🌱 A Basic Agritech Primer

The Greatest Casino Nobody’s Watching: How Four Companies Rigged the Game of Food

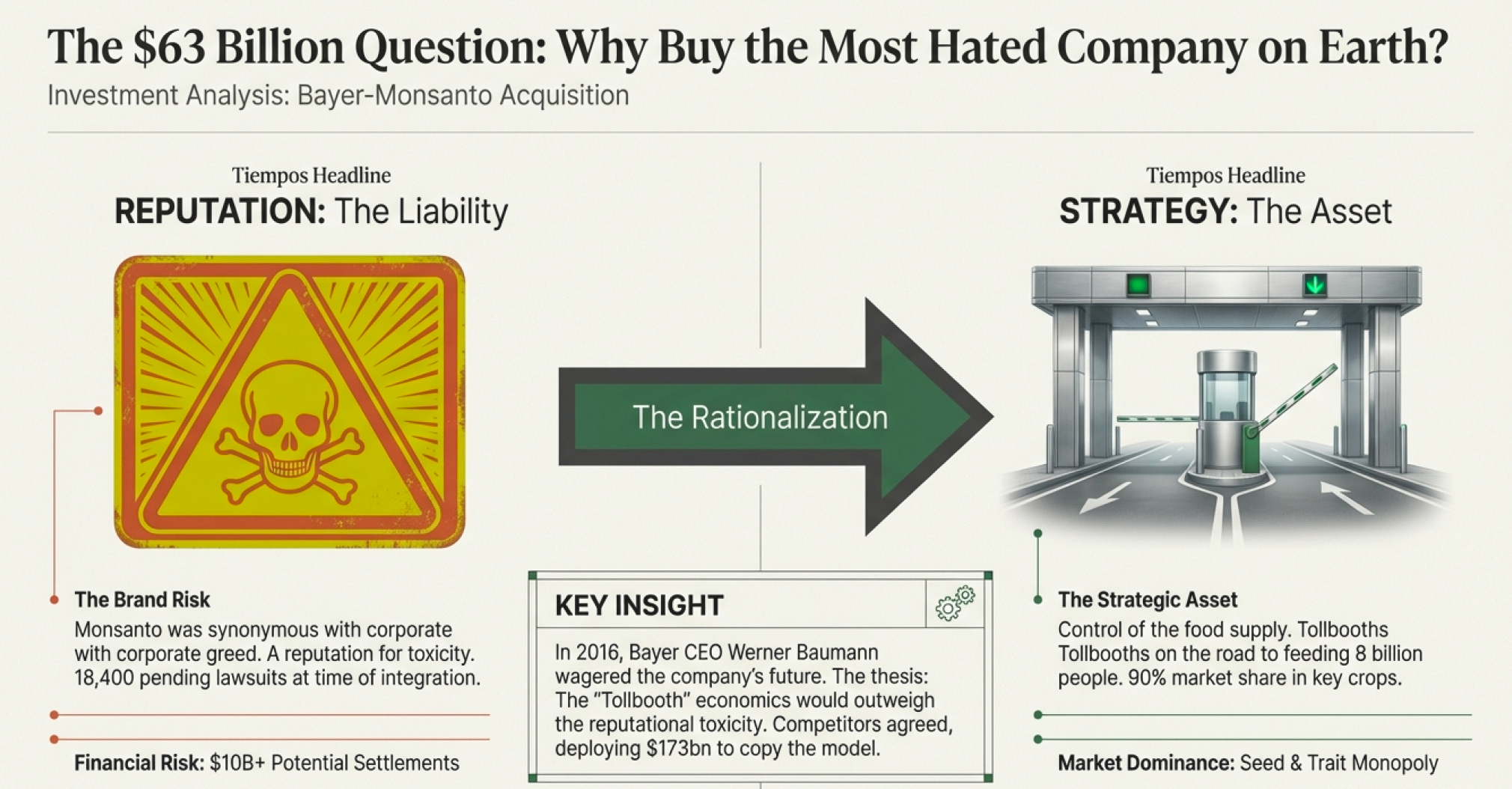

The $63 Billion Question Nobody Asked

Here’s a thought experiment: You’re Werner Baumann, CEO of Bayer, sitting in a Leverkusen boardroom in 2016. Your company makes aspirin and blood thinners. Someone slides you a proposal to buy Monsanto for $63 billion—the largest all-cash acquisition in human history. The company you’re buying is so hated that “Monsanto” has become a verb meaning “to destroy with corporate greed.”

What would you do?

If you said “run away screaming,” congratulations—you have more sense than Bayer’s board. They said yes. And what happened next is one of the most spectacular business disasters in modern capitalism, teaching us more about industry moats, barriers to entry, and business economics than any textbook ever could.

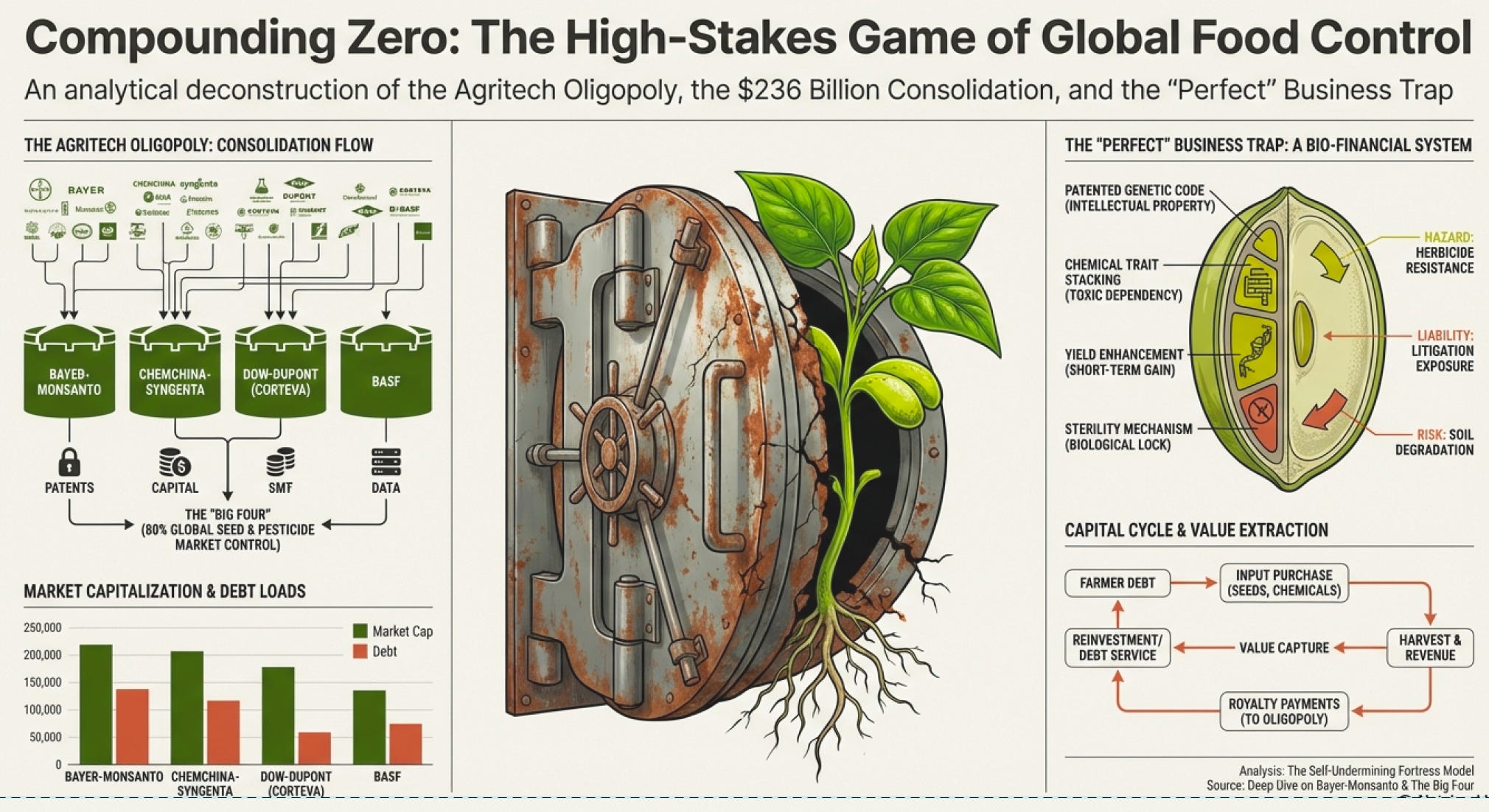

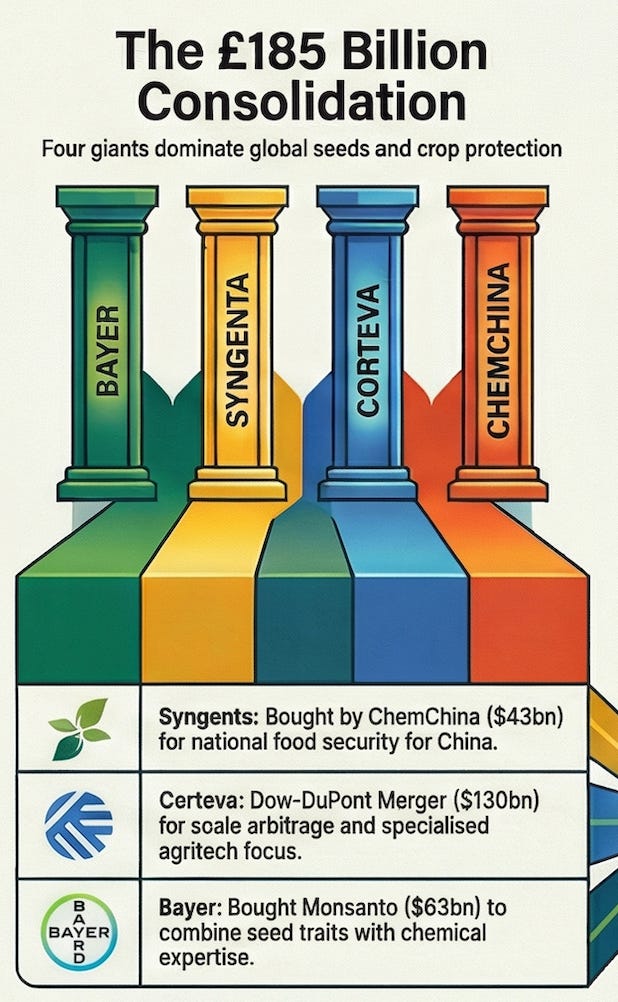

But here’s the twist that makes this story interesting: Monsanto wasn’t worthless. The business model was brilliant. So brilliant that even as Bayer hemorrhaged billions in lawsuits, three other companies were simultaneously spending $130 billion (Dow+DuPont) and $43 billion (ChemChina+Syngenta) to build the exact same type of business.

