,000/ton to below $10,000/ton, it’s rallied 57% since June 2025. Not because demand exploded, but because supply contracted as high-cost producers shut down. The five-year lag strikes again.

Each of these stories is unique. But each reveals the same underlying architecture: Supply determined by geological accident and five-year lead times. Demand determined by economic growth, technology shifts, and China. Prices determined by the interaction between inelastic supply and volatile demand. And profits captured by whoever controls the irreplaceable assets with the lowest costs and longest reserve lives.

The Lesson

The commodity business is not about forecasting prices. It’s about understanding structure.

When you grasp that BHP’s iron ore advantage comes from a deposit formed by geological processes millions of years ago, that cannot be replicated, and that takes 10-20 years to develop into a producing mine, you stop worrying about quarterly earnings. You start thinking about whether this asset has fundamental scarcity value over decades.

When you understand that aluminum smelters must be located near cheap power sources, you realize Iceland’s geothermal advantages and the Middle East’s cheap natural gas create durable competitive positions that don’t disappear because of a recession.

When you see that five-year lead times mean today’s supply was determined by 2020’s investment decisions, and 2030’s supply is being determined right now, you realize the game is about reading investment signals, not spot prices.

When you recognize that China accounts for 100% of marginal demand growth in copper, you stop trying to predict copper prices from U.S. housing starts and start watching Chinese infrastructure spending, EV adoption, and renewable energy buildouts.

The moats in commodity businesses are different from those in consumer brands or software companies. They’re not about switching costs or network effects. They’re about geology, time, infrastructure, and the brutal physics of digging things out of the ground and turning them into usable materials.

But they’re just as real. Perhaps more so.

You can disrupt a software business with better code. You cannot disrupt BHP’s iron ore franchise by being smarter or working harder. The ore is where it is, and getting it out requires exactly the infrastructure, expertise, and time that BHP has spent decades developing.

This is why Stern Hu’s laptop mattered. The information on it—about production, inventories, negotiating positions—was worth billions because it revealed the internal dynamics of a market where three sellers face hundreds of buyers. In a concentrated market, information is power. In a fragmented market, information is survival.

The arrest, the trial, the 10-year prison sentence—these weren’t just about punishing one negotiator for alleged bribery. They were about China attempting to impose order on a market structure that economics had already determined.

China wanted pricing power. But pricing power flows from market structure, not from desire. Three miners controlling 70% of supply will always have more power than 700 mills controlling 30% of demand, no matter how many times you arrest the negotiators.

The hole in the ground, it turns out, is also a moat.

And some moats were dug 300 million years ago by forces beyond human control.

Epilogue: The Man Who Knew Too Much

Stern Hu was released from prison in July 2018 after serving eight years of his ten-year sentence. He returned to Australia, where he lives quietly, rarely speaking publicly about his experience.

Rio Tinto signed a deal with Chinalco just before Hu’s trial—a $1.5 billion agreement to develop the Simandou iron ore project in Guinea. The irony was not lost on observers: The company that China accused of causing $100 billion in damages was now partnering with the state-owned company whose rejected investment had precipitated the crisis.

The benchmark pricing system never recovered. Today, iron ore trades on spot markets and through quarterly contracts, with prices swinging wildly based on Chinese demand signals and supply disruptions. Steel mills face unpredictable costs. Miners face unpredictable revenues. And financial speculators have inserted themselves into what was once a straightforward trade between industrial producers and consumers.

In December 2025, Rio Tinto announced a $2.5 billion investment to expand the Rincon lithium project in Argentina. First production is expected in 2028, with full capacity around 2031. That’s six years from decision to full production.

The commodity business: Capital-intensive. Time-intensive. Unforgiving of mistakes. But for those who understand the moats—who can identify the irreplaceable assets, the time fortresses, the engineering advantages, and the capacity paradoxes—the rewards can be extraordinary.

Because when you’ve spent five years building something that took nature 300 million years to create, in a location where competitors cannot follow, using infrastructure they cannot replicate, serving demand they cannot ignore, you don’t just have a business.

You have a fortress.

And Stern Hu’s laptop, for all the secrets it supposedly contained, revealed the most important secret of all:

In commodity markets, the strongest fortresses are the ones built by geology, time, and the fundamental physics of supply that no amount of information, coordination, or negotiating skill can overcome.