17 Oct 2025 - Centene ($CNC)

🔑 Introduction

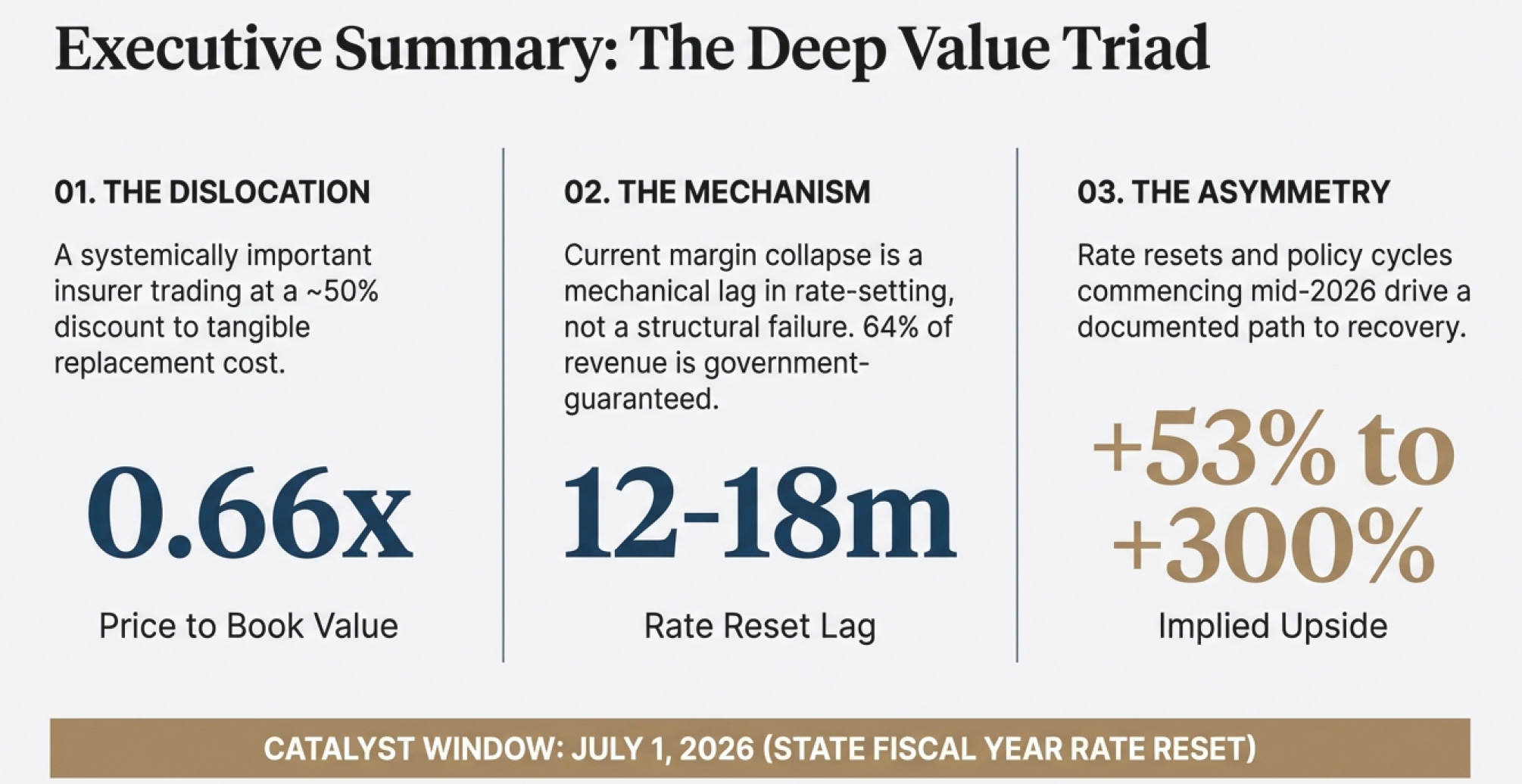

This research note explains why I’m investing in Centene Corporation (CNC) using long-dated LEAP options and a deep-value approach. My strategy focuses on thorough financial analysis combined with understanding policy cycles, industry structure, and how the U.S. healthcare system actually works. I look for companies with solid fundamentals that the market temporarily misunderstands—not stocks driven by short-term hype.

Centene is a perfect example of this disconnect. The company operates in a massive, essential market backed by government funding. Yet it trades at a steep discount to both its book value and what similar Medicaid-focused companies have sold for in acquisitions. Why? The market is focused on temporary issues: short-term cost pressures, unresolved state settlements, and uncertainty around the ACA marketplace.

But the long-term fundamentals remain strong:

Stable enrollment that actually grows during economic downturns

State-guaranteed payments for coverage

Low customer acquisition costs

Expanding populations with complex healthcare needs

This research breaks down what makes Centene valuable, explains the structural advantages of Medicaid managed care, and shows why the next 12–24 months could be a turning point. Several catalysts are coming: rate resets, potential economic softening, legal resolutions, and state-level pricing corrections. I believe the market is significantly underestimating both Centene’s earning power and balance sheet strength.

My goal with this Substack goes beyond sharing a stock pick. I want to show you, transparently, how I analyze companies, find asymmetric opportunities, and build conviction when others see only uncertainty. Centene is exactly this type of opportunity: a misunderstood, systemically important insurer with durable economics, trading at prices that assume far worse outcomes than the fundamentals support. As this is a deep value analysis, i will focus delivering my points via 3 sections

How many birds are in the bush

How sure are you

How fast till you get them out

But first, let’s have some context and take a look at what happened.

🔑 Why Did Centene’s Stock Price Collapse?