Why would rational executives throw $236 billion at an industry everyone claims to hate? Because they understood something that doesn’t show up in any financial statement: they were buying the tollbooths on the only roads to feed eight billion people.

Let me show you how those tollbooths work.

The Weed Problem, or: How to Make $10 Billion Selling Poison and Antidote

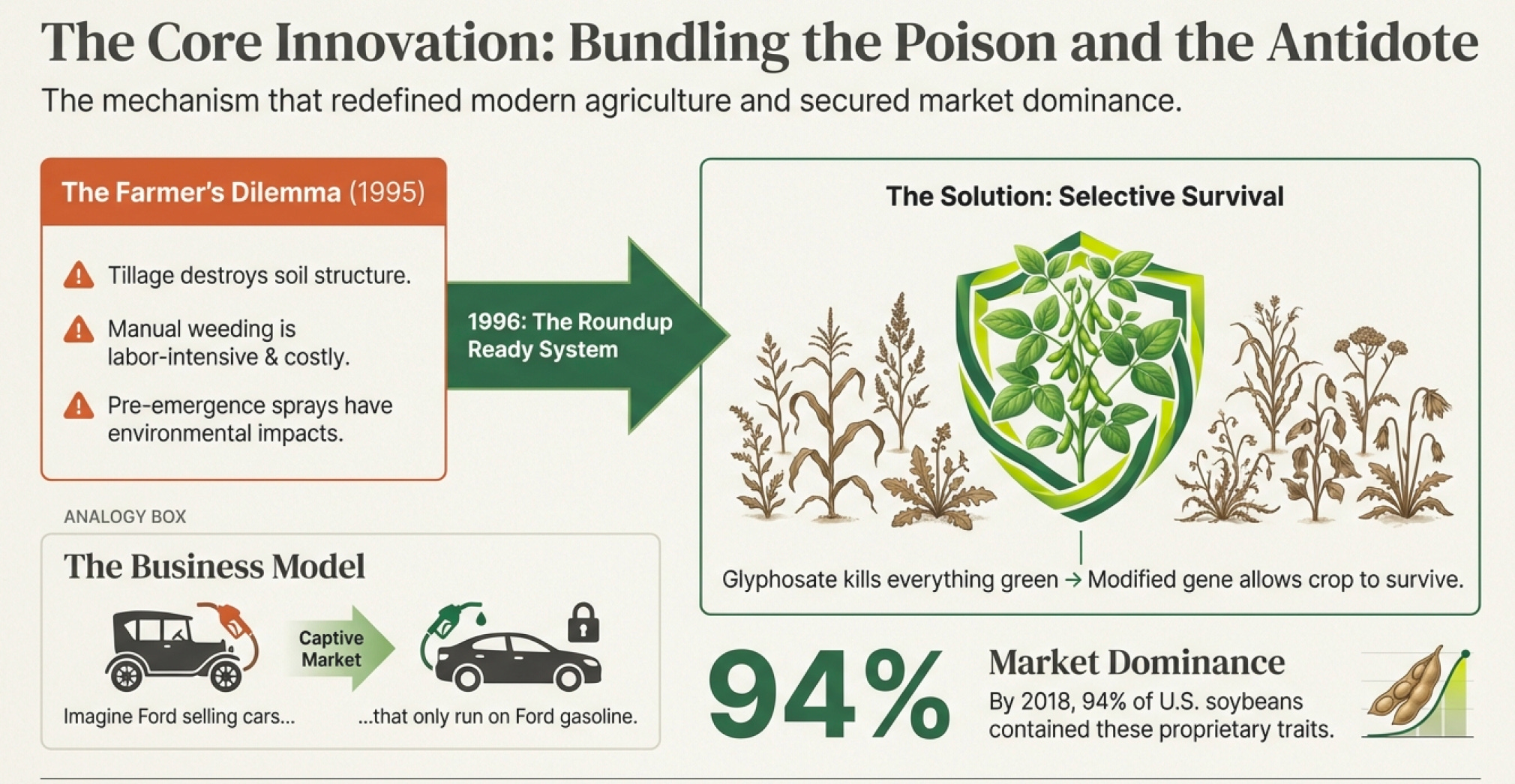

Picture Iowa, 1995. You’re a corn farmer with 1,000 acres. Weeds are your enemy. They steal water, nutrients, and sunlight from your corn. They can cut your yield by 50% if you don’t control them.

Your options all suck:

Tillage: Plow the field to bury weeds. Destroys soil structure, causes erosion, burns diesel fuel, takes time.

Pre-emergence herbicides: Spray before planting. Toxic stuff that lingers in groundwater. Doesn’t work on weeds that emerge later.

Manual weeding: Are you kidding? You have 1,000 acres.

This is the problem farmers faced for 10,000 years. Monsanto’s chemist John Franz found something amazing in 1970: glyphosate, which killed plants by blocking a specific enzyme (EPSP synthase) they need to make proteins. It was like finding the “off switch” for photosynthesis.

By 1974, Monsanto was selling it as Roundup. Perfect herbicide. One problem: it killed everything green, including your crops.

Here’s where the business model gets beautiful—or diabolical, depending on your perspective.

In 1996, Monsanto introduced Roundup Ready soybeans. Genetically modified to resist glyphosate. Now you could spray your entire field during the growing season. The weeds die. Your soybeans laugh at the poison and keep growing.

Think about what Monsanto just created from a business perspective:

Poison Pill #1: Intellectual Property as a Moat

They patented the gene. Not just the process of inserting it, but the gene itself in the plant. Every seed carrying that gene pays tribute to Monsanto. By 2018, 94% of U.S. soybeans, 91% of cotton, and 90% of corn contained Monsanto’s traits.

That’s not market share—that’s dominance. But it’s better than dominance. It’s a system.

Poison Pill #2: The Bundled Monopoly

The glyphosate patent expired in 2000. Anyone could make generic Roundup. But here’s the trick: glyphosate only works because the seeds resist it. The monopoly moved upstream. You need both products. Monsanto sold both products.

Imagine if Ford sold both cars and gasoline, and their cars only ran on Ford gasoline. That’s the Roundup Ready system.

Poison Pill #3: The Technology Agreement

When you bought Monsanto seeds, you didn’t actually buy them. You licensed them. You signed an agreement promising not to save seeds for replanting. You agreed to let Monsanto inspect your fields. You agreed to arbitrate disputes in venues favorable to Monsanto.

Why did farmers agree? Because the alternative was going back to 1995’s terrible weed control options. The seeds delivered 5-10% better yields. The convenience was undeniable. The math worked—even at premium prices.

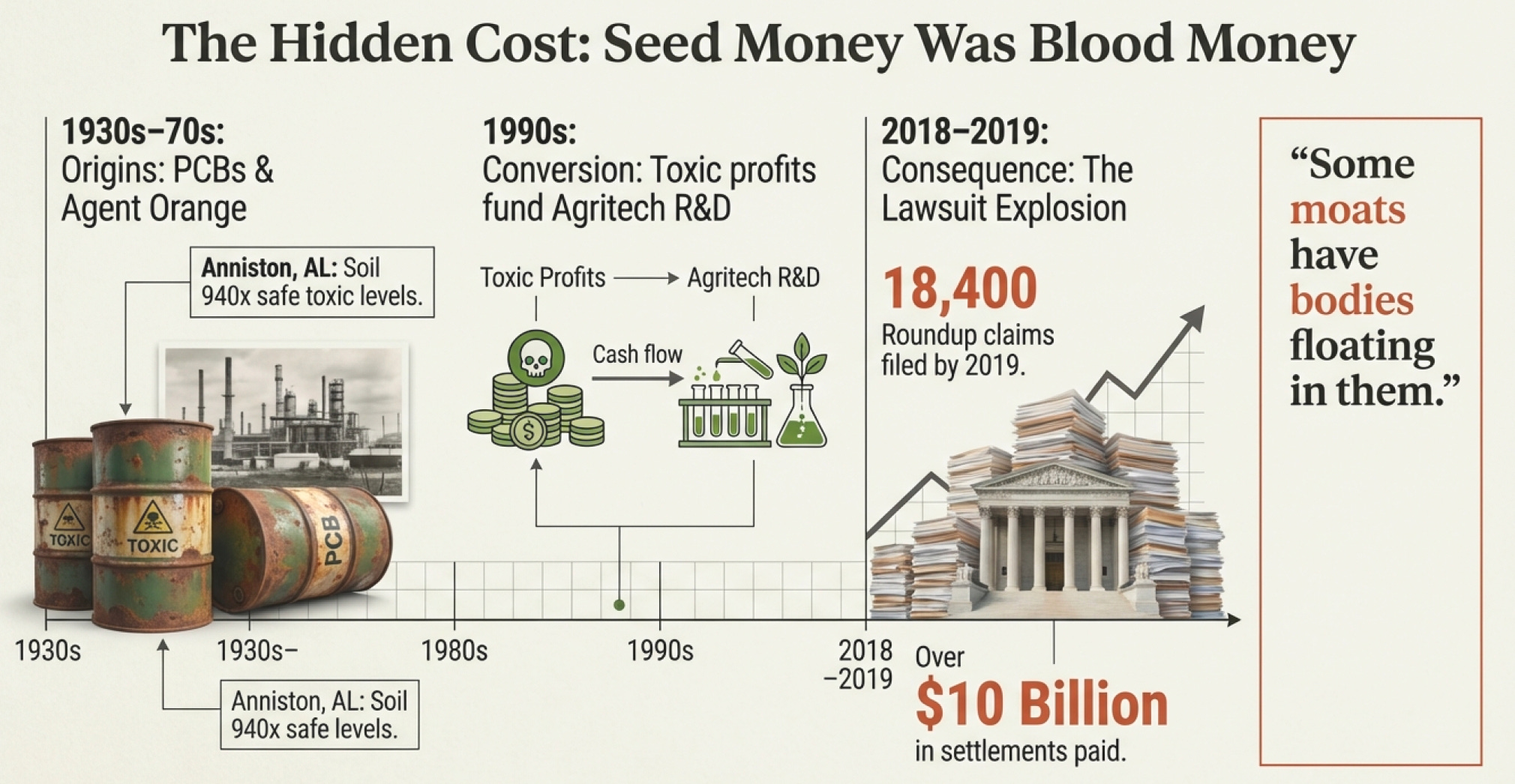

The Seed Money Was Blood Money

Now, here’s the uncomfortable question: Where did Monsanto get the billions needed to develop this genetic engineering technology?

The answer makes the story darker and explains why Bayer inherited a lawsuit bomb: PCBs and Agent Orange.

From the 1930s through 1977, Monsanto manufactured polychlorinated biphenyls (PCBs)—industrial coolants used in electrical transformers. They were perfect for the job: stable, fire-resistant, effective.

They were also toxic. They cause cancer. They cause developmental problems. They accumulate in human tissue and persist for decades.

Monsanto knew. Internal documents from the 1930s show executives understood PCB toxicity. They made them anyway.

In Anniston, Alabama, Monsanto’s plant contaminated everything. Soil tested at 940 times the safe level. The creek was declared “hazardous waste.” Residents were warned not to eat fish from local waters. Factory workers literally peeled off layers of their own skin but kept working because Monsanto offered cash bonuses.

The profits were extraordinary. They funded Monsanto’s expansion into agricultural chemicals.

Then came Agent Orange—the herbicide-defoliant the U.S. military sprayed over Vietnam. The dioxin contamination has caused birth defects spanning multiple generations. Monsanto was a major manufacturer.

Those toxic profits were “seed money” that funded the agricultural empire. When you’re studying business moats, remember this—sometimes the fortress was built with blood money, and those liabilities never fully disappear.

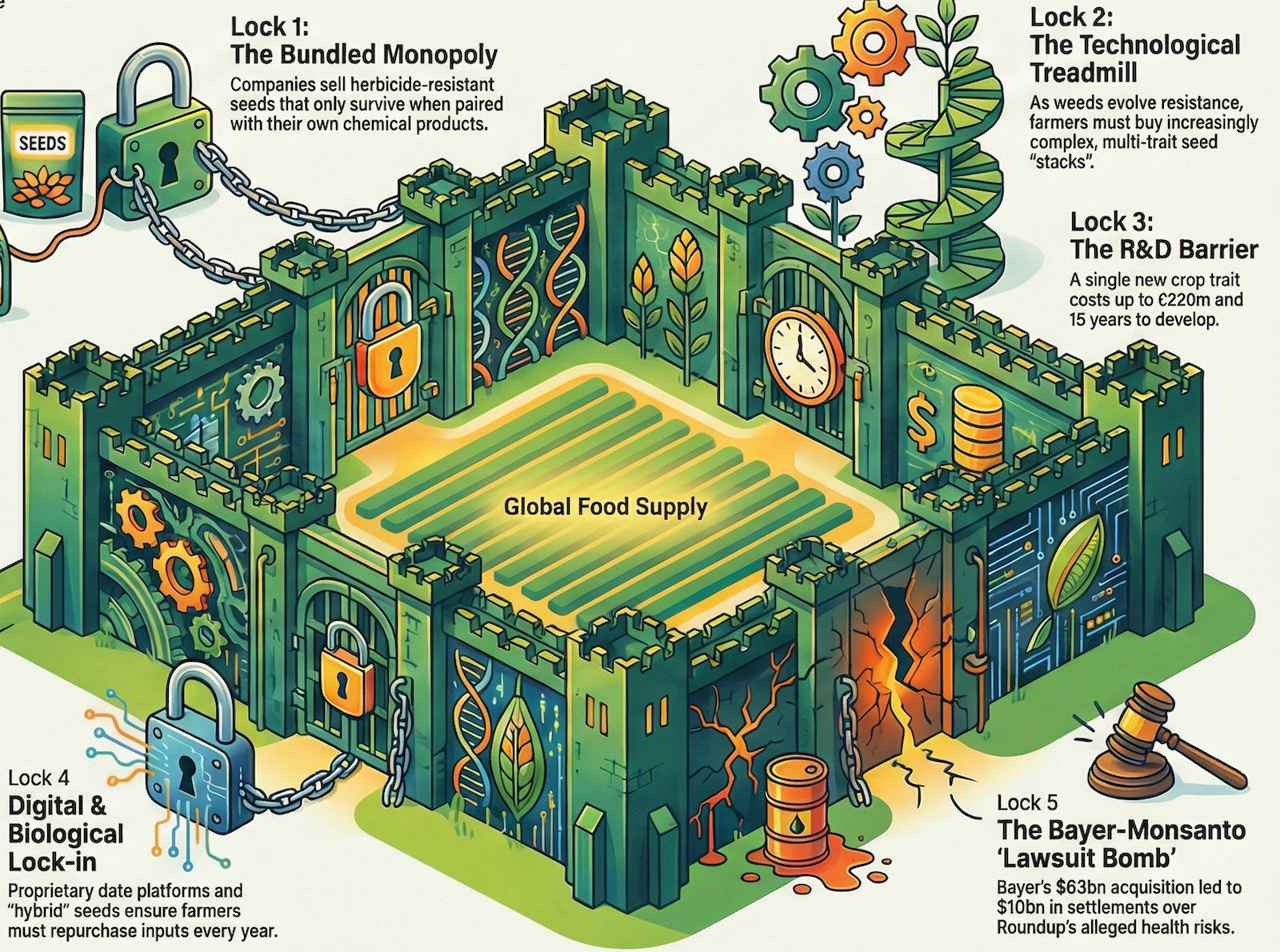

When Bayer bought Monsanto in 2018, they thought they were buying the tollbooths. What they also bought were the lawsuits. By mid-2019, they faced 18,400 Roundup cancer claims. They’ve paid over $10 billion settling them.

The market cap of Bayer fell by half. The entire value of Bayer’s pre-Monsanto business evaporated. It’s taught in business schools now as one of history’s worst M&A deals.

The lesson: A great business model with a toxic liability overhang is still toxic. Some moats have bodies floating in them.

The Four Horsemen of Agriculture, or: How to Control Food Without Owning Farms

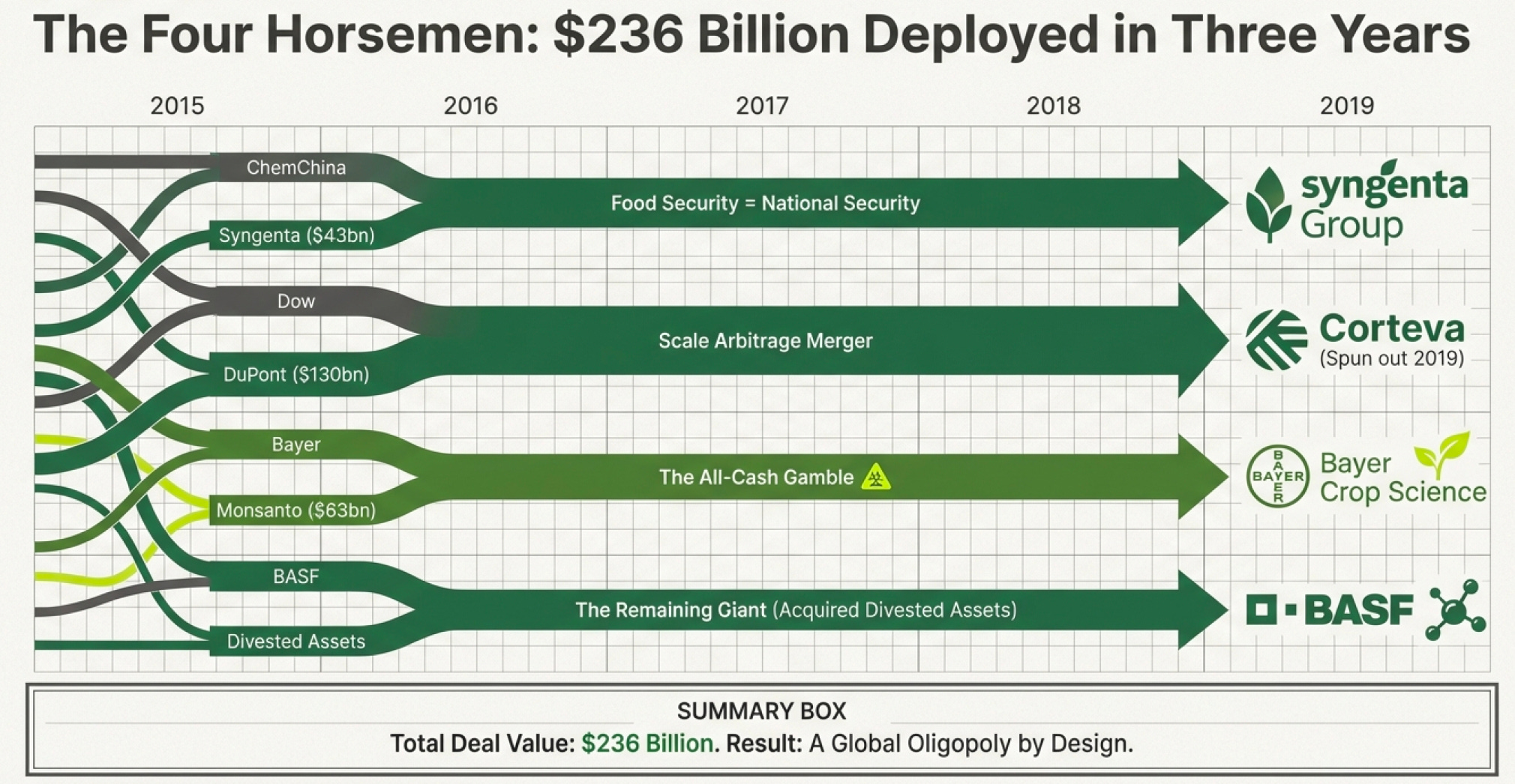

While Bayer was stepping on that landmine, something extraordinary was happening. The entire agricultural input industry was consolidating. And they did it in a three-year span:

2017: ChemChina buys Syngenta for $43 billion

2017: Dow and DuPont merge for $130 billion, later spinning out Corteva

2018: Bayer buys Monsanto for $63 billion

Total: $236 billion deployed

Why would rational executives create an oligopoly? Because oligopolies are wonderful businesses if you’re one of the oligopolists.

The China Move: When Food Security Becomes National Security

The ChemChina-Syngenta deal is the easiest to understand. China experienced famines that killed tens of millions within living memory. The Communist Party’s legitimacy rests on one promise: never again.