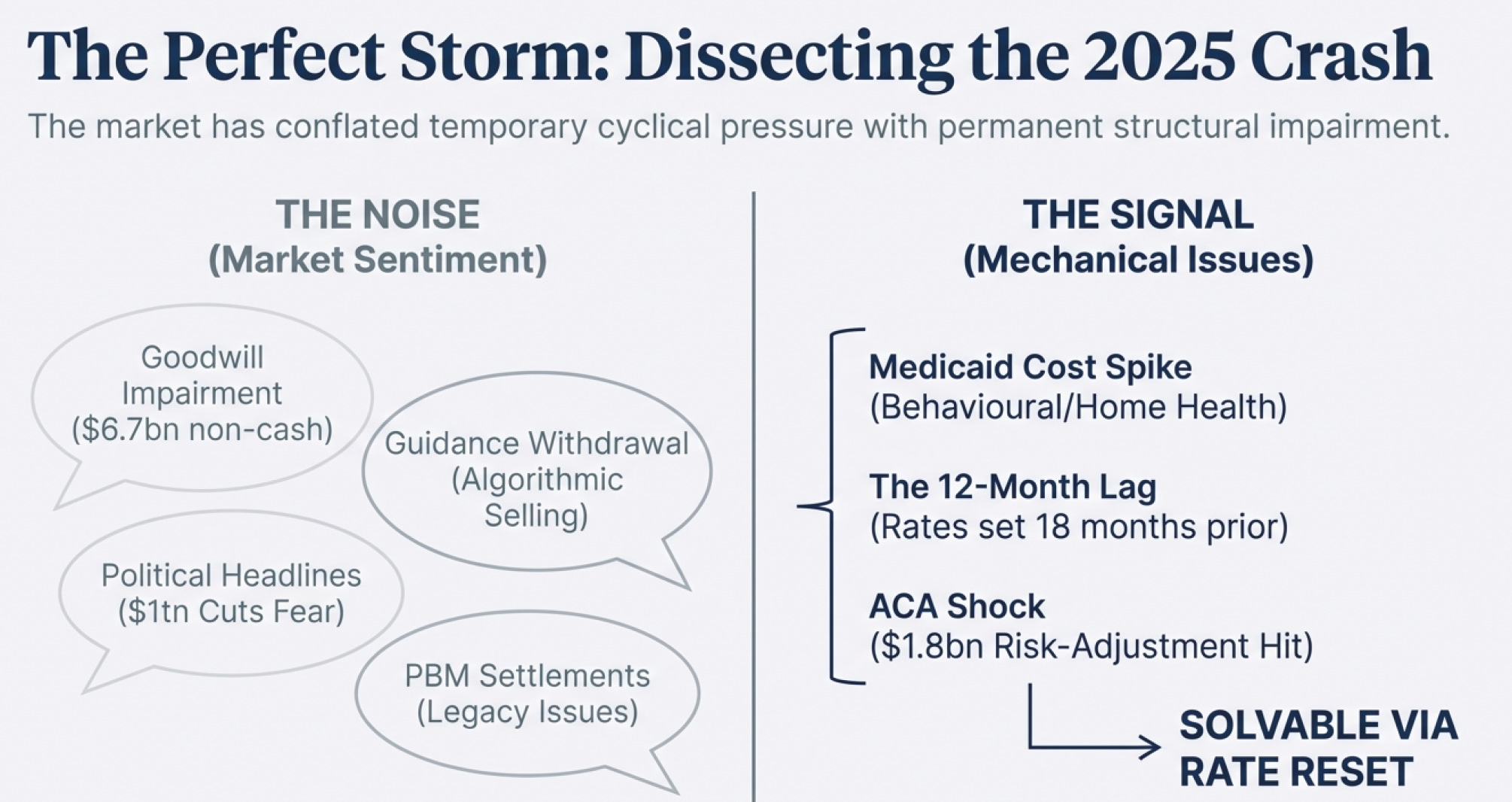

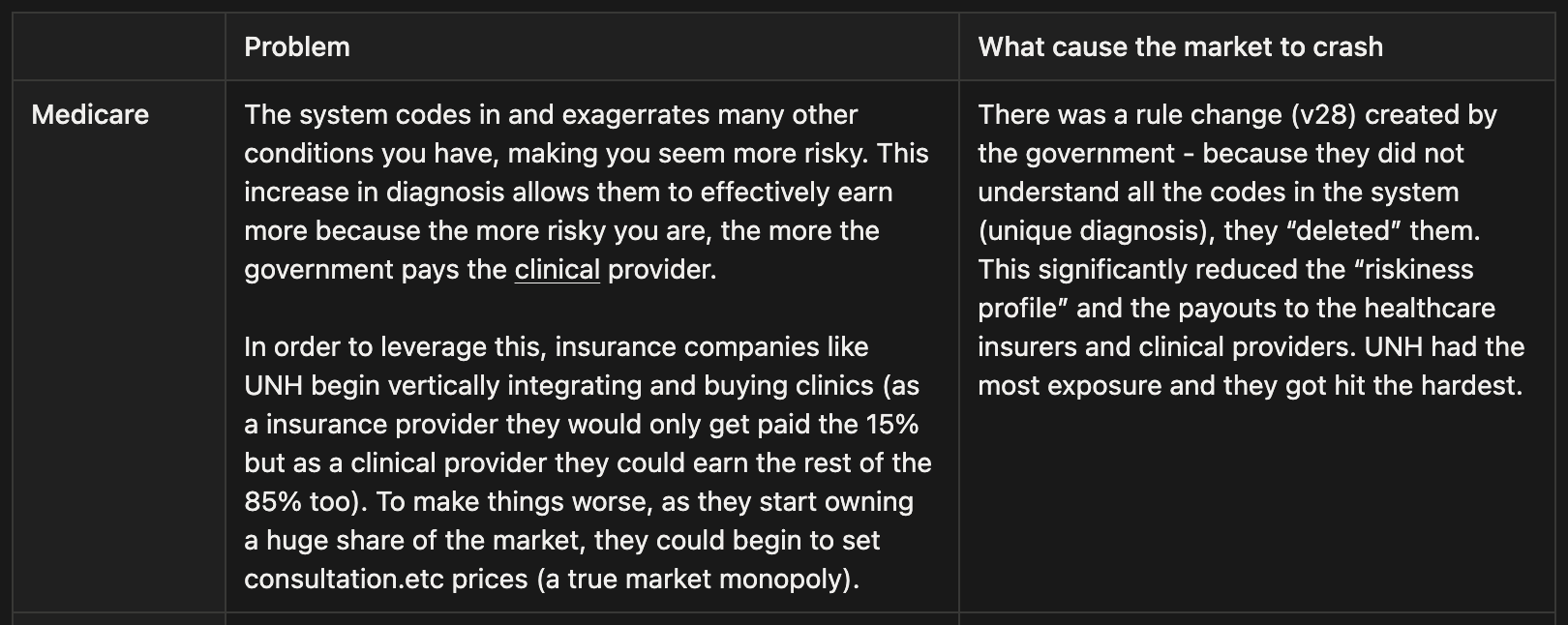

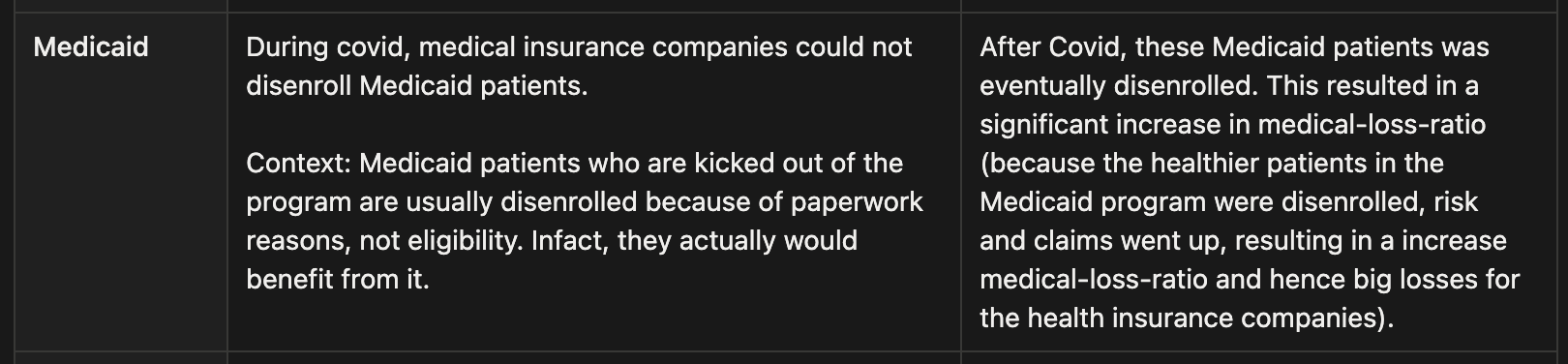

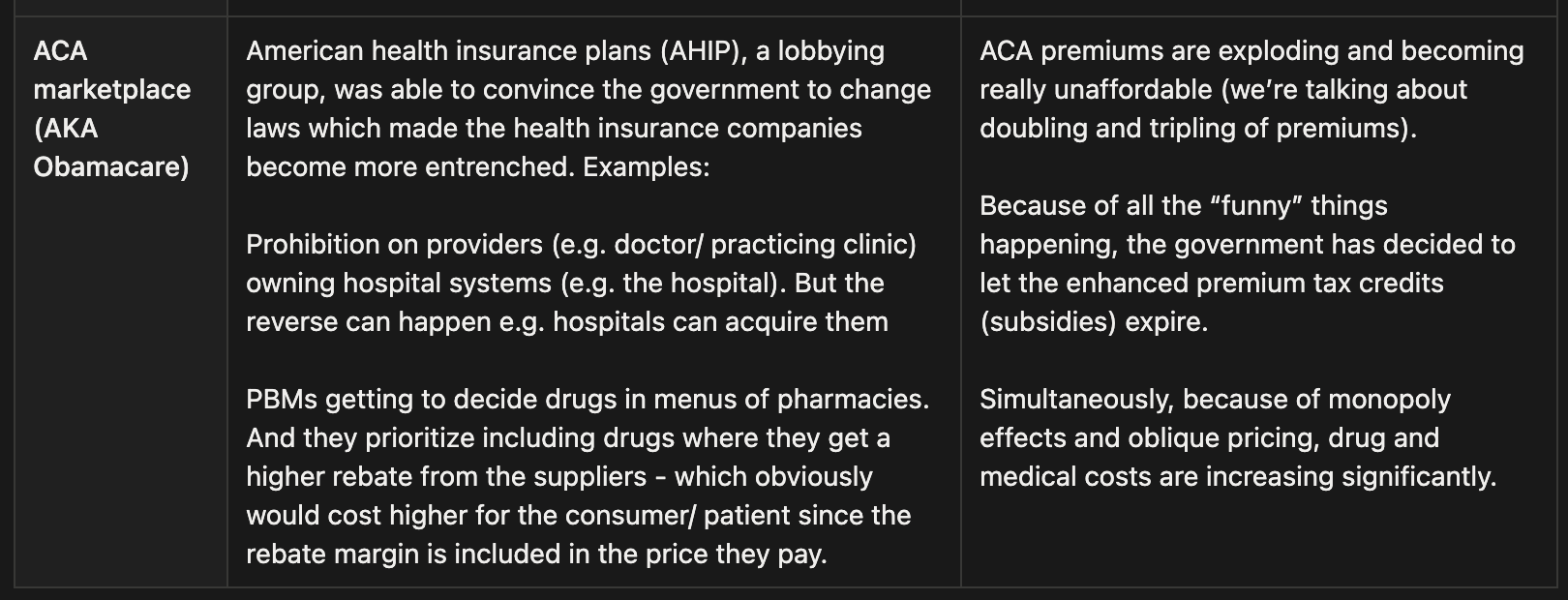

Centene’s sharp decline in 2025 was not caused by a single issue, but by several simultaneous, documented pressure points that created the appearance of structural weakness — even though most were temporary, mechanical, or already in the process of being resolved.

1. Medicaid Costs Spiked Faster Than Rates Adjusted

In mid-2025, Centene reported a sudden jump in medical costs — particularly in behavioral health, home health, and specialty drugs.

Its Health Benefits Ratio surged to 93%, far above expectations.

But Medicaid rates are set 12–18 months in advance, so Centene was still being paid based on old cost assumptions.

This created a temporary margin squeeze that alarmed investors.

Note: When we look at June 2024 and previous years, COGs is only 88%. However, as of the recent quarter, that has increased significantly by 5% - which is pretty significant. The company mentioned that it was due to Medicaid cost increase (due to higher utilization in (1) behavioral health, (2) home health, and (3) other high-cost drugs)

2. ACA Marketplace Shock: $1.8 Billion Risk-Adjustment Hit

An independent actuarial review found that ACA Marketplace members were sicker than Centene had assumed.

The company was told it would receive $1.8 billion less in risk-adjustment transfers — a major earnings shock that hit all at once and triggered a selloff.

3. Withdrawal of Financial Guidance

In 2025, Centene withdrew its full-year guidance and later reinstated a lower one.

Historically, withdrawing guidance is interpreted as a red flag for financial uncertainty, leading to heavy selling from institutions and quant funds.

4. Industry-Wide Medicaid Margin Compression

Every major Medicaid insurer — Elevance, UnitedHealth, Molina, CVS — reported the same pattern:

higher acuity, higher utilization, and a widening gap between medical costs and state reimbursement.

Because the entire sector flagged the same issue, investors assumed a prolonged downturn.

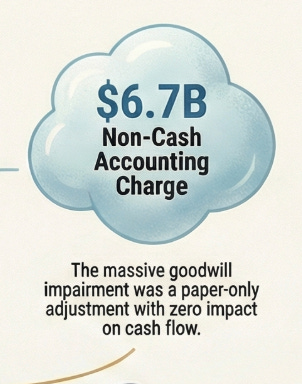

5. Goodwill Impairment of $6.7 Billion

In October 2025, Centene recorded a $6.7B goodwill impairment due to an anticipated deep cut to Medicaid and ACA subsidies from the new “One Big Beautiful Bill Act,” - which reduced the company’s expected future value.

Although this was a non-cash accounting charge, headlines amplified the perception of deeper operational problems.

6. PBM Settlement Overhangs Across 20+ States

Centene’s former PBM subsidiary was accused of overbilling Medicaid programs, resulting in $1B+ in settlements across many states.

While most major settlements were already paid, a few “holdout” investigations — including Florida — created the impression of open-ended legal risk, even though the financial exposure was largely contained.

7. Political Noise Around Potential Medicaid Cuts

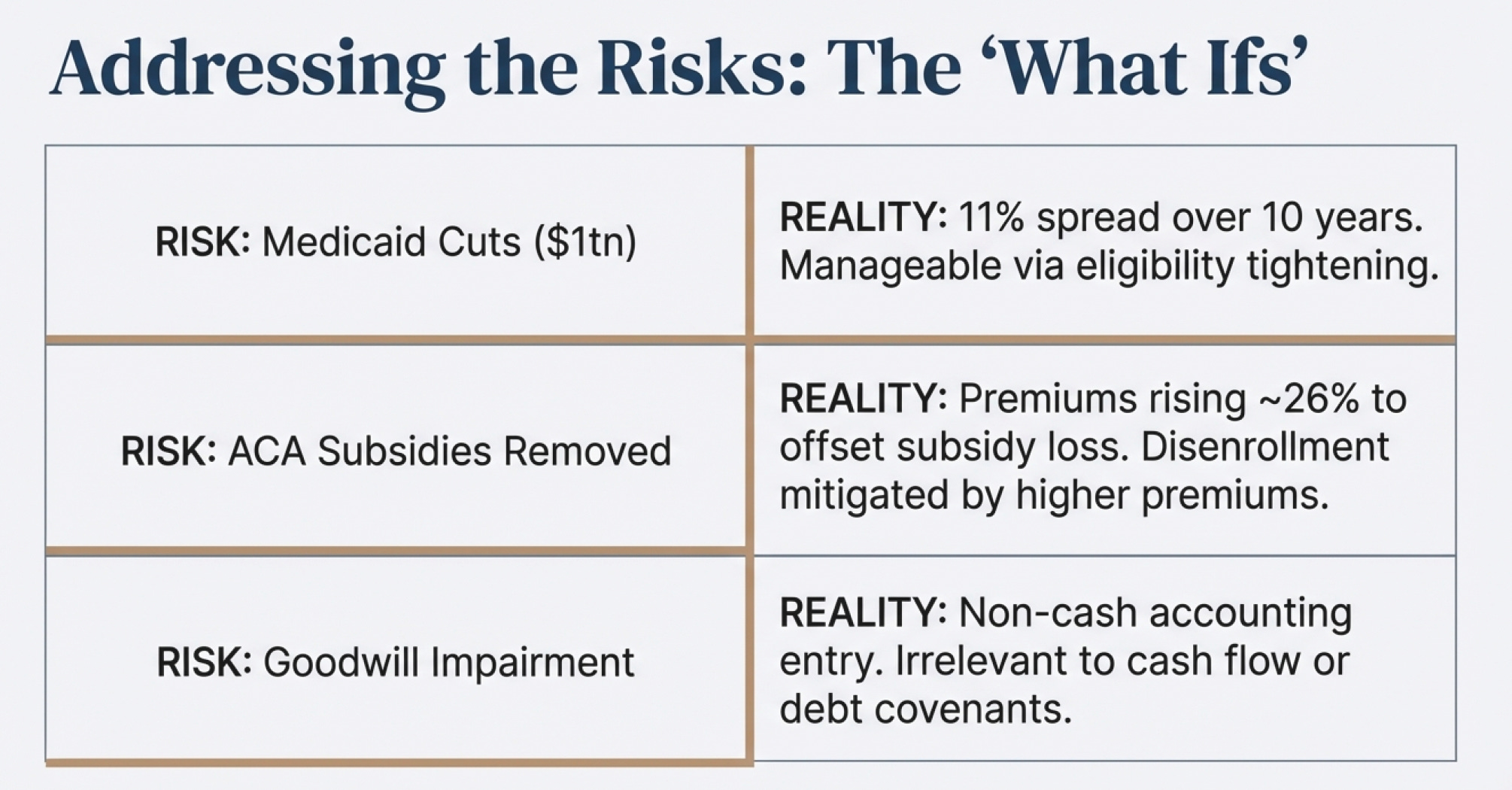

Federal discussions about reducing Medicaid spending by $1 trillion over 10 years fed fears that the entire Medicaid market would shrink.

Despite the actual impact being roughly a 10% decade-long reduction, the headline number alone fueled selling pressure.

🔑 How Many Birds Are in the Bush

The Value Floor: What Centene Is Worth at Minimum

Let’s start with the most conservative scenario—liquidation value. Even if everything went wrong and Centene had to sell off its business piece by piece, what would it be worth?