When ChemChina’s CEO Ren Jianxin proposed buying Syngenta—the world’s third-largest seed company and a top crop protection player—the Chinese government didn’t just approve it, they cheered. Syngenta brought access to genetic modification technology that security concerns had blocked. It brought 20% of the global pesticide market and 8% of the global seed market.

By 2020, China had merged Syngenta with Sinochem’s agricultural assets to create Syngenta Group—$27 billion in sales, 25% of the global agrochemical market. The single largest player.

Think about the barriers to entry this creates:

Government-Backed Competition: When your competitor has the backing of a government that views agriculture as national security, they can operate at different economic margins than you can. They can sustain losses to gain market share. They can access capital at below-market rates. They can leverage diplomatic pressure in emerging markets.

This isn’t your grandfather’s business competition. This is geopolitics disguised as agriculture.

The Dow-DuPont Dance: When Marriage Is Just for the Divorce

Here’s a beautiful piece of financial engineering. In 2017, Dow Chemical and DuPont announced a $130 billion “merger of equals.” But everyone knew the plan: merge, then immediately break into three pieces:

Dow (materials science)

DuPont (specialty products)

Corteva (agriculture)

Why this elaborate dance? Scale arbitrage.

Together, they could negotiate better divestitures with regulators. They could cherry-pick the best assets from each portfolio. They could cut overlapping costs. Then they’d split up, each piece focused and efficient.

Corteva inherited DuPont’s Pioneer corn business—dominant in corn genetics for decades—plus Dow’s crop protection chemicals. When it spun out in June 2019, it had $14 billion in revenue.

As of 2024, Corteva announced plans to split again—separating seeds from chemicals. Even within agriculture, the economics of seeds and chemicals are different enough that they might be worth more apart.

This is what happens when you have real moats—you can keep slicing the business and each piece is still valuable because the barriers to competition persist.

The Bayer Disaster: A Masterclass in What NOT to Buy

Now we return to Werner Baumann’s $63 billion question.

The thesis seemed solid:

Bayer had crop protection chemicals expertise

Monsanto had unparalleled seed and trait technology

Together they’d control over 25% of the world’s commercial seed and pesticide markets

Expected $1.2 billion in annual synergies

Pro forma sales of €45 billion

The DOJ (Department of Justice) required $9 billion in divestitures—largest ever in U.S. merger history. Bayer had to sell Liberty herbicide (competed with Roundup), cotton/canola/soybean seeds, even their digital agriculture business to BASF.

Two months after closing, a California jury ordered Bayer to pay $289 million to a groundskeeper who claimed Roundup caused his cancer. The floodgates opened.

Here’s what Bayer missed: The difference between an economic moat and a legal liability.

Roundup’s economic moat was spectacular—the bundled system of herbicide-resistant seeds plus herbicide created lock-in effects and pricing power. But the International Agency for Research on Cancer had classified glyphosate as “probably carcinogenic” in 2015. That legal risk was quantifiable. It just wasn’t quantified by Bayer’s dealmakers.

The Seven Locks on the Food Fortress

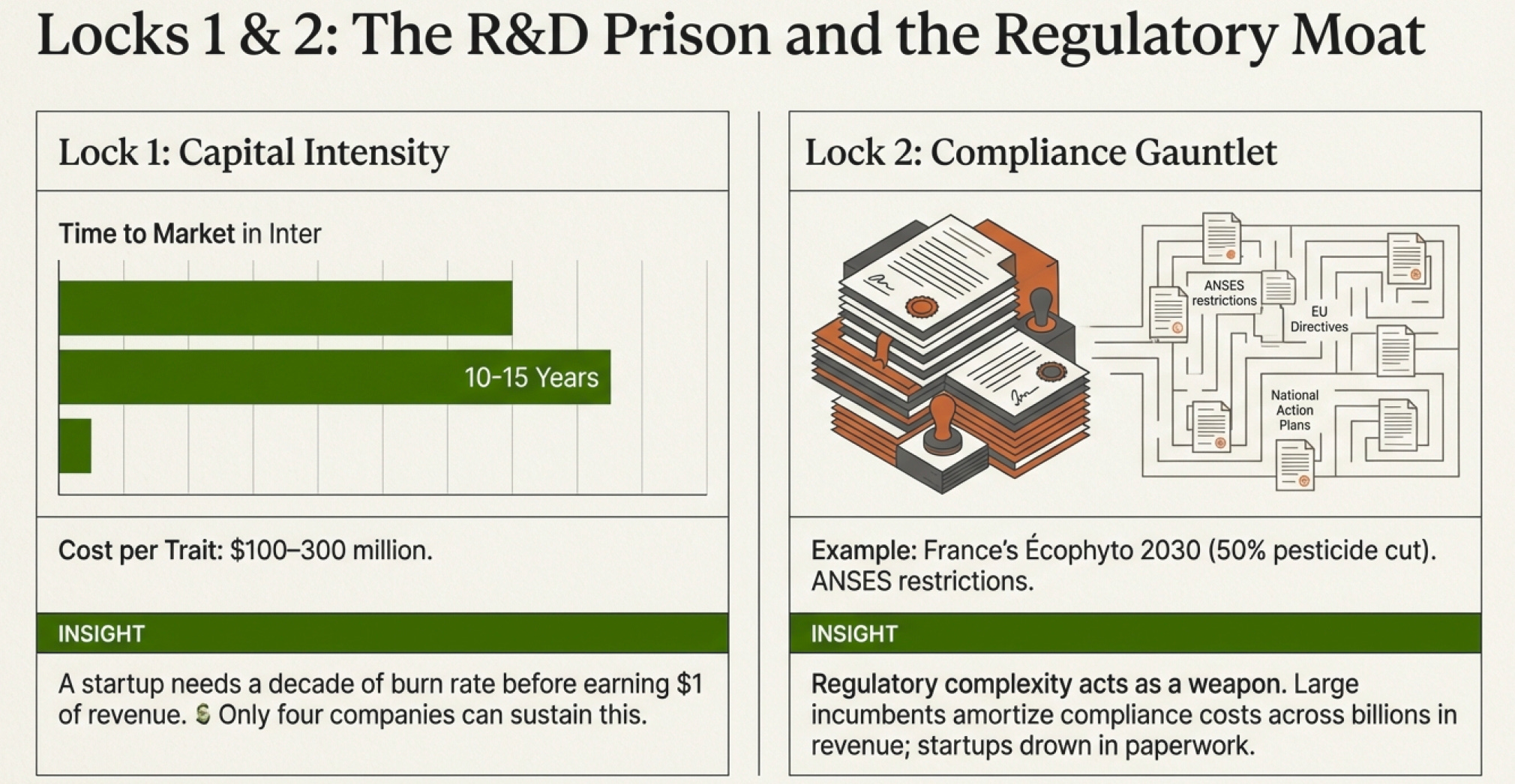

Let’s get specific about what makes this industry so defensible. These aren’t generic competitive advantages—these are brutal barriers that make entry nearly impossible.

Lock #1: The R&D Time-and-Money Prison

Developing a new crop trait takes 10-15 years and costs $100-300 million. That’s per trait. The combined Bayer-Monsanto entity spent €2.4 billion on R&D in 2017. Syngenta secured over 1,200 product approvals in 2025 alone.

Think about that from a startup’s perspective. You’d need:

A decade of burn rate before revenue

Hundreds of millions in capital

Expertise in molecular biology, genomics, agronomy, chemistry

Field testing across multiple growing seasons and geographies

Regulatory approval from EPA, ANSES, Chinese Ministry of Agriculture, and dozens more

And even if you succeed, your patent gives you 20 years—but you’ve already burned 10-15 getting to market. You have 5-10 years to recoup your investment before generics appear.

This is why only four companies play this game. The stakes are too high.

Lock #2: The Regulatory Moat (Or: How to Make Money Through Paperwork)

France’s Écophyto 2030 strategy mandates a 50% cut in synthetic pesticide use. ANSES, the French regulatory body, has halved approval times for biologicals while banning products like metam-sodium.

Each jurisdiction has different standards. Different testing requirements. Different timelines. Getting a product approved globally means running a regulatory gauntlet that costs millions in legal fees, studies, and lobbying.

Here’s the beautiful part: Regulatory complexity is itself a moat.

Large companies can spread compliance costs across hundreds of products. They can hire teams of regulatory specialists. They can absorb the risk of products that don’t make it through approval.

Small players can’t. This is why Syngenta, Bayer, Nufarm, BASF, and Corteva controlled 70% of the French market in 2024. Scale lets them digest costs that would choke smaller competitors.

Charlie Munger would love this: “Show me the incentive and I’ll show you the outcome.” Regulators want high safety standards. Companies want barriers to entry. Both get what they want—and consumers pay the bill through reduced competition.

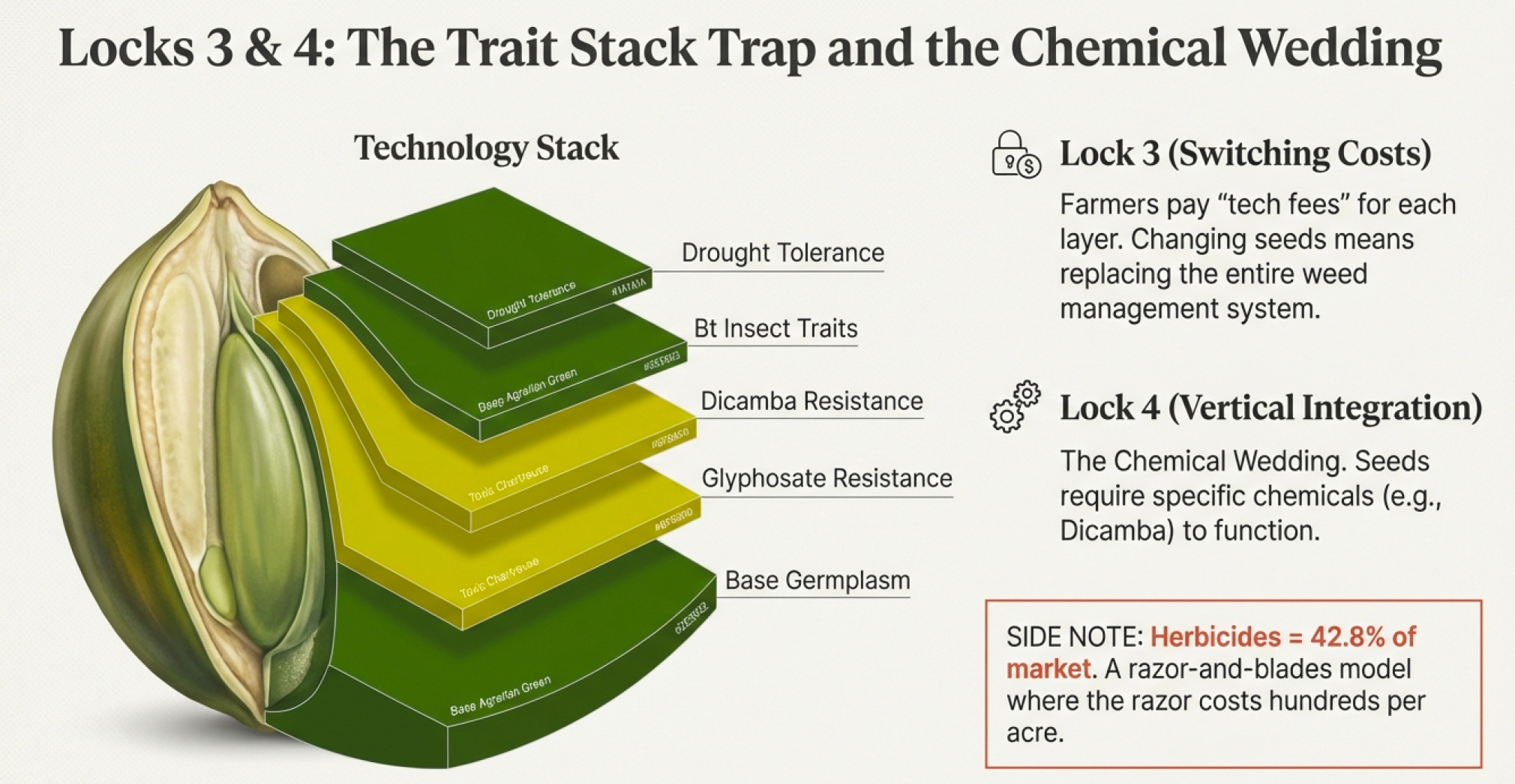

Lock #3: The Trait Stack Trap (Or: How to Make Farmers Buy the Same Thing Twice)

Modern seeds aren’t single products—they’re “trait stacks.” A premium soybean seed in 2024 might contain:

Glyphosate resistance (Roundup Ready)

Dicamba resistance (Roundup Ready Xtend, introduced 2016)

Bt traits for insect resistance

Drought tolerance genes

High-oleic acid content

Each trait is separately patented. Farmers pay technology fees that often exceed the base seed cost.

Here’s the trap: Once you adopt a trait stack, you’re locked in. Your weed management program assumes glyphosate resistance. Your insect control program assumes Bt traits. Switching to a competitor’s seeds means rebuilding your entire management system.

This is switching costs on steroids. It’s not just the hassle of learning new software—it’s potentially destroying your crop if you get it wrong.

Bayer’s Dekalb corn, Asgrow soybeans, and Channel brands (the value line launched April 2025) target different farmer segments. But they all use the same trait platforms. Once you’re in the Bayer ecosystem, you’re shopping within Bayer’s product line.

Lock #4: The Chemical Wedding (Or: Selling the Disease and the Cure)

Remember how this started: Roundup kills everything, except plants specifically engineered to resist Roundup.

That’s vertical integration disguised as innovation. You can’t use the seeds without the chemical. You can’t use the chemical without killing your crops unless you have the seeds.

The crop protection chemicals market is $104.83 billion in 2025, growing to $131.78 billion by 2030. Break it down:

Herbicides: 42.8% market share, highest forecast growth at 5.21% CAGR

Insecticides: Fast-growing segment

Fungicides: BASF’s fungicide business slightly exceeds their herbicide business

By application mode, foliar treatments captured 43.9% of market share in 2024. By crop type, grains and cereals grabbed 43.7%.

Here’s what this means: Farmers can’t just buy seeds. They need the complete system—seeds engineered for specific chemicals, chemicals that work with specific seeds, equipment calibrated for specific application modes.

It’s the razor-and-blades model, except both the razor and the blades cost hundreds of dollars per acre.

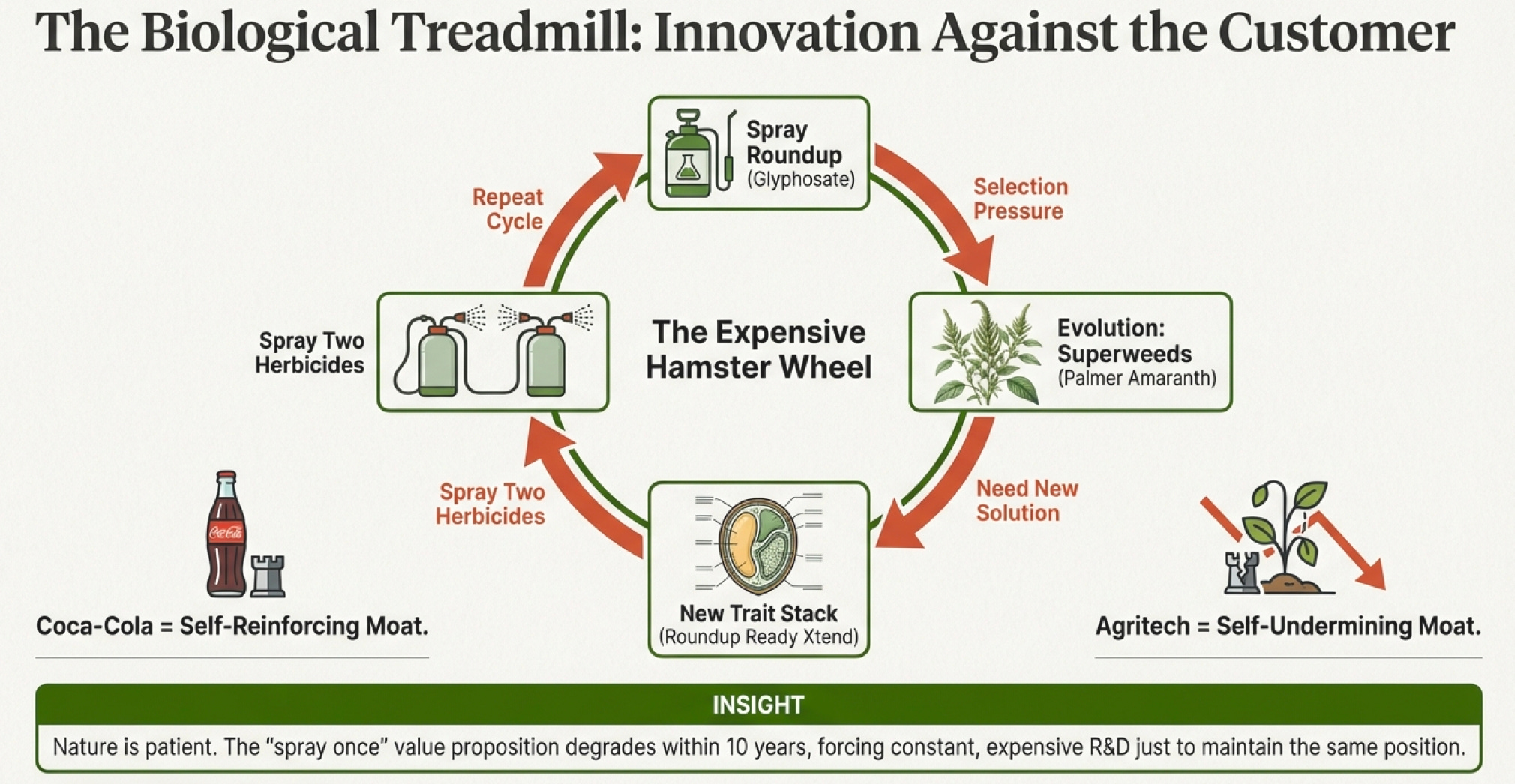

Lock #5: The Weed Arms Race (Or: Selling Solutions to Problems You Created)

Now here’s where it gets funny—and by funny, I mean economically predictable in a way that would make Charlie Munger cackle.

When you spray Roundup on millions of acres year after year, Darwinian evolution doesn’t take a vacation. Glyphosate-resistant weeds emerged: Palmer amaranth, horseweed, ryegrass. By the mid-2000s, “superweeds” were spreading.

Farmers who relied exclusively on Roundup were in trouble. They had to return to tillage and more toxic herbicides.

Monsanto’s solution? Roundup Ready Xtend soybeans, introduced in 2016. Modified to resist both dicamba and glyphosate. Now you spray two herbicides instead of one!

Xtend soybeans went from 1 million acres in 2016 to a projected 50 million by 2020.

Think about the business model:

Create an herbicide

Create resistance to the herbicide in your seeds

Wait for weeds to evolve resistance

Create new seeds resistant to multiple herbicides

Sell multiple herbicides

Wait for weeds to evolve resistance to those...

Repeat

It’s a technological treadmill. Farmers must continually adopt new trait stacks to stay ahead of resistance. From their perspective, it’s an expensive arms race. From an investor’s perspective, it’s beautiful—recurring revenue streams with pricing power.

Warren Buffett would call this “innovation against the customer.” But it works because what’s the alternative? Go back to manual weeding? Good luck with 1,000 acres.