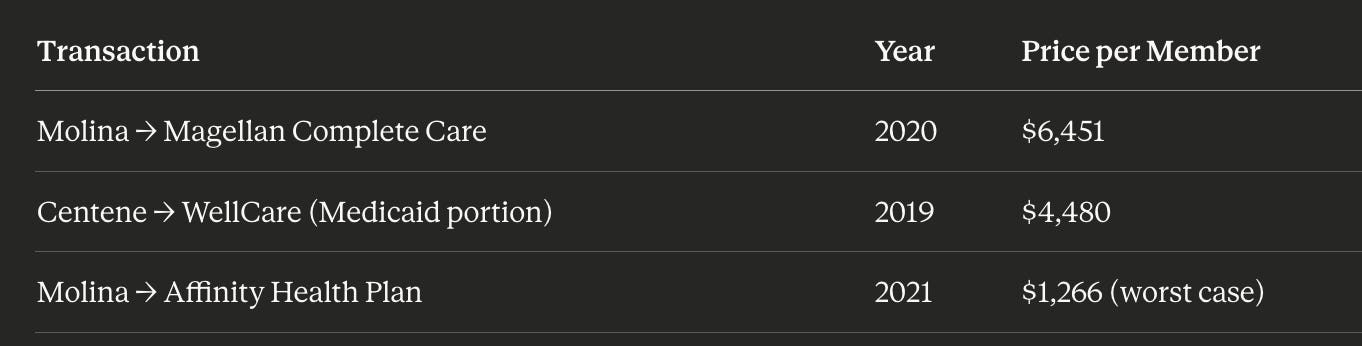

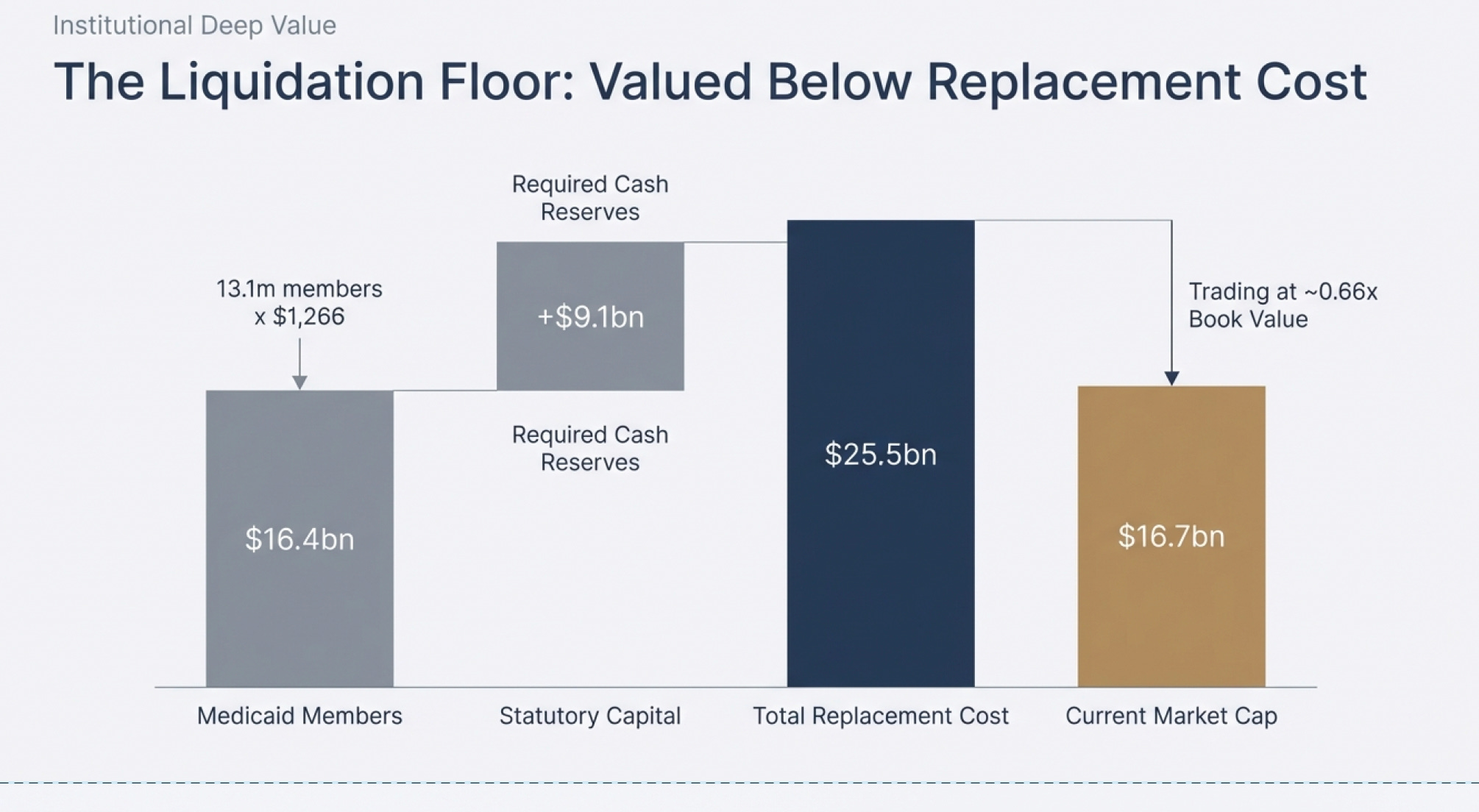

The Medicaid Book Alone: Centene’s Medicaid business (64% of total revenue) serves 13.1 million members. Looking at comparable transactions where Medicaid member bases changed hands, the worst-case valuation was $1,266 per member (Molina’s acquisition of Affinity Health Plan in 2021). At that rock-bottom multiple:

13.1 million members × $1,266 (worst case due to their financial dificulties) = $16.4 billion

But here’s the critical part: Centene isn’t going out of business. As a managed care organization, they’re required by law to maintain statutory capital reserves to operate. That requirement is currently $9.1 billion (and since this is what is required to compete in the business, we can add that in to derive replacement cost of the business).

Since the company is financially sound and will continue operating, we add this back:

Replacement cost: $16.4B + $9.1B = $25.5 billion minimum value

Replacement cost is used instead of liquidation value because we expect the business to continue operating. The $9.1 billion is added back because that is the capital requirement for a new competitor to “set-up shop” to compete with Centene at their current level

And remember—this completely ignores:

The Marketplace business (21% of revenue)

The Medicare business (14% of revenue)

Any premium for being a going concern with established state contracts

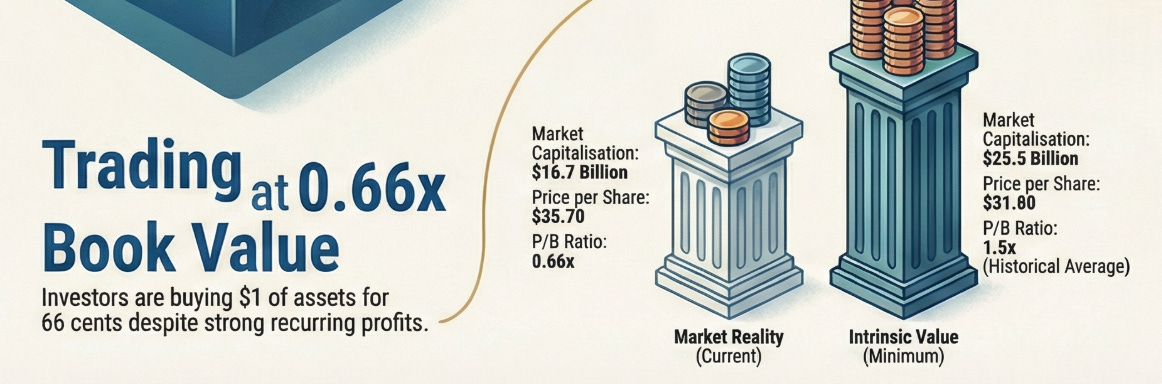

Current market cap: $16.7 billion

The market is valuing Centene below just its Medicaid liquidation value plus required capital. That’s absurd for a functioning, systemically important insurer.

The Book Value Reality Check

Now let’s look at what Centene owns on its balance sheet:

Book value per share: $33 ($16.4B ÷ 492 million shares outstanding)

Replacement cost per share (minimum) = $51.8 ($25.5B ÷ 492 million shares outstanding)

Current price per share: $35.70

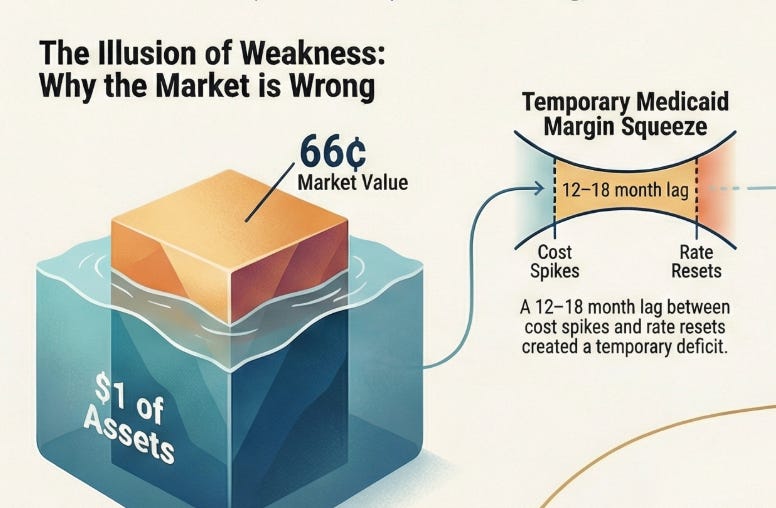

Trading at 0.66× book value

This means you’re buying a dollar’s worth of assets for 66 cents. But it gets more interesting when you compare this to industry norms:

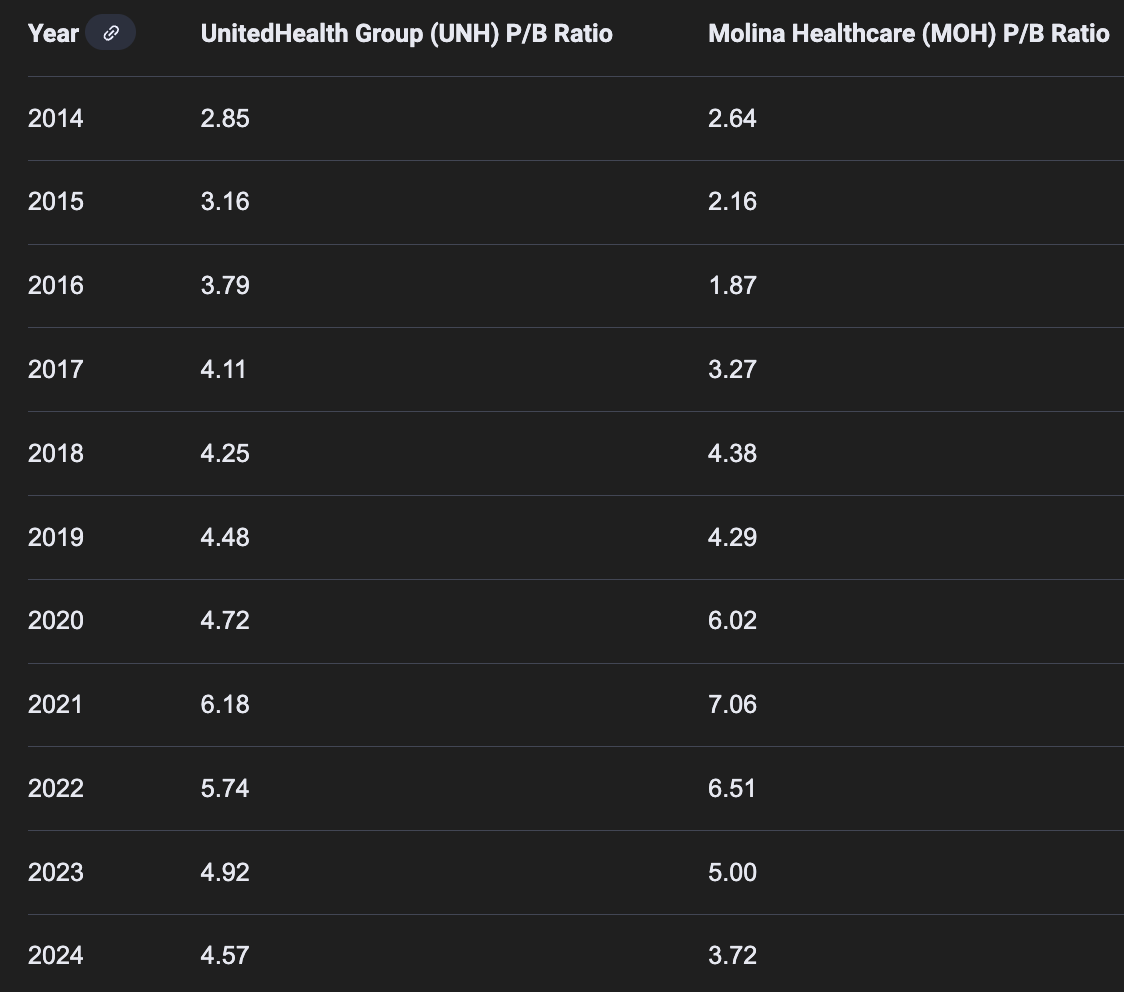

Managed care sector average P/B ratio: about 3×

Centene’s historical P/B ratio: about 1.5×

P.S. Molina’s revenue consist of 70-80% of Medicaid, more than Centene’s c.60%. Most MCO P/B is suppressed due to the lower margins and growth of Medicaid. But as we can see here, the discrepancy between Molina and Centene is LARGE

Even if Centene never returns to sector-average multiples (which would be generous given the current pessimism), just reverting to its own historical average of 1.5× book value implies:

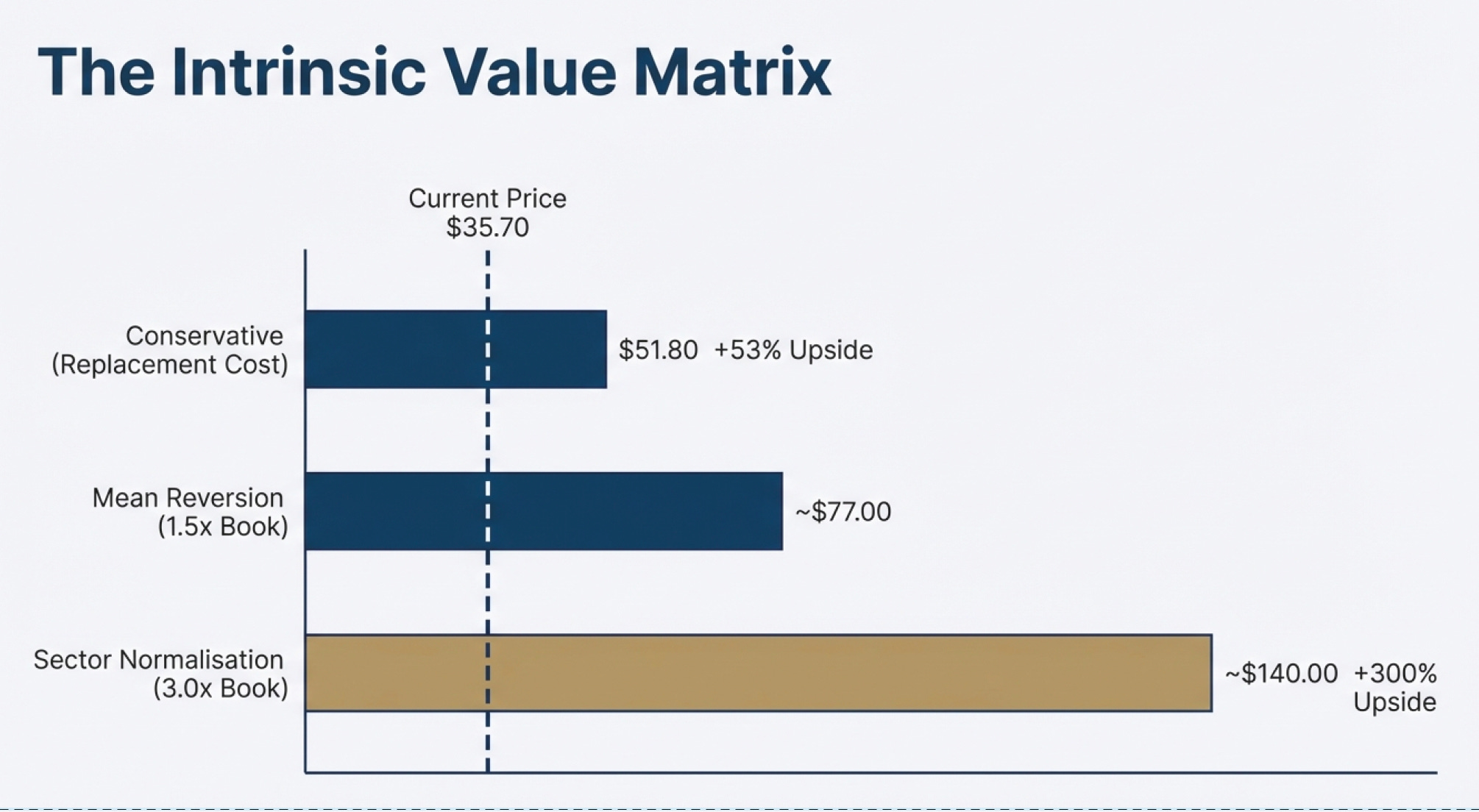

Conservative case (Replacement cost): ~$51.8 (1.5× upside)

Sector average case (3× book): ~$99/ share (2.7× upside)

What You’re Really Buying

Let me put this in perspective with the actual economics:

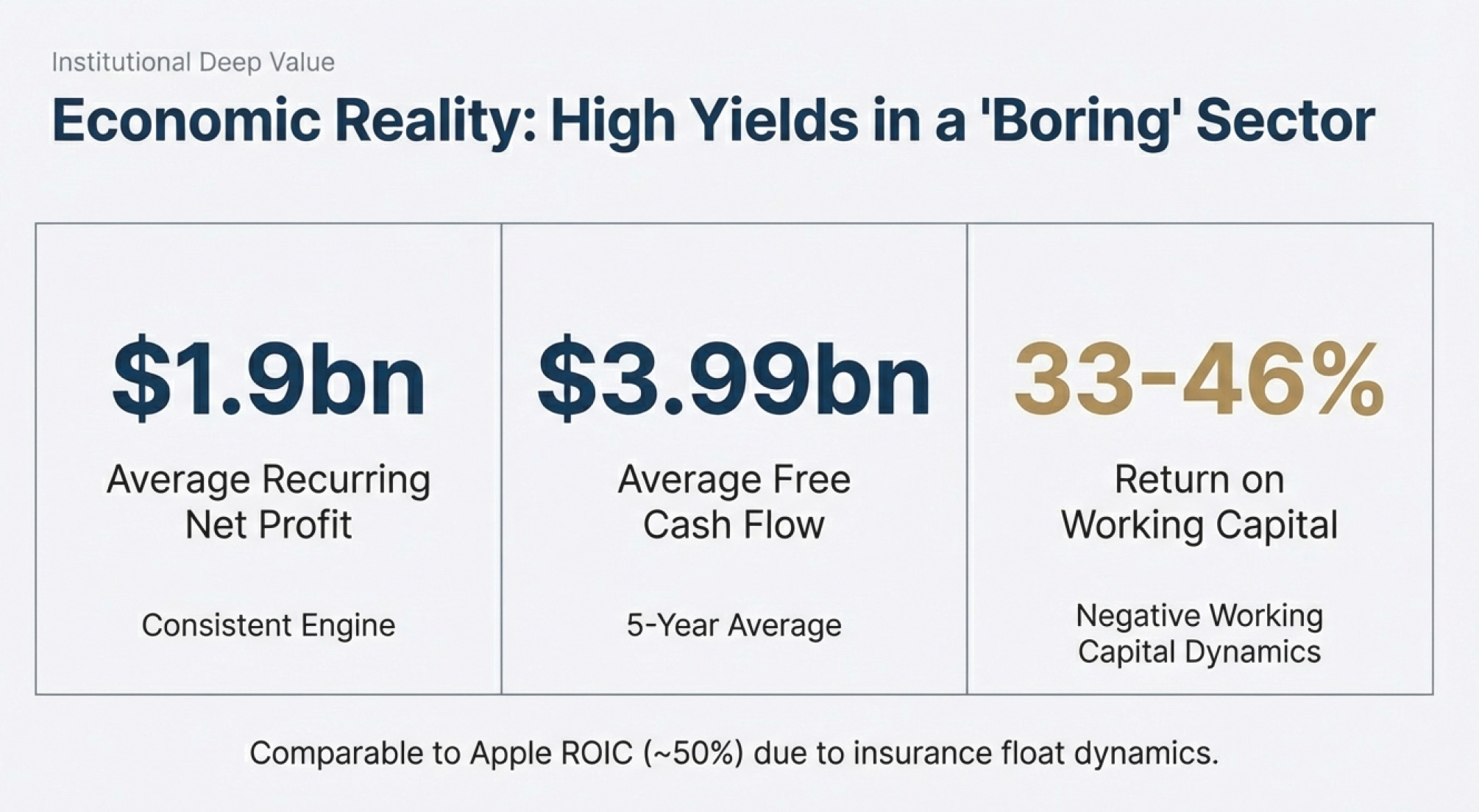

Great operating Performance (4-year averages):

Average recurring net profit: $1,928 million/year

Free cash flow (5-year average): $3,990 million/year

Returns on working capital: 33%

2024 returns on working capital: 46%

Cash Conversion Cycle improving significantly

(figures in millions $USD)

4 year average adjusted recurring net profit = [($1,347 + $785) + ($1,202 + $1,009) + ($2,702-$864) + ($3,305 - $1,771)] ÷ 4 years = $1,928 million

4 year average net working capital = [($12,238 - $10,617) + ($13,272 - $10,979) + ($15,532 - $17,714) + ($19,713 - $15,024)] ÷ 4 years = $1,605 million

4 year average PP&E = ($6,957 + $4,986 + $2,415 + $2,426) ÷ 4 years = $4,196 million

Returns on working capital = $1,928 ÷ ($1,605 + $4,196) = 33% on a 4 year average

These are Apple-tier returns (Apple does ~50%) in a healthcare services business with government-backed revenues.

The Transaction Comparables Tell the Story

When Medicaid books actually trade hands, they command significant premiums:

Even at the lowest comparable of $1,266 per member, you’re looking at $16.4B for just the Medicaid book. But strategic buyers have paid 2-5× more than that.

The Medicaid “Crisis” in Context

Here’s what the market is freaking out about: potential Medicaid cuts. Let’s look at the actual numbers:

Announced reduction over 10 years: ~$1 trillion

Annual reduction: ~$100 billion/year

Current annual Medicaid spending: $900 billion

That’s an 11% market reduction spread over a decade.

Does an 11% market headwind over 10 years justify a discount of almost 50% to book value? For a business with:

State-guaranteed payments

Counter-cyclical enrollment (grows during recessions)

No customer acquisition costs

Legal requirements ensuring actuarially sound rates

Absolutely not.

The Valuation Range

Putting it all together:

Conservative (Liquidation + Required Capital): $26.5B → 53% upside

Bull Case (Sector Average 3× P/B): $49.2B → 194.6% upside

Current Market Cap: $16.7B

Even if Medicaid loses 20% of its value over the next decade—far worse than the projected 11%—you’re still buying at a massive discount to intrinsic value.

Why This Discount Exists

The market is pricing in:

✅ Temporary Medicaid margin compression (real, but cyclical)

✅ ACA marketplace challenges (being repriced for 2026)

✅ Legal settlements (mostly resolved, $1B+ already paid)

✅ Recent $6.7B goodwill impairment (non-cash, already reflected)

But the market is not pricing in:

State rate resets coming in 2026-2027

Counter-cyclical enrollment benefits from economic softening

Structural moats in Medicaid managed care

Government’s inability to let essential healthcare infrastructure fail

The birds in the bush: conservatively $25.5B to $49.2B in intrinsic value.

What you’re paying today: $16.7B.

That’s a 1.5× to 4.4× return to fair value—before considering any growth, rate improvements, or economic cycle benefits.

🔑 How Sure Are You?

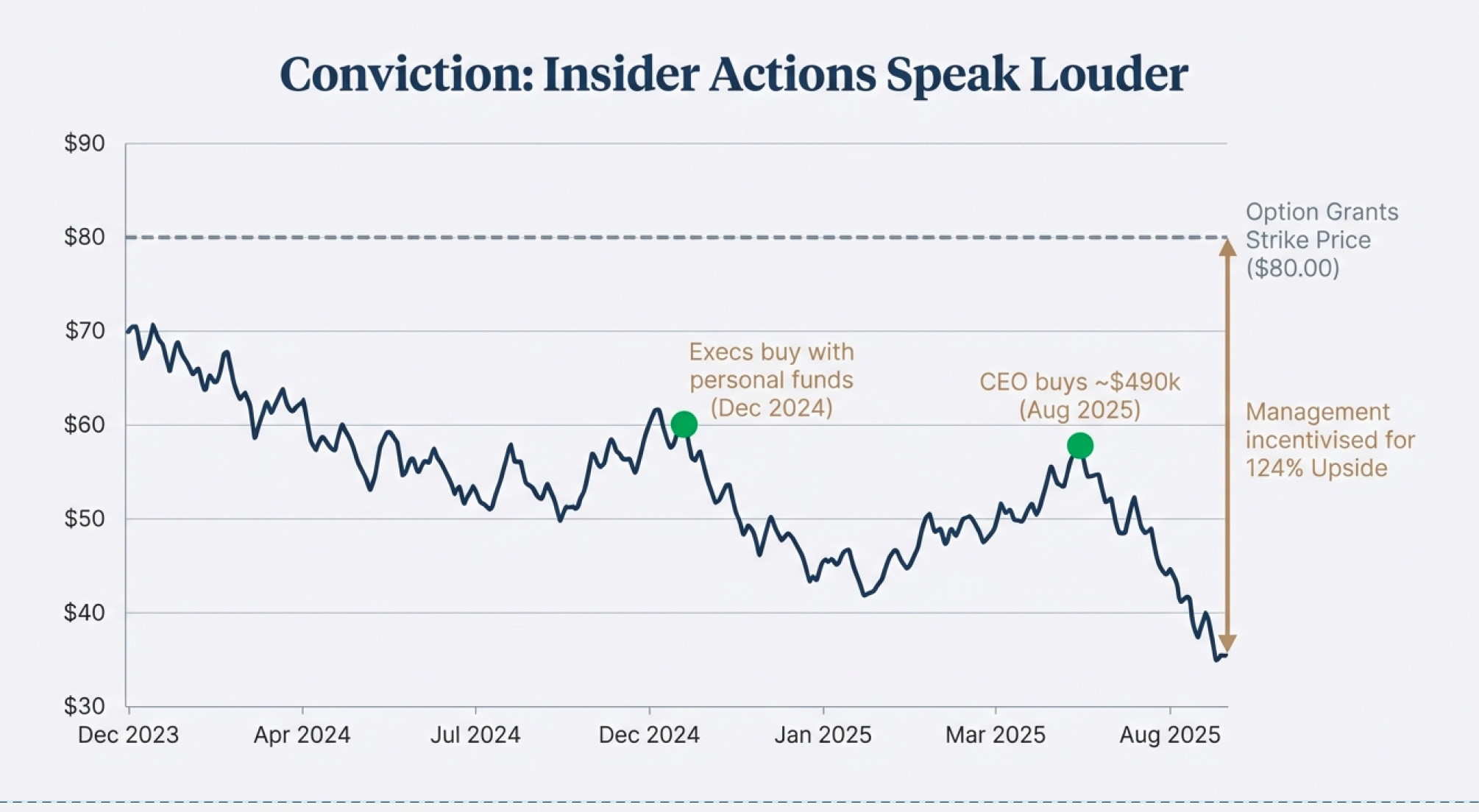

Insider Actions Speak Louder Than Words

Corporate insiders have made significant open-market purchases, distinct from restricted stock unit grants that executives receive as compensation.

Major Purchases (End 2024 - 2025):

December 2024 saw substantial insider buying when the stock traded in the low $60s following initial concerns about ACA Marketplace performance. Multiple executives made purchases in the $50,000-$200,000 range.

August 2025 brought another wave of purchases after the July guidance withdrawal sent shares plummeting. The most significant purchase came from the CEO, who bought approximately $490,000 worth of shares in open-market transactions. While this represents only about 2% of her total portfolio, the timing is notable: immediately after the worst news had been announced and the stock had already fallen 40%.

These purchases occurred at prices between $58-$65 per share when insiders had full knowledge of the problems. They knew about the ACA risk adjustment shortfall. They knew about elevated Medicaid costs. They knew about the upcoming goodwill impairment. Yet they chose to buy with personal funds, not just accept RSU grants.

These are pretty significant especially in December 2024 and August 2025. Especially the CEO ($490k) although it’s only 2% of her portfolio.

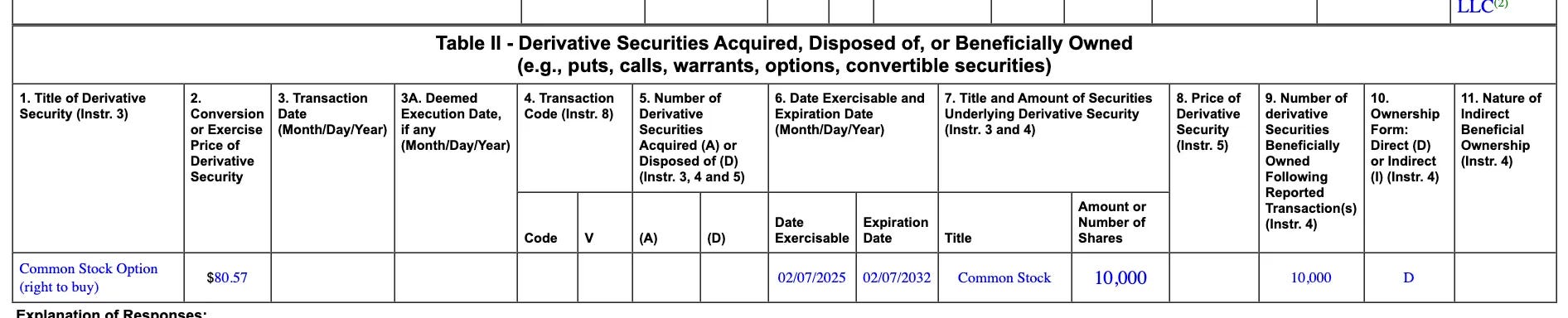

In recent periods, insiders were issued substantial stock options with an $80 exercise price. These options only become valuable if the stock rises above $80, which represents 124% upside from current levels of $35.70. The $80 strike price suggests management’s internal projections assume significant recovery, though the exact timing and quantity of these grants aren’t fully disclosed in the available documents.

The Legal Foundation That Changes Everything

This investment doesn’t rely on market sentiment, management brilliance, or favorable trends. It relies on something far more solid: federal law.

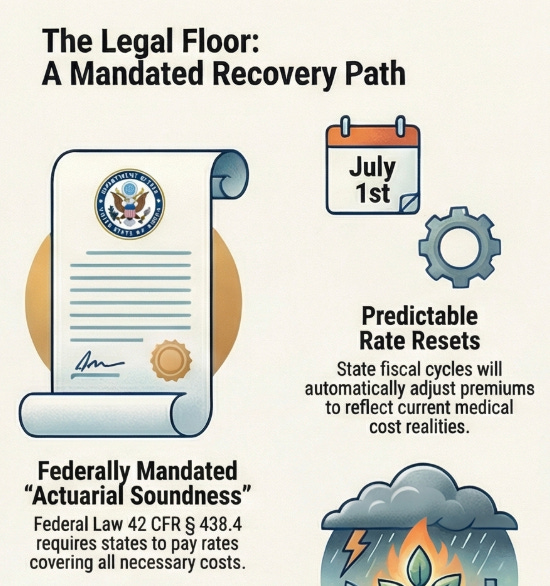

Federal Regulation 42 CFR § 438.4 establishes a critical requirement that most investors completely overlook. State Medicaid agencies must ensure that capitation rates paid to managed care organizations are “actuarially sound.” This legal term has a specific meaning: the rates must be sufficient to cover all reasonable and necessary costs for providing services to Medicaid enrollees.

Think about what this means in practice. By federal law, states cannot pay Centene rates that would make the business unprofitable. The government has legally obligated itself to ensure Medicaid managed care remains financially viable. This isn’t a regulatory suggestion or guideline—it’s a mandate enforced by CMS (Centers for Medicare & Medicaid Services), which must approve all state Medicaid rates.

Why does such a law exist? Because Centene and companies like it provide essential healthcare infrastructure to 13.1 million Americans. States cannot simply allow this system to collapse. They lack the administrative capability, provider networks, claims processing systems, and actuarial expertise to manage Medicaid in-house. It took Centene decades to build this infrastructure. States cannot replicate it, and they know it.

Consider what would have to happen for Centene’s Medicaid business to permanently fail. States would need to either take Medicaid management back in-house (impossible given lack of infrastructure), accept losing 50-75% federal matching funds (financial suicide), or leave millions without healthcare coverage (political and economic disaster). None of these scenarios has ever occurred in Medicaid’s 60-year history. None ever will.

How Government Payment Actually Works

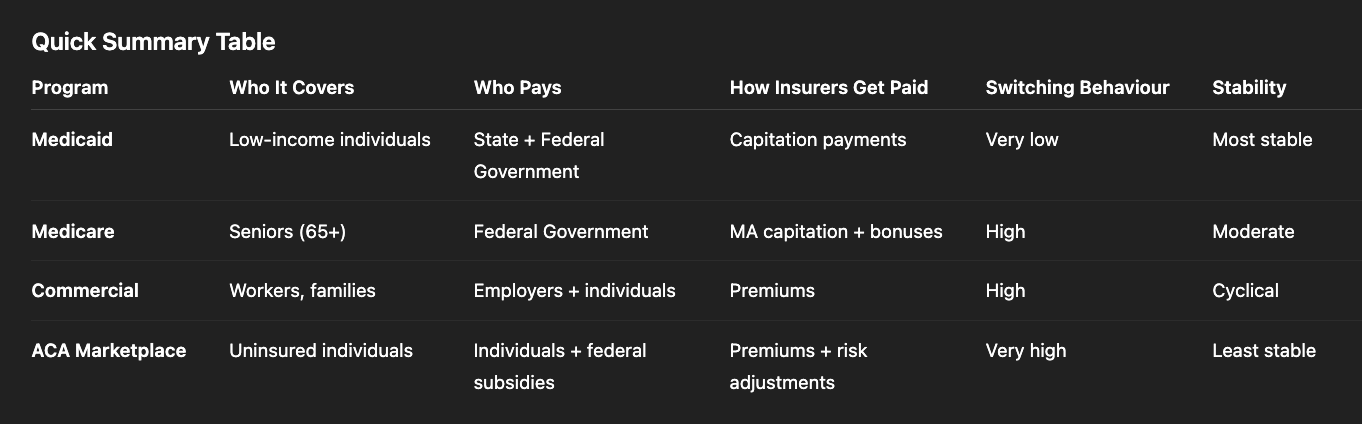

Before we continue, let’s have a quick introduction on the marketplaces

Medicaid - Government insurance for low-income individuals, funded by state and federal dollars. Insurers receive fixed per-member payments, making it stable and counter-cyclical with very little member switching.

Medicare - Federal insurance for people 65+ and certain disabled individuals. Private Medicare Advantage plans get monthly federal payments but face high competition and frequent member switching.

Commercial Insurance - Employer-based or individually purchased plans paid by companies and workers. Highly competitive, expensive to acquire customers, and enrollment drops during economic downturns.

ACA Marketplace (Obamacare) - For people without employer insurance who may receive federal subsidies. Very price-sensitive, members shop annually, and profitability depends heavily on accurate pricing and risk adjustments.

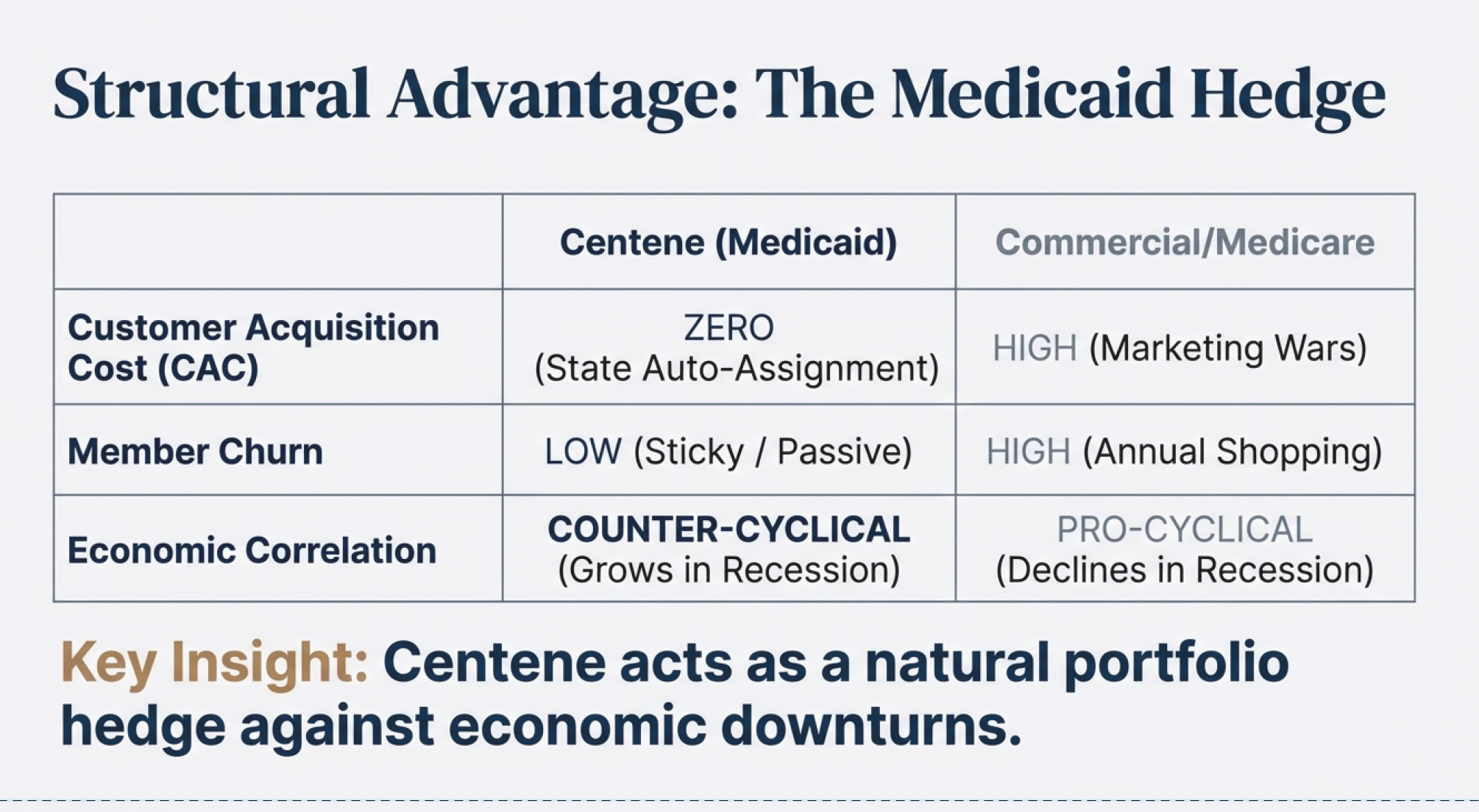

Understanding Centene’s revenue certainty requires understanding how Medicaid managed care payments flow. Despite this move not being a SOYA (Sit-On-Your-Ass) play for me, it does has some significant moats that we will talk about. One of Centene’s fundamental difference from commercial insurance lies in their Medicaid (64% of revenue) segment of the business. In commercial insurance, customers can, and tend to stop paying premiums or switch carriers easily, such behaviours are rare in Medicaid especially when a organization (hint: Centene) owns a significant Medicaid share in a state.

Centene receives fixed per-member-per-month capitation payments directly from state governments. These payments are backed by federal matching funds, which typically cover 50-75% of costs depending on the state. There is almost zero risk (there is a dark truth behind this which we shall not go into, but you can find it in “The Price We Pay” - by Marty Makary) of member non-payment because members don’t pay anything. The government sends Centene automatic, guaranteed monthly payments for every enrolled member.

Compare this to Medicare Advantage, where UnitedHealth, Humana, and CVS spend hundreds of millions annually on TV advertising, agent commissions, broker fees, and lead generation. They fight tooth and nail for every member because seniors actively shop and switch plans each year. Centene faces none of this. States auto-assign most Medicaid members. There are no marketing wars. Members don’t shop around. Once a state awards an MCO contract, it typically runs for multiple years with automatic renewal provisions. The infographics below demonstrates Centene’s position in the Medicaid market.

The enrollment patterns are equally predictable. Medicaid eligibility is tied to income thresholds and state rules, not personal choice. And things are even more exciting when times are bleak. When someone loses their job, they automatically qualify for Medicaid. During the 2008 recession, millions lost employment. More people became Medicaid-eligible. Centene’s membership grew, revenues increased, and margins actually expanded because these newly eligible members were generally healthier than the existing population (essentially massive customers inflow at 0 Customer Acquisition Cost). The business is counter-cyclical by design.

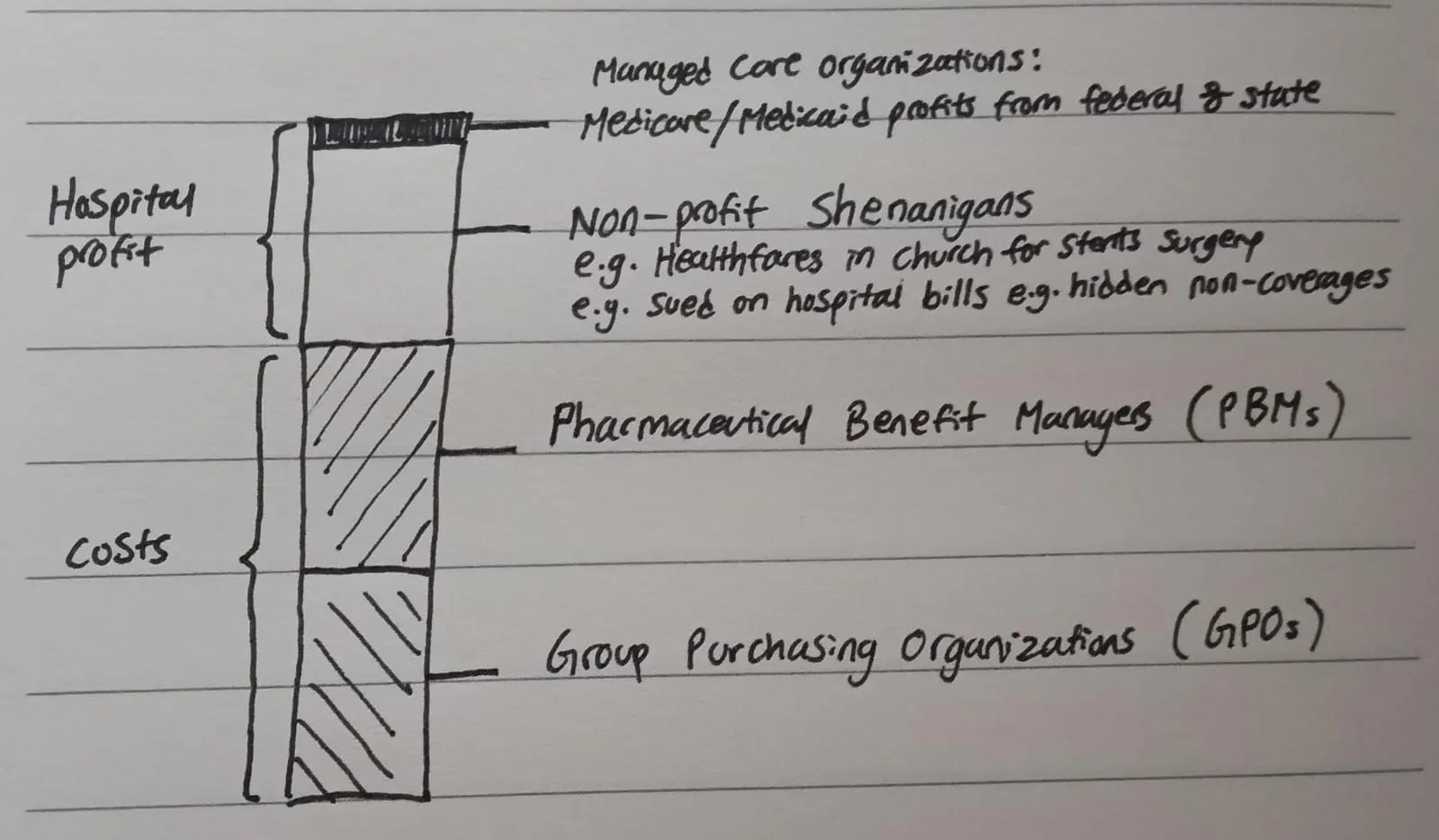

If we take a look at the “supply” side of stuff, the business becomes even more exciting (shall not talk about more “dark truths”) as partnerships become so entrenched that smaller Managed Care Organization (MCO) are not able to attain the benefits that companies with significantly larger market share has. Whilst on the other hand, healthcare partners and service providers e.g. hospitals have almost no choice but to partner up with the larger MCOs due to the customer base it has. This also involves a highly complex relationship with PBMs (Pharmaceutical Benefit Managers) and GPOs (Group Purchasing Organisations) which eventually results in premiums on products and services that makes healthcare unaffordable.

What Every Competitor Is Saying

Every major Medicaid MCO is experiencing the same margin compression. This isn’t a Centene-specific problem—it’s an industry-wide rate reset cycle.

Documented statements from competitors (2025):

Elevance CFO (November 2025):

Warned Medicaid would hit a trough in 2026

Operating margin projected at -1.75% before rebounding

Attributed to higher-acuity members and specialty drug costs

Costs “outpace payment rates” (temporarily)

UnitedHealth executives:

Medicaid margins will worsen into 2026

Driven by “dislocation of premium funding”

Elevated costs: behavioral health, specialty pharmacy, home health

2026 expected to be the low point

Recovery to “modest 2% margins” by 2027-28

CVS Health:

Exiting ACA individual market by 2026

Cannot price policies profitably under current structure

Industry-wide pattern: When all major players report the same issue, it’s not company-specific execution failure. It’s a systemic pricing lag that corrects through the annual rate-setting process.

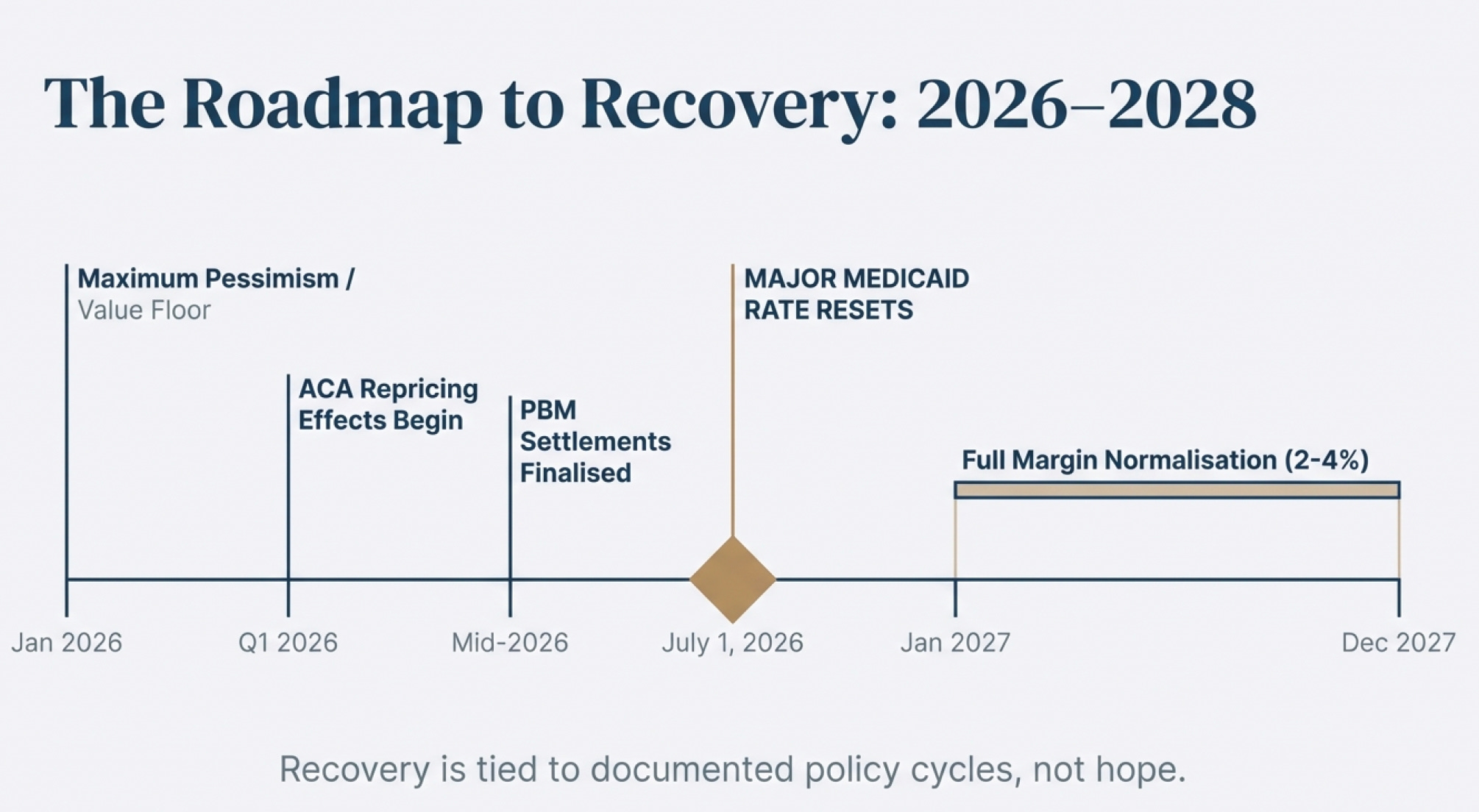

The Rate Reset Mechanism Explained

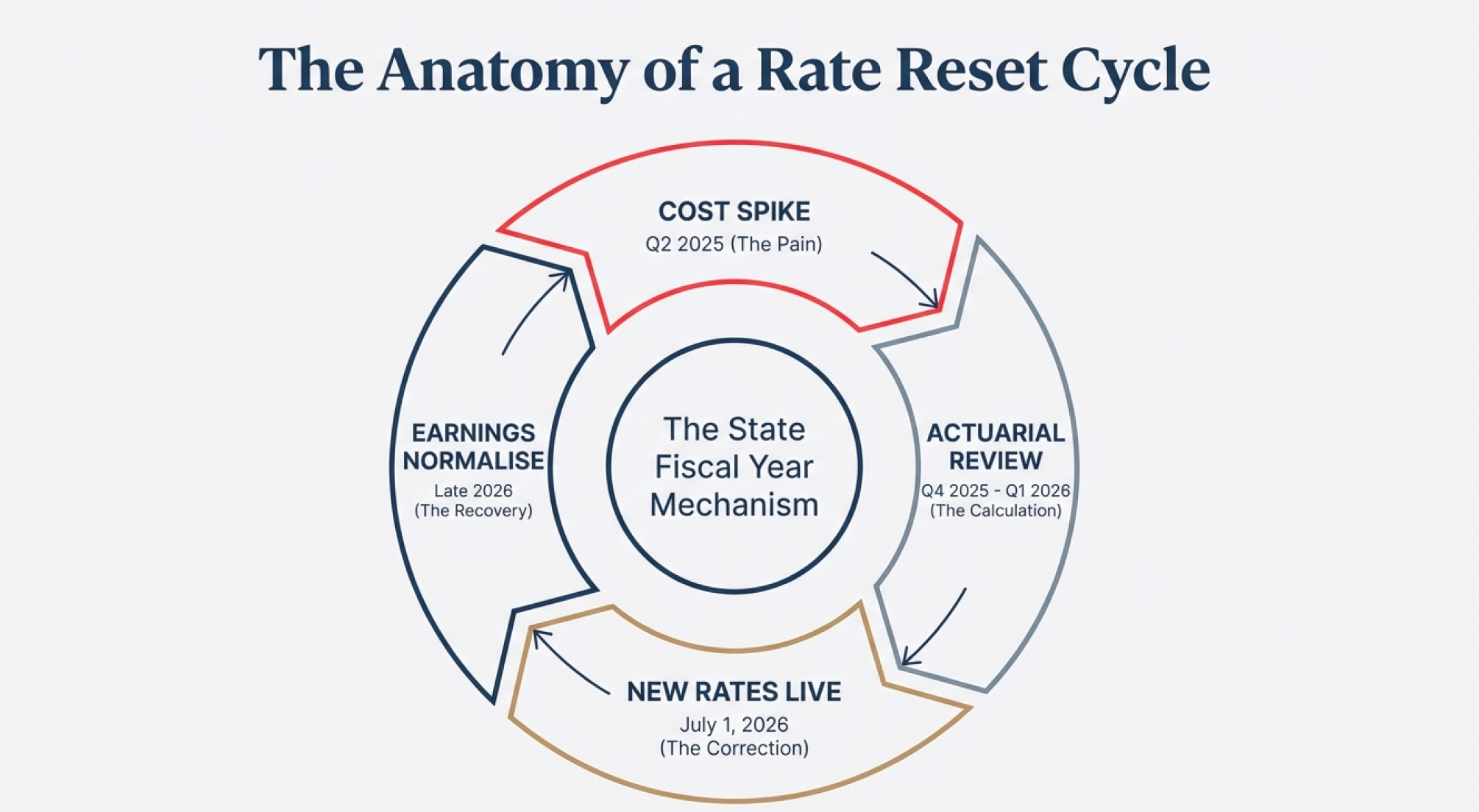

State Medicaid rates don’t reset automatically or instantaneously when costs spike. There’s a predictable lag that creates temporary margin compression followed by recovery. Understanding this cycle is essential to understanding why Centene is mispriced.

States operate on fiscal years, typically running July 1 to June 30. The capitation rates they pay to MCOs reset annually at the start of each fiscal year. Here’s how the cycle plays out in practice.

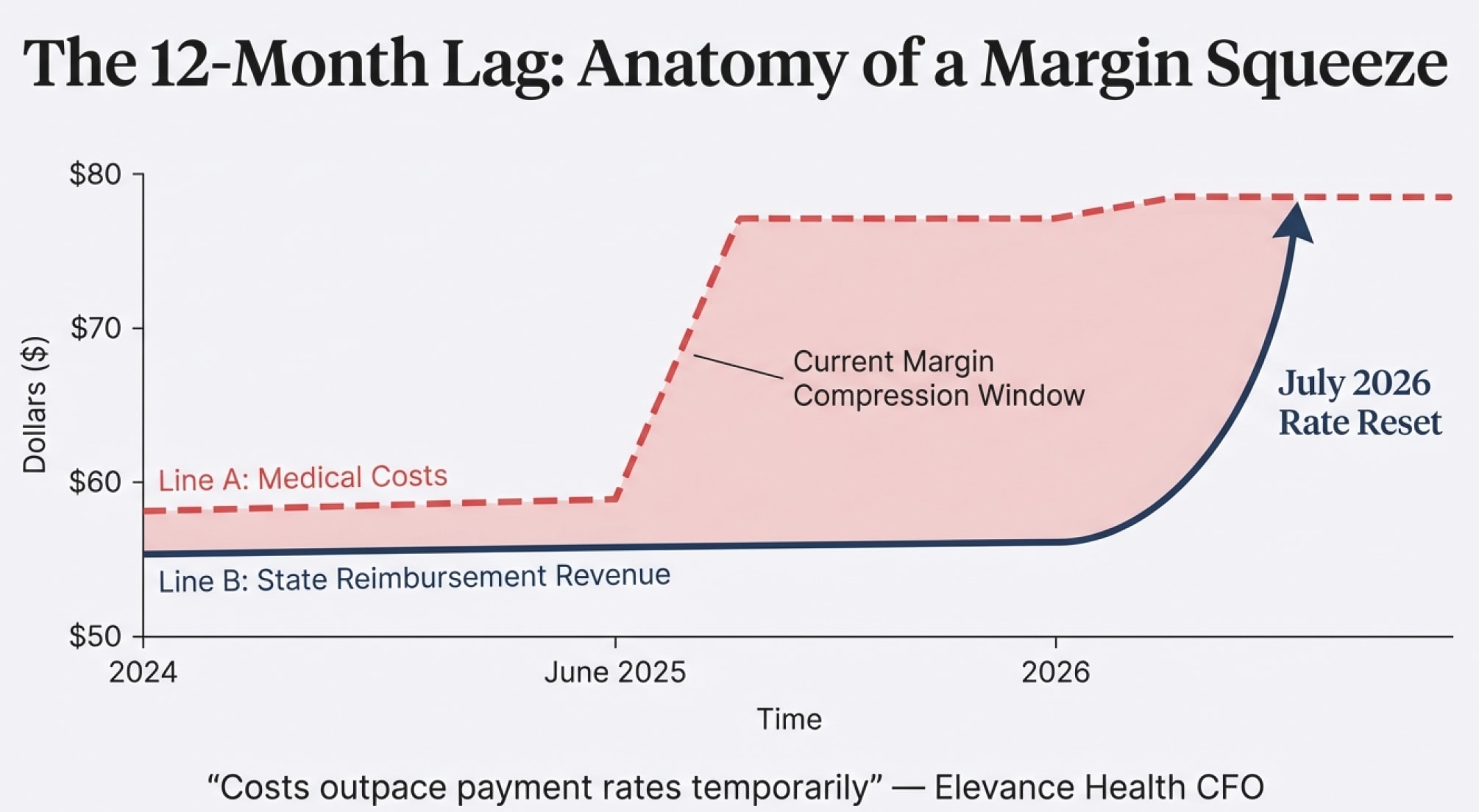

First, a cost spike occurs. This happened to Centene in Q2-Q3 of 2025 when behavioral health utilization, specialty drug costs, and home health services all increased simultaneously. The company reported these higher costs in Q3-Q4 2025, leading to the massive stock price decline. But the rates Centene was being paid were set 12-18 months earlier based on 2023-2024 cost data. The mismatch between old rates and new costs created the margin squeeze.

Next, states conduct actuarial reviews. Throughout Q4 2025 and Q1 2026, state Medicaid agencies are legally required to analyze whether current rates remain actuarially sound. They review actual medical claims data, trend analysis, and MCO financial reports. CMS must approve any rate changes to ensure federal matching funds continue.

Then new rates become effective. For most states, this happens July 1, 2026. The new rates reflect the higher cost environment. MCOs like Centene receive immediate premium increases—typically 5-15% depending on the state—while their costs have already stabilized. This is when margins expand rapidly.

Finally, financial results reflect the improvement. By Q3-Q4 2026 or Q1-Q2 2027, Centene’s reported earnings show normalized margins. The stock price eventually follows, though often with additional lag as investors wait for proof of sustainability.

This exact pattern has played out repeatedly in Medicaid managed care history. In 2016-17, pharmacy costs spiked following the introduction of expensive hepatitis C drugs and specialty oncology medications. MCOs saw margin compression. States conducted reviews. Rates reset in mid-2017. Margins recovered by late 2017 and early 2018. In 2021-22, COVID-related acuity adjustments created another cycle of compression and recovery. Now in 2024-25, we’re seeing the same pattern following the end of pandemic-era continuous enrollment provisions.

What Centene Has Already Fixed

Management actions (not promises—actual executed changes):

ACA Marketplace repricing:

“In July 2025, we commenced the process of refiling 2026 policy year rates to reflect a higher projected baseline of Marketplace morbidity than previously expected. We currently expect to be able to take corrective pricing actions for 2026 in states representing a substantial majority of our Marketplace membership.”

Translation: They’ve already filed higher premiums for 2026 to fix the ACA issue

Medicaid margin guidance:

Company stated Medicaid margins “will be consistent into 2026”

This is different from what other MCOs are saying (who expect further deterioration)

Implies Centene’s data analytics and state negotiations are further along

Value-based care expansion:

Actively shifting to value-based provider arrangements

Reduces cost volatility by sharing risk with providers

The Legal Settlement Scorecard

Investors obsess over Centene’s legal troubles, but the actual financial exposure is largely resolved.

State PBM (Pharmaceutical Benefit Managers/ disgusting middle-mans that contributes in high drug costs) settlements:

Over $1 billion already paid to settle with majority of states

Remaining “holdouts” (like Georgia) in final negotiation phases

Estimated resolution timeline: 3-9 months (mid-to-late 2026)

Florida controversy:

$67 million settlement completed

Criminal investigation targets state officials, not Centene

Centene followed the settlement agreement signed by Florida officials

Worst-case financial impact: already reflected in existing settlement reserves

Securities fraud class action:

Filed mid-2025 following guidance withdrawal

Typical timeline: 2-3 years (late 2027-2028)

Standard disclosure-related lawsuit that follows any major stock drop

Does not impair business operations or cash flows

The key point: the largest financial obligations are behind Centene. The $1+ billion in PBM settlements has been largely paid. Remaining litigation represents ordinary-course legal issues that any large public company faces.

Understanding the Goodwill Impairment

In October 2025, Centene recorded a $6.7 billion goodwill impairment charge. Headlines screamed. The stock dropped further. Investors panicked. But understanding what this actually means reveals why it’s largely irrelevant to intrinsic value.

Goodwill is an accounting fiction created when companies make acquisitions. If Centene pays $5 billion to acquire a company with $3 billion in tangible assets, the $2 billion difference gets booked as “goodwill” on the balance sheet. It represents intangible value like brand names, customer relationships, and market position.

Accounting rules require companies to periodically test whether goodwill remains valuable. The test compares the “fair value” of reporting units to their carrying value on the balance sheet. Fair value is typically estimated using current stock price multiples or discounted cash flows.

During the mid-2025, rising Medicaid costs and anticipated deep cuts to subsidies (from the new “One Big Beautiful Bill Act,”) resulted in many analyst re-rating of the company’s valuation. They reduced the value to the company as they expected its earnings and market size to collapse from their DCF models. This resulted in the company’s market capitalization falling well below the book value of its reporting units. The event triggered further pessimism in the market and the company was forced to write down $6.7 billion in goodwill which significantly reduced the (intangible) book value of the company.

But here’s the critical part: this is a non-cash accounting charge. No money left the company. No operations were impaired. No members were lost. No contracts were cancelled. Centene didn’t pay $6.7 billion to anyone. They simply adjusted an accounting entry on the balance sheet to reflect the lower stock price.

The impairment doesn’t affect cash flows, operations, or ability to serve members. It doesn’t affect the statutory capital requirements, which remain fully satisfied. It doesn’t indicate business deterioration.

The Medicaid “Cut” That Isn’t

The market is pricing in catastrophic Medicaid cuts that would permanently impair Centene’s business. Let’s examine what’s actually being proposed versus what the market assumes.

Current proposals suggest reducing federal Medicaid spending by approximately $1 trillion over ten years. That sounds enormous until you do the math. One trillion over ten years is $100 billion per year. Current annual Medicaid spending is approximately $900 billion. The proposed reduction is 11% of total spending.

Moreover, this isn’t an immediate cliff. The implementation timeline spans a full decade with gradual phase-in. The cuts would primarily affect eligibility criteria, not payment rates for existing members. States would face difficult choices about who qualifies for coverage, but they wouldn’t arbitrarily slash reimbursement rates below actuarially sound levels because federal law prohibits it.

The political reality makes even these proposed cuts uncertain. The bill remains in discussion and hasn’t passed. As noted in the research: “If the feds leave those who lose coverage out to die, the democrats/republicans responsible will get ousted during the next election.” States have enormous incentive to backfill any federal cuts with their own funding or find alternative approaches to maintain coverage levels.

Even if we assume the full $1 trillion reduction occurs exactly as proposed, we’re talking about an 11% market contraction over a decade. For context, consider that Medicaid enrollment is counter-cyclical. During the 2008 recession, enrollment surged as job losses made millions newly eligible. If the U.S. economy weakens over the next 2-3 years—which many indicators suggest is likely—Medicaid enrollment could grow significantly even with tighter eligibility rules. The counter-cyclical nature of the business provides a natural hedge against economic downturns that typically hurt most companies.

The Certainty Framework

Let me summarize what we know versus what we’re betting on:

Facts (100% certain):

✅ Federal law requires actuarially sound rates

✅ States legally cannot let major MCOs fail

✅ Centene maintains required statutory capital

✅ Company generates $3-4 billion annual free cash flow

✅ Rate resets occur annually on state fiscal years

✅ All major MCOs facing same margin pressure (systemic, not company-specific)

✅ Most legal settlements already paid

✅ Replacement cost is $53.90 vs. current price of $35.70

High probability (>80%):

State rate resets will occur by mid-2026 to mid-2027

Margins will normalize to historical ranges (2-4%)

Medicaid enrollment will grow if economy weakens

ACA marketplace repricing will improve 2026 results

What we’re NOT betting on:

❌ Revolutionary new products

❌ Market share gains from competitors

❌ Multiple expansion beyond historical norms

❌ Perfect execution by management

❌ Policy changes favoring insurers

The certainty comes from:

Legal obligations states must fulfill

Economic impossibility of alternative scenarios

Historical precedent of rate reset cycles

Structural characteristics of Medicaid managed care

Documented financial strength and capital adequacy

This isn’t a speculative growth story. It’s a documented value gap between market price ($16.7B) and legally-mandated, structurally-sound business value ($25.5B minimum).

The question isn’t “if” the value gap closes. The question is “when”—which is what we’ll cover in the next section.

🔑 How Fast Till You Get Them Out

The final question in this deep-value framework is timing: when will the gap between Centene’s current market price and its intrinsic value begin to close?

The answer lies not in speculation, but in documented policy cycles, confirmed regulatory timelines, and already-executed corporate actions.

Below is a clear, fact-based roadmap grounded entirely in the operational, legal, and policy timing contained in the research.

Note: in value investing, we don’t time the market but in my case, where i am taking high risk utilising LEAP options, i am exposed to significant time risk

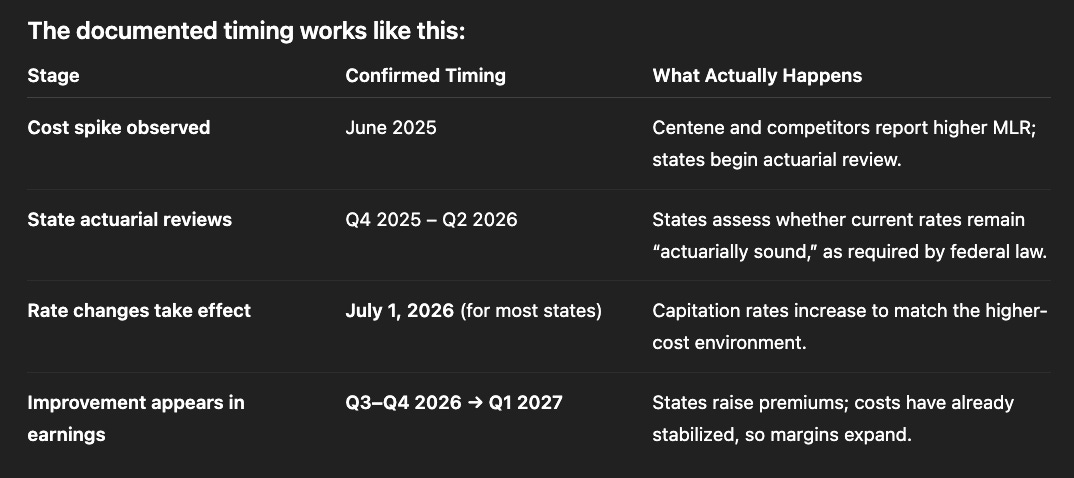

1. The Medicaid Cost Shock Has a Known Start Date

Centene’s margin pressure began in June 2025, when behavioral health, specialty drug costs, and home-health utilization spiked across the industry. This was publicly disclosed in the company’s financials and was consistent with every major Medicaid MCO.

This date matters because it anchors the entire recovery cycle.

2. Rate Resets Follow a Predictable Annual Calendar

Most states operate on a July 1 → June 30 fiscal year, and Medicaid capitation rates — which determine Centene’s revenue — are adjusted only during these scheduled cycles.

This cadence has repeated historically — after the 2016–17 specialty drug shock and after the 2021–22 COVID acuity spike.

The pattern is the same every time:

Cost spike → actuarial review → July 1 rate reset → margin recovery within the next 1–3 quarters.

3. Marketplace Repricing Has Already Been Executed

Centene disclosed that in July 2025 it began refiling 2026 ACA Marketplace rates to reflect higher morbidity.

These filings cover the majority of its Marketplace membership.

This is not an intention or projection — the company has already completed the administrative work.

Effect timing:

Policy year: 2026

Pricing impact: Begins January 2026

Financial reflection: Q1 2026 results (reported April 2026)

Marketplace issues were a major driver of the 2025 sell-off; the corrective pricing work is already done.

4. Industry-Wide Recovery Window Is Documented

Multiple insurers gave public guidance confirming the same cycle:

Elevance (Nov 2025):

Medicaid trough expected in 2026

Operating margin about –1.75%

Recovery visible 2027–2028

UnitedHealth Group:

Medicaid margins worsening into 2026

Recovery begins 2027 → 2028

These are not opinions — these are public disclosures from the largest Medicaid MCOs in the U.S. This positions 2026 as the documented trough and 2027–2028 as the documented recovery window.

Centene’s recovery pathway is not speculative — it is tied to legally required rate adjustments, fixed fiscal calendars, and already executed filings.

Earliest visible improvements:

Mid–2026 (Q3/Q4 2026 earnings)

Full normalization window:

2027 → early 2028

In other words, till 2028, there is actually 2 “Lifelines” for Centene to adjust rates and recover. This timing is aligned with the natural cycles of Medicaid pricing and legal resolution, giving the company a clear, documented path toward valuation re-rating.

🔑 Conclusion

Centene is not a speculation, a turnaround story, or a bet on management brilliance. It is a legally protected, structurally entrenched, economically essential business that the market has priced as if its foundation were permanently impaired. The research shows that this simply isn’t the case.

Every major factor suppressing Centene’s valuation today — Medicaid margin compression, ACA repricing issues, PBM settlements, goodwill impairment, and even the political noise around federal budget proposals — is tied to known, finite, time-bound cycles. None of them change the company’s core economic engine:

A massive, government-backed customer base

Counter-cyclical enrollment

Actuarially required reimbursement

Statutory capital strength

Decades of entrenched relationships with states and providers

Low acquisition costs and high return on working capital

The intrinsic value range derived from the data is wide, but all points converge on the same conclusion:

Centene is worth far more than what the market is currently willing to recognize.

A liquidation-floor valuation already sits above today’s market cap.

A return to historical book multiples doubles the valuation.

A sector-average re-rating produces multi-bagger potential.

And the timeline for unlocking that value is grounded in documented state fiscal cycles and industry guidance — not hope.

Because of this, I’ve taken a significant position. Not as a gamble, but out of conviction built on:

hard financials

statutory requirements

consistent industry patterns

resolved and soon-to-be-resolved legal overhangs

and the predictable nature of Medicaid rate mechanics

Centene’s current price reflects a temporary dislocation, not a permanent impairment. The next 12–36 months will simply allow the underlying fundamentals, legally mandated rate corrections, and full-cycle normalization to surface.

This is exactly the kind of investment I look for — a misunderstood, essential, and deeply undervalued business — and it’s why I’m willing to size the position meaningfully.

21 Jan 2026 Conviction Update

A short but important note to “How fast till you get them out”: people are dying, so this is pretty urgent. Statistics show that for every 1% increase in health care costs, death rates go up by 2%! Even on a worldwide basis, the problem is becoming more prominent. The question is no longer “when will the government solve it”, but “how will they solve in within the next 1 year” because people are dying!

And there is no doubt (no speculation) that Medical insurance companies have to benefit when this problem is solved - why am I so confident? - because the way the industry works is that healthcare insurance is just “transfer payment”.

As clarity (using inversion thinking):

What will cause the opposite reaction to the crash would be (in the case of Centene): For Medicaid - medical cost ratio decreasing as risk pool in medicaid reduces

And this has to happen because high risk pools are unsustainable for government payouts - and they can’t stop payouts since it’ll significantly affect the economy

Neither can they squeeze Centene to unsustainable losses, or no one would be able to manage the program for them

Not to forget the 10% reduction in valuation which we made above still puts us in a nice margin of safety.

What will cause the opposite reaction to the crash would be (in the case of Centene): For ACA marketplace - government continues to subsidise ACA marketplace + evidence that membership and margins won’t deteriorate as much as feared.

The U.S. House has already passed a bill to restore and extend enhanced ACA premium tax credits for three years. Even if this does not pass, they have to do something similar because things are getting pretty bad to members who are not covered (we’re talking about deaths).

Enrollment holds up better than expected (right now, the whole ACA marketplace is removed from the valuation): paid effectuated enrolment (who actually pay) ends up materially higher than feared (complete removal of ACA marketplace), reducing unit-cost pressure

KFF notes that 2026 ACA premiums are rising sharply (about 26% on average on current rates which people are receiving tax credits for), and if costs don’t rise as fast as premiums on an absolute basis, underwriting margins can “surprise” to the upside

From the article: https://pmc.ncbi.nlm.nih.gov/articles/PMC5158240/#:~:text=A%20recent%20RAND%20report%20considered,the%20individual%20health%20insurance%20market. What the above suggests is that: if ACA marketplace subsidies are being removed by the government, approximately 68% of the ACA marketplace members would be disenrolled. However, KFF also suggests that ACA premiums rises 26% on average which actually offsets a significant amount of the 68% premium loss (32% remaining members absolute premium x 26% added = c.40% absolute premium relative to current levels).

Moreover, data have also shown that less affluent individuals tend to have poorer health outcomes and higher healthcare risks on average. This stems from correlations between low socioeconomic status and increased prevalence of chronic conditions, as well as barriers to preventive care. Which also means that medical-loss-ratio would be reduced, further offsetting the loss of the 60% - since margins are “Modestly Negative to Slim” (based on Oscar health) e.g. a 10% increase in revenues of a $100m company with 1% net margin would mean a 100% increase in net margin. The reverse can also be true in this case (which many do not realise). This is not speculative but factual surveyed data.

Something interesting to note as well: when the motivation of “protecting one’s asset” outweighs the ESG component of “not wanting to get involved in a dirty company”, market sentiment and performance will invert (and let’s not try to speculate what will happen to AI in the coming few months 😉).

To exacerbate matters (performance of stock), a ton of investors are indiscriminately selling healthcare insurance companies like United Health Group (which as a value investor is pretty good for me).

It is not that i am trying to profit from others’ misery, but rather, being practical about the situation and being level headed as an investor.

That being said, i do empathise with the situation the more I learn about it. A majority of people who have joined healthcare are in the sector to serve and help others, they have a calling to really care - but it is really the capitalistic incentives that is in the system that is making things turn ugly - not the insurance providers, not the people working in them, because people do really want to help. In the long-term i have a pretty optimistic view about the situation due to the heroes and people that are in the sector (and kantian fairness).

References

Centene Corporation Annual Report / Form 10-K (via Fintel)

https://fintel.io/doc/sec-centene-corp-1071739-10k-2025-february-18-20137-3766Molina Healthcare Q3 2025 Financial Results

https://investors.molinahealthcare.com/news-releases/news-release-details/molina-healthcare-reports-third-quarter-2025-financial-resultsMolina Healthcare Annual Report

https://investors.molinahealthcare.com/static-files/d19fbaa9-198b-4563-a5bd-02eeb6ea963bCVS Health Q3 2025 Results & FY 2025 Guidance Update

https://investors.cvshealth.com/news/news-details/2025/CVS-HEALTH-CORPORATION-REPORTS-THIRD-QUARTER-2025-RESULTS-AND-UPDATES-FULL-YEAR-2025-GUIDANCE/default.aspxCVS Health 2024 Annual Report

https://s206.q4cdn.com/752775519/files/doc_financials/2024/ar/CVS-Health-2024-Annual-Report.pdfElevance Health Q3 2025 Earnings Release

https://www.elevancehealth.com/content/dam/elevance-health/documents/earnings/3Q2025ELVEarningsRelease.pdfElevance Health 2024 Annual Report

https://s202.q4cdn.com/665319960/files/doc_financials/2025/ar/Elevance-Health-2024-10K-color.pdfUnitedHealth Group Q3 2025 Earnings Release

https://www.unitedhealthgroup.com/content/dam/UHG/PDF/investors/2025/unh-reports-third-quarter-2025-results-and-raises-full-year-2025-earnings-outlook.pdfUnitedHealth Group 2024 Annual Report

https://www.unitedhealthgroup.com/content/dam/UHG/PDF/investors/2024/UNH-Q4-2024-Form-10-K.pdfCentene + WellCare merger note (Advisory.com)

https://www.advisory.com/daily-briefing/2019/03/29/centeneKaiser Family Foundation (KFF) — Medicaid Spending & Budget Analysis

https://www.kff.org/medicaid/state-indicator/federalstate-share-of-spending

https://www.kff.org/medicaid/a-closer-look-at-the-50-billion-rural-health-fund-in-the-new-reconciliation-lawHKS Harvard — Health insurance subsidies & government shutdown impact

https://www.hks.harvard.edu/faculty-research/policy-topics/health/health-insurance-subsidies-behind-government-shutdownThe Conversation — ACA subsidies & shutdown impact

https://theconversation.com/how-the-government-shutdown-is-hitting-the-health-care-system-and-what-the-battle-over-aca-subsidies-means-266565Health Management Associates (HMA) — Medicaid Spending FY 2024

https://www.healthmanagement.com/blog/medicaid-spending-in-federal-fy-2024-totals-nearly-909-billionU.S. Congress — H.R.5371 Medicaid Budget Reduction Bill

https://www.govtrack.us/congress/bills/119/hr5371/textGuruFocus — financial ratios, valuation history, and data

https://www.gurufocus.com/Macrotrends — historical financial charts and KPIs

https://www.macrotrends.net/The Price We Pay — Dr. Marty Makary (book)

When Breath Becomes Air — Paul Kalanithi (book)

An American Sickness: How Healthcare Became Big Business and How You Can Take It Back — Elisabeth Rosenthal (book)

Medicare For Dummies — Patricia Barry (book)

Medicaid managed care transaction references used in valuation (Affinity Health Plan, Magellan Health, Magellan Complete Care, WellCare, etc.) — sourced from public filings, Advisory.com summaries, and company transaction announcements.

The Broken US Healthcare System is Failing Millions of Americans with Warris Bokhari

Found this an important reminder (from an article i read): the biggest culprit in rising health care costs is the rates charged by hospitals and doctors’ offices, which are in turn covered by insurers, experts say.

“Prescription drug spending and insurance company overhead and profits is a tiny slice of the pie compared to spending on hospitals and doctors,” said Cynthia Cox, senior vice president and director at KFF.

“You can imagine cuts in any of these categories, but where the money is is inpatient and outpatient care,” Cox said.

Now...can you imagine who will benefit when hospitals cut spending and claims lesser from health insurance? (albeit temporarily) - If "the top brass" is thinking clearly, they will be addressing this, the root cause (and not trying to renegotiate with health insurance)

Update: I made a mistake in my analysis. I utilized replacement cost as the book value of 1 which resulted in my valuation upside inflating. I have edited and amended to:

Conservative (Liquidation + Required Capital): $26.5B → 53% upside

‼️ Bull Case (Sector Average 3× P/B): $49.2B → 194.6% upside (It is important to note that this book value is based on 64% of their revenue-generating activity which is Medicaid. Hence, we are being extremely conservative here especially when we consider the fact that they have written off of c.$6.6B which theoretically have contributed to its durable moat. Therefore, we should include that, and if we do; we can get an approximate $69B in intrinsic value/ $140 per share, 313% upside)

Current Market Cap: $16.7B

To be honest, i'm not very satisfied with the margin of safety as this now becomes my 2nd best idea in terms of the quality of the stock. With its stock options availability I would still place it in the first place, but tbh its a relatively risky one since my MOS shrank - hence i'm not very satisfied

I will be posting the alternative opportunity i am looking at (in a few days) and might be look to re-adjust my position

P.s. Also note that this valuation is only based on the 64% of Centene's business - Medicaid. The valuation does not include its ACA and Medicare business