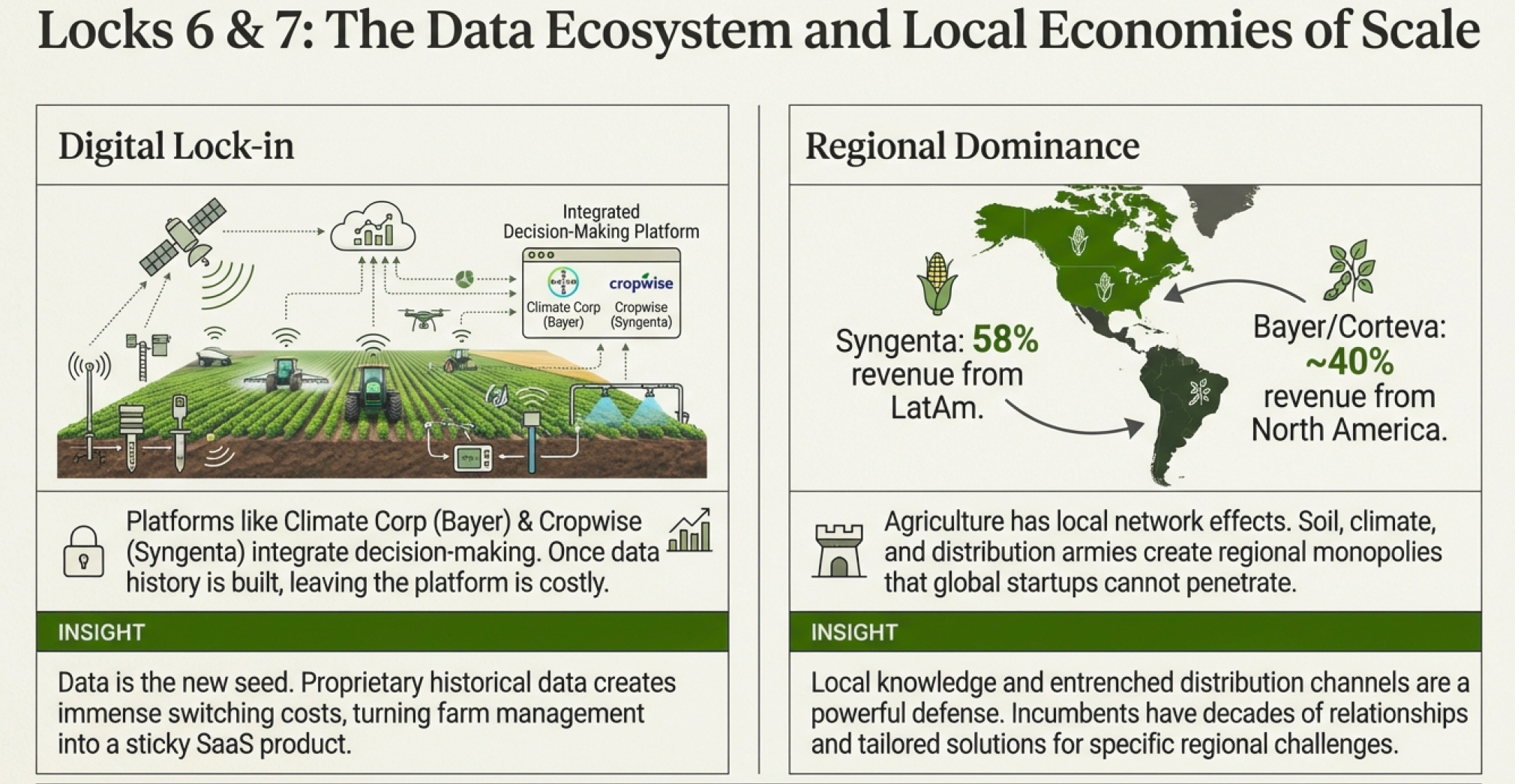

Lock #6: The Data Moat (Or: How They See Your Farm Better Than You Do)

The newest lock is digital. Every major ag company is racing to build platforms that capture and monetize farm data.

Climate Corporation (owned by Bayer) combines satellite imagery, soil sensors, weather data, and predictive analytics to optimize planting decisions and pesticide applications. In April 2024, BASF partnered with Climate Corporation to integrate real-time weather and pest pressure into fungicide timing tools.

Corteva’s digital agriculture focuses on variable-rate application—drones and precision sprayers that cut waste while maintaining efficacy.

Syngenta’s Cropwise platform, opened to developers in late 2025, aggregates data across multiple farms. Network effects emerge—insights from one grower benefit others.

Here’s how the data moat works:

Sensors monitor your field in real-time

ML models predict pest pressure and disease outbreaks

The platform recommends specific products (conveniently, products they manufacture)

Digital integration locks you into an ecosystem stickier than the old seed-and-spray bundles

South America leads in GPS variable-rate adoption at 35% of large farms, nearly doubling since 2022. France offers 40% tax credits on drift-reducing sprayers.

Once farmers adopt these platforms, they’re not just locked into the seeds and chemicals—they’re locked into the entire decision-making infrastructure.

Lock #7: The Geographic Fortress (Or: Local Scale Economies)

The market isn’t global—it’s regionally concentrated with local scale advantages:

Bayer: 42% of revenue from North America

Corteva: 39% North America

Syngenta: 58% Latin America

Adama: Most balanced—20.5% North America, 27.1% Europe, 25% Latin America, 27.4% Asia Pacific

Why does this matter? Because agriculture has local network effects:

Distribution networks in rural areas

Relationships with local dealers and co-ops

Understanding of local soil types, climate patterns, and pest pressures

Regulatory knowledge for each market

Field testing adapted to local conditions

A startup can’t just build a better seed and compete globally. They need to build regional presence with local agronomists, local distribution, local regulatory approval, and local credibility.

Syngenta’s dominance in Latin America—the world’s breadbasket for soybeans—gives them advantages a global competitor can’t easily replicate. They understand Brazilian soil. They know Argentine weather. They have relationships with local cooperatives.

The lesson: Some moats are national or regional, not global. But they’re just as defensible.

The Technology Treadmill Nobody Can Exit

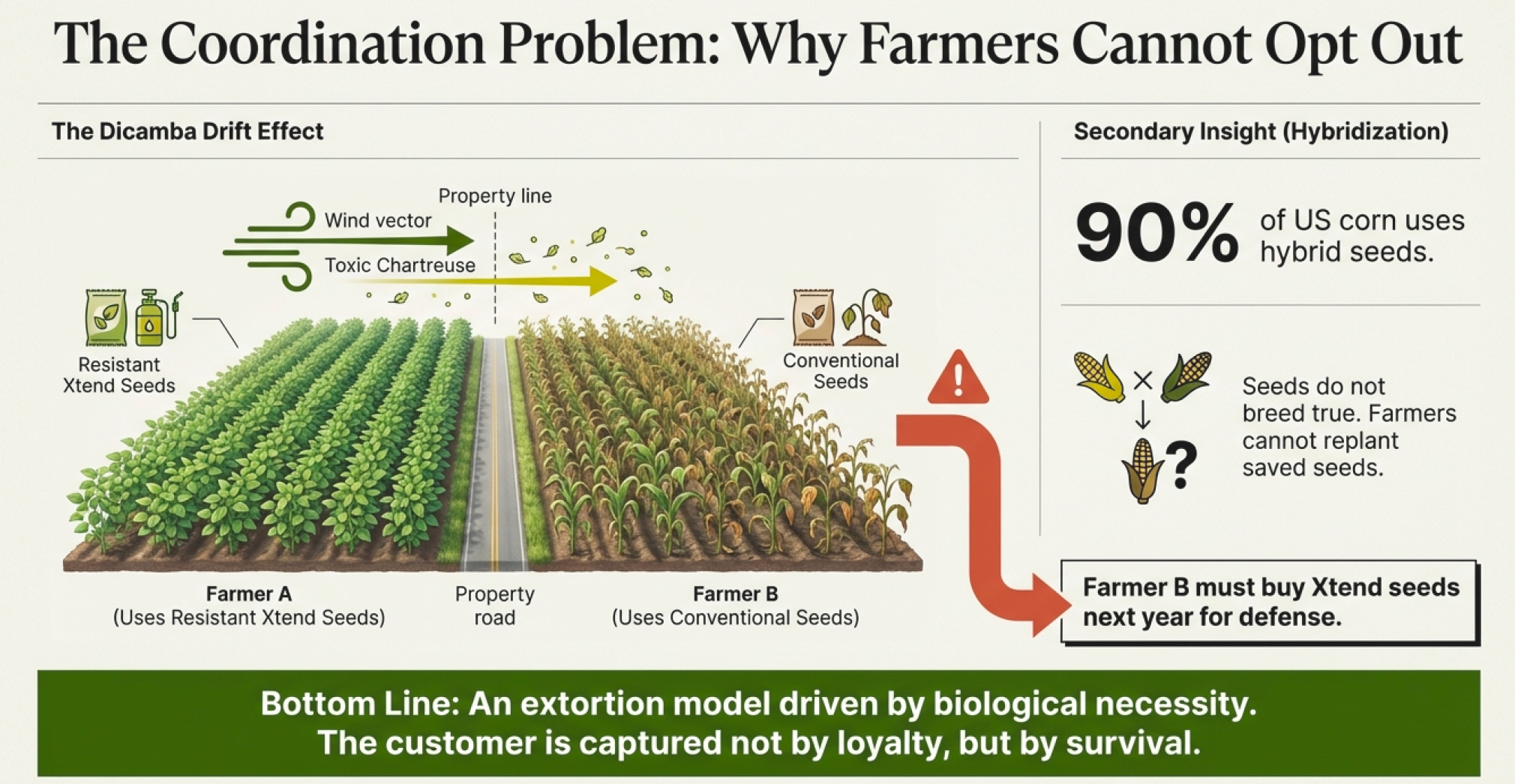

Let me paint you a picture of how deep these moats really are.

It’s 2016. You’re a corn farmer in Iowa. Your neighbor just planted Roundup Ready Xtend soybeans—resistant to both glyphosate and dicamba. He sprays dicamba on a windy day. The volatile herbicide drifts onto your field. Your soybeans—regular Roundup Ready, not Xtend—are damaged. Yield drops 20%.

What are your options?

Option A: Sue your neighbor. Good luck with that relationship. And proving wind drift damage is expensive.

Option B: Call Monsanto to complain. They’ll note your concerns and do nothing. Their Xtend seeds work perfectly—for people who bought them.

Option C: Switch to Xtend soybeans next year so drift doesn’t hurt you.

Which option do most farmers choose? Option C. Within a few years, everyone in the neighborhood is planting Xtend varieties.

This is what economists call a “coordination problem,” but farmers call it extortion. And it’s brilliant business design.

The same pattern repeats with every new trait release:

Corn rootworm develops resistance to Bt toxin → Buy next-gen Bt traits

Fall armyworm develops multi-toxin resistance → Buy stacked trait packages

Palmer amaranth resists glyphosate and dicamba → Buy seeds with even more resistance traits

Each generation of traits costs more. Each requires new complementary chemicals. Each locks you deeper into the ecosystem.

By 2024, hybrid seeds—which don’t breed true, forcing farmers to buy new seeds every year—captured 73.2% of market share, growing at 5.6% CAGR through 2030. Hybrid corn penetration exceeds 90% in the U.S.

Let me repeat that: 90% of U.S. corn uses seeds that don’t breed true. Farmers must buy new seeds every year. This isn’t accidental—it’s the business model.

Burridge’s law of product development: “Products will be designed to maximize company revenue, not customer welfare.” Agricultural biotechnology is Exhibit A.

The Numbers Game: What the Economics Actually Look Like

Let’s talk money, because that’s what reveals the real moat depth.

The R&D Arms Race

Combined Bayer-Monsanto R&D investment: €2.4 billion (2017)

Development cost per new trait: $100-300 million

Development time: 10-15 years

Patent protection: 20 years

Effective monopoly period: 5-10 years (after subtracting development time)

This creates a temporal moat. By the time your first generation of traits comes off patent, you’ve already released second and third generations that farmers have switched to. The old patents become worthless even before they expire because the new traits are objectively better.

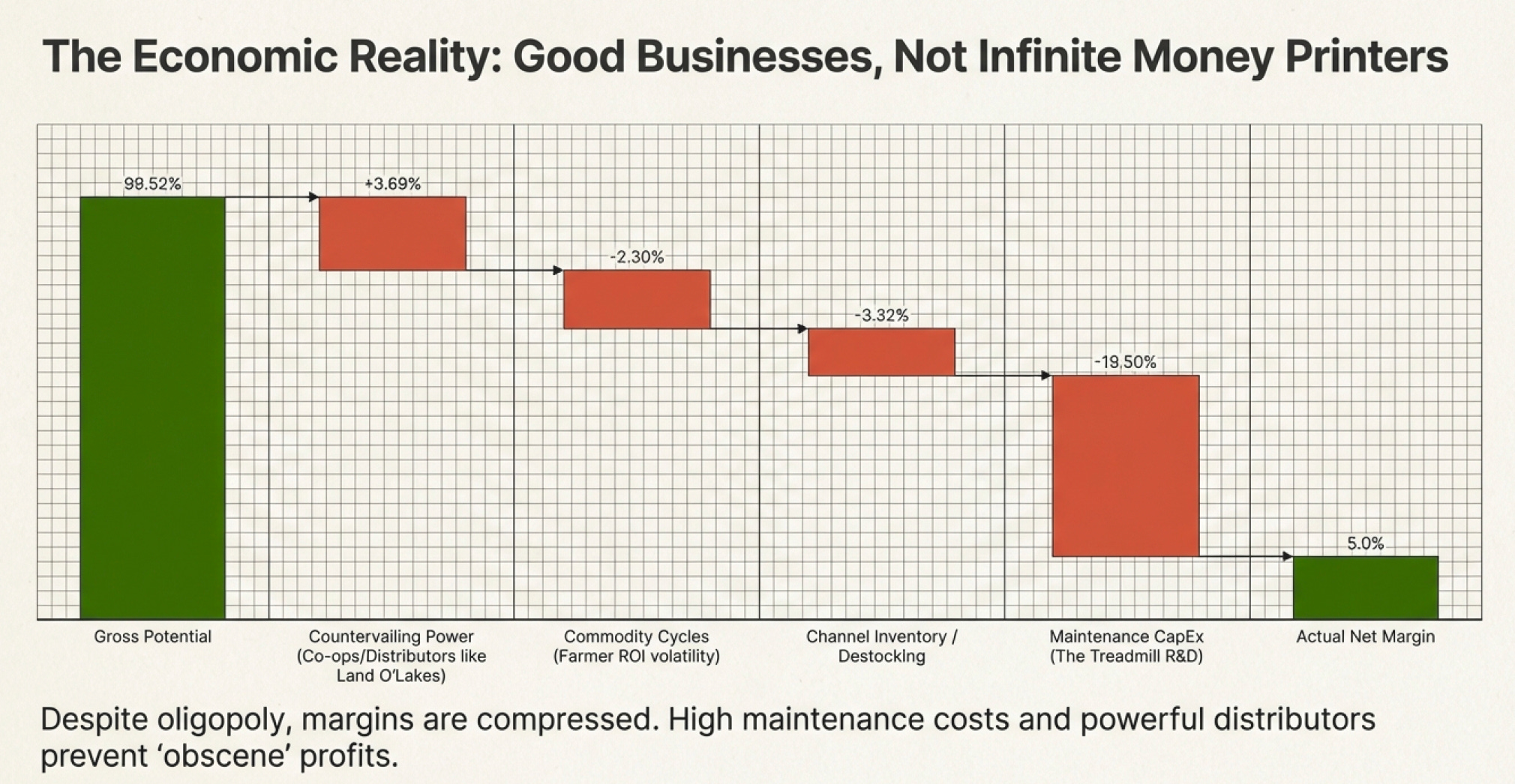

The Profit Margins

Here’s what’s fascinating: Despite massive consolidation and oligopolistic market structure, profit margins in agriculture aren’t obscene. Why not?

Countervailing power: Farmers organize through cooperatives and buying groups. Major distributors like Land O’Lakes and CHS have their own market power. They negotiate hard on price.

Commodity cycles: When corn prices are high, farmers invest in premium seeds. When prices collapse, they cut back ruthlessly. Input suppliers get whipsawed by commodity volatility.

Channel inventory volatility: In 2024, severe weather and channel destocking hit crop protection sales hard. Distributors carried excess inventory, depressing orders even as end-demand remained stable. This creates earnings cyclicality that obscures underlying economics.

Regulatory costs: Compliance spending never stops. Every product faces periodic re-evaluation. Glyphosate battles cost hundreds of millions in legal fees, studies, and lobbying before you even face lawsuits.

The result? Good businesses, not great ones—unless you’re one of the four survivors. Then it’s pretty good.

The Geographic Lottery

Regional concentration creates interesting economics:

North America (high-value acres): Corn and soybeans with premium traits. High spending per acre. Strong distribution infrastructure. But cyclical—deeply tied to commodity prices and land values.

Latin America (massive scale): Brazil is the world’s soybean breadbasket. Argentina follows. Intense price competition. Currency volatility. But projected to grow at 4.85% CAGR through 2030.

Asia-Pacific (fragmented smallholders): Highest projected growth CAGR. But fragmented markets mean higher costs to reach farmers. China is unique—state-backed Syngenta Group can leverage government relationships that foreign companies can’t match.

Europe (regulatory nightmare): France mandates 50% cuts in synthetic pesticide use by 2030. ANSES fast-tracks biologicals while banning traditional chemistries. High regulatory costs, uncertain market structure. But also premium pricing for approved products.

Companies with balanced geographic exposure (like Adama) avoid concentration risk but sacrifice local scale economies. Companies with concentrated exposure (like Corteva at 39% North America) get local scale but high cyclical risk.

The Resistance Problem: When Your Product Trains Its Own Competitors

Let me tell you my favorite part of this whole story, because it reveals something profound about business moats.

The Roundup Ready system was economically perfect. Patents protected the genes. Bundling protected the business model. Farmer desperation protected demand. It should have lasted decades.

It lasted about ten years before nature found the cracks.

Palmer amaranth—a weed—evolved resistance to glyphosate through random mutation and selection pressure. Nothing fancy. Just Darwin being Darwin. Now Palmer amaranth infests millions of acres across the South. It can grow three inches per day. It produces up to 1 million seeds per plant. It’s resistant to glyphosate, and many populations are now resistant to multiple herbicide classes.

From a business perspective, this is both disaster and opportunity:

Disaster: The core Roundup Ready value proposition degrades. Farmers need additional herbicides, additional applications, additional costs. The “spray once and you’re done” simplicity disappears.

Opportunity: Sell farmers the next generation of trait stacks! Roundup Ready Xtend adds dicamba resistance. Future generations will add resistance to even more herbicide classes.

It’s a treadmill. The products create the problem, then new products solve the problem, then those products create new problems, ad infinitum.

Here’s the thing Warren Buffett would notice: This is not a durable moat. It’s an expensive hamster wheel.

True moats last decades with minimal maintenance. Coca-Cola’s brand doesn’t degrade because consumers drink Coke. Visa’s network doesn’t weaken because merchants accept Visa cards. These are self-reinforcing moats.

Agricultural biotechnology moats are self-undermining. The more successfully you deploy them, the faster you trigger evolutionary resistance that requires new R&D to overcome.

The companies are running a race they can never win. They can only keep running. That’s profitable—but it’s exhausting. And it means the R&D spending can never stop, which means the cash flows can never fully convert to owner earnings, which means the intrinsic value is lower than it superficially appears.

The Future That’s Already Here: Biologicals, Gene Editing, and Climate Stress

Now the plot thickens. Because while the Big Four are locked in their chemical-seed arms race, technology is shifting underneath them.

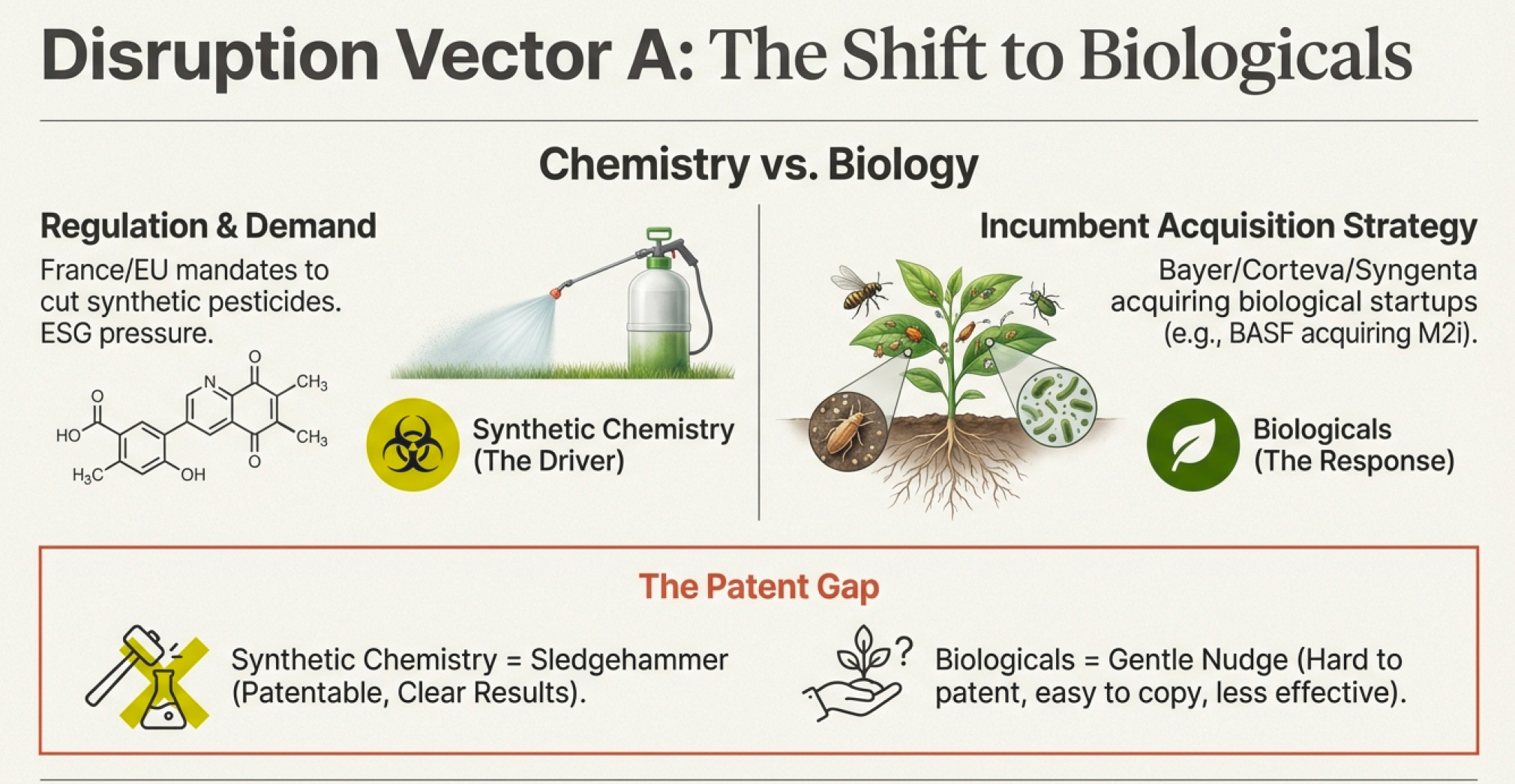

The Biologicals Wave

Syngenta, Corteva, and Bayer have all entered biologicals—using natural pest enemies and beneficial microorganisms instead of synthetic chemicals.

Why the sudden enthusiasm for “nature-based solutions” from companies that built empires on synthetic chemistry?

Reason 1: Regulatory pressure. France’s 50% pesticide use reduction mandate isn’t optional. ANSES fast-tracks biological approvals. Adapt or die.

Reason 2: Consumer preference. Organic food markets are growing. “Sustainable agriculture” scores points with ESG investors and retail buyers.

Reason 3: Resistance is slower. Biological controls use multiple mechanisms, making single-resistance mutations less effective. The treadmill might run slower.

BASF acquired M2i Life Sciences in August 2024 for biocontrols in vines and fruits. Corteva acquired Symborg in 2024 to expand microbial platforms.

But here’s the economics problem with biologicals: They’re harder to patent, easier to copy, and often less effective.

A specific bacterium species is harder to protect legally than a novel chemical molecule. Competitors can find similar microorganisms. Farmers can potentially propagate their own if the biology is simple enough.

And effectiveness? Synthetic chemicals are sledgehammers. Biologicals are more like gentle nudges. They work—but not with the same dramatic, reliable results that made farmers fall in love with Roundup.

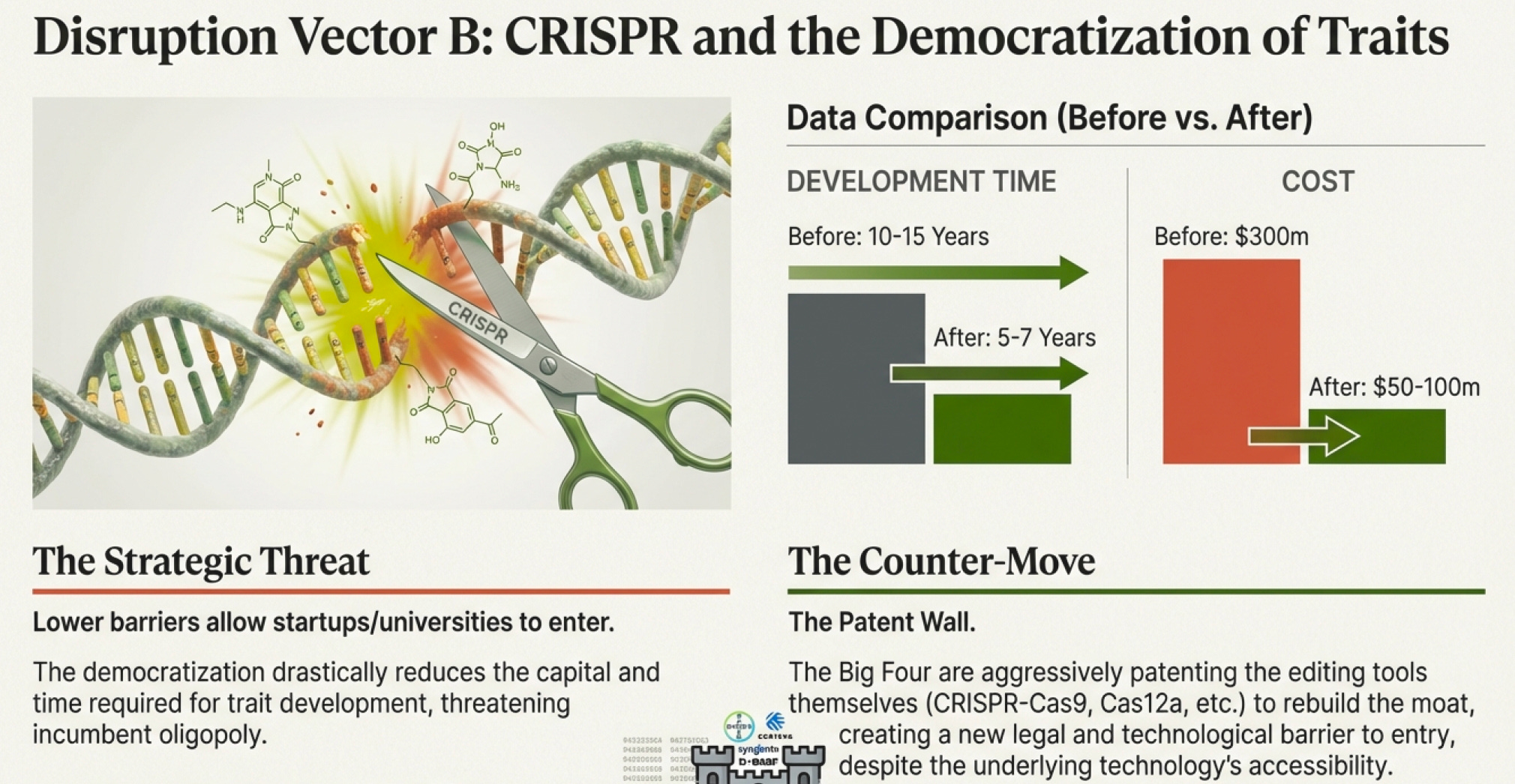

Gene Editing: CRISPR Changes Everything (Maybe)

In May 2025, Syngenta partnered with Tropic Biosciences for gene-edited coffee, rice, and banana varieties with disease resistance and better nutrition.

CRISPR gene editing is precise—snip specific genes, insert specific sequences, done. Earlier GMO techniques were crude: fire genes into cells randomly, hope something works, breed out the failures.

The economic promise of CRISPR:

Faster development (maybe 5-7 years instead of 10-15)

Lower costs (maybe $50-100 million instead of $100-300 million)

Potentially lighter regulatory burdens (some jurisdictions don’t classify precise gene editing as “GMO”)

If CRISPR delivers on these promises, it lowers barriers to entry. That’s bad for incumbents. Smaller players could enter the trait development game. University research could commercialize faster. Startups could specialize in specific crops or regions.

But—and this is crucial—the incumbents aren’t sitting still. They’re filing CRISPR patents aggressively. They’re acquiring CRISPR startups. They’re building CRISPR expertise in-house.

The race is on to patent the fundamental CRISPR tools and techniques before anyone else can use them. If the Big Four succeed, they’ll just rebuild their moats using new technology. If they fail, the industry could fragment.

Right now, mid-2026, it’s too early to tell. But watch the patent battles. They’ll determine whether CRISPR democratizes agriculture or just gives the incumbents cheaper tools to maintain control.

What Feeds the World Also Bleeds the World

Let me end with a thought experiment.

Imagine you’re a farmer in 2025. You need to feed your family and pay your mortgage. Weeds, insects, diseases, and weather all threaten your crop. You don’t particularly love Bayer or Corteva or Syngenta, but their products work.

The seed company offers you:

Seeds that resist herbicides and insects

Chemicals that kill weeds and pests

Digital tools that optimize application

Financing to pay for all of it

You’re locked in. But honestly? It beats the alternative of going back to 1950s farming techniques.

Now imagine you’re an investor in 2025. You see an oligopolistic market structure. You see regulatory barriers. You see technological complexity. You see 60% market share concentrated in four companies.

But you also see:

Evolutionary resistance undermining products

Legal liabilities from past conduct

Regulatory trends toward biologicals (lower margin businesses)

Climate uncertainty creating winner-take-all outcomes

Geopolitical risk (China controls one of the four champions)

These are good businesses—but not obviously great investments at current prices.

The agriculture sector is a fortress. But fortresses are expensive to maintain, occasionally besieged by unexpected enemies, and sometimes built on foundations that crumble slowly.

Understanding the moats isn’t enough. You need to understand the rate at which they erode, the cost to repair them, and whether the economics justify the maintenance expense.

That’s the real lesson of Bayer’s $63 billion disaster. They understood Monsanto’s moats. They just didn’t understand that some moats have bodies floating in them, and sometimes those bodies float to the surface at the worst possible time.

The four companies feeding the world have built something remarkable—a system of interlocking patents, chemicals, seeds, data, and relationships that’s nearly impossible to compete against. But “nearly impossible” isn’t the same as “invincible.”

Nature is patient. Weeds adapt. Regulations tighten. Lawyers multiply. Climate shifts. And somewhere, probably in a university lab or a startup garage, someone is working on the technology that makes today’s traits obsolete.

That’s capitalism. Creative destruction runs on a slower clock in agriculture than in software, but it runs nonetheless.

The Big Four are kings today. How long they stay kings depends on how fast the world changes underneath them—and whether their moats can handle the pressure.

Exceptional breakdown of how agritech moats actually work. The Palmer amaranth example nails something most people miss--these aren't self-reinforcing moats like Coke's brand, theyre self-undermining ones that require constant R&D just to maintain position. Ive followed this sector for a while and the treadmill economics are wild when you see how quickly resistance develops